NAND flash is critical for data centres because it provides massive, non-volatile storage with exponentially faster read/write speeds, smaller physical footprints, and far greater energy efficiency than traditional Hard Disk Drives (HDDs). It is the foundation of enterprise Solid State Drives (SSDs) and modern cloud computing operations.

Why NAND is Indispensable

- Speed and Low Latency: NAND-based SSDs eliminate the mechanical delays of HDDs. This allows servers to feed data to processors in microseconds rather than milliseconds, solving major Input/Output (I/O) bottlenecks.

- Reliability: Because NAND has no moving parts, it is highly resistant to physical shock and vibration, making data centre hardware much more durable and less prone to mechanical failure.

- Energy Efficiency: Flash memory draws significantly less power and produces far less heat than spinning mechanical disks, heavily reducing the cooling and electricity costs of running a massive server farm.

- Massive Density: Modern advancements like 3D NAND and QLC (Quad-Level Cell) stack memory cells vertically, allowing data centres to pack petabytes of data into standard server rack spaces at a sustainable cost per gigabyte.

NAND’s Role in the AI Boom

The rise of Artificial Intelligence (AI) and Machine Learning (ML) has made NAND even more important.

- The “Cold Knowledge” Layer: While dynamic memory (DRAM) handles active, real-time token generation, AI models rely on vast NAND SSD pools to store and stage large training datasets, model checkpoints, vector databases, and retrieval systems.

- Inference Workloads: As AI usage shifts toward real-time inference, high-throughput NAND (paired with NVMe interfaces) is increasingly used to feed colossal datasets directly to specialized processing units.

- Technologies Leveraging NAND

- NVMe (Non-Volatile Memory Express): A protocol designed specifically for flash storage that removes system-level bottlenecks, allowing servers to process millions of I/O operations per second.

- Computational Storage: Emerging architectures that put processing power directly onto NAND-based drives, reducing the amount of data that must travel to the main CPU.

When you realise what is happening, it seems ever less likely that the memory boom will hit a cyclical peak any time soon.

From Data to Intelligence

Artificial intelligence isn’t just transforming software. It’s fundamentally reshaping the infrastructure that powers it. Behind every large language model, recommendation engine or real-time analytics platform sits an increasingly complex data centre architecture, where memory and storage are now as critical as compute.

At the heart of this shift is Micron, a company traditionally known for DRAM and NAND, who we have been partnered with for some time now, who are now playing a pivotal role in enabling the AI era.

The AI Data Centre: A Memory-Driven Architecture

AI workloads are fundamentally different from traditional enterprise applications. Instead of simple transactional processing, AI systems require:

- Massive datasets to train models

- High-throughput pipelines to feed GPUs

- Ultra-low latency access for real-time inference

This creates a new bottleneck: data movement. Even the most powerful GPUs cannot deliver results if they are starved of data. As a result, modern AI data centres are increasingly designed around memory bandwidth and storage performance, not just compute power.

DRAM: Feeding the AI Engine

DRAM remains the primary working memory in AI systems, where active datasets are processed.

In AI environments, particularly those using GPUs and accelerators, high-bandwidth memory (HBM) and advanced DRAM architectures are essential because they:

- Provide the ultra-fast access speeds required for model training

- Enable parallel data processing across thousands of cores

- Reduce latency in inference workloads

Micron has been aggressively innovating here, with its HBM roadmap delivering significant performance gains and improved power efficiency, critical in energy-constrained data centres.

As AI models scale, DRAM demand is surging. Not just in volume, but in performance class. This is one of the reasons the wider memory market is shifting heavily toward AI-focused infrastructure.

NAND & SSDs: The Backbone of AI Data Pipelines

While DRAM handles active workloads, NAND flash and SSDs underpin the data pipeline, storing, staging and delivering the enormous datasets AI systems rely on.

Micron’s latest data centre SSD portfolio highlights how storage is evolving specifically for AI:

- PCIe Gen6 SSDs delivering up to ~28 GB/s throughput

- Ultra-low latency for real-time inference

- Massive capacity drives (100TB+) to support large-scale datasets

- Improved energy efficiency to reduce operational costs

These advancements are not incremental, they’re enabling entirely new architectures.

For example:

- Faster SSDs reduce the “data starvation” problem for GPUs

- High-capacity drives allow localised datasets, reducing network bottlenecks

- Better performance-per-watt helps manage AI’s growing energy footprint

In essence, SSDs are no longer just storage, they are an active part of the AI compute pipeline.

Breaking the “Memory Wall”

One of the biggest challenges in AI infrastructure is the so-called memory wall, the growing gap between compute performance and data access speed.

Micron is addressing this through innovations that blur the line between memory and storage:

- Leveraging ultra-fast NVMe SSDs to extend GPU memory capacity

- Creating hierarchical memory architectures where data moves seamlessly between DRAM and NAND

- Optimising latency and throughput across the entire stack

This approach is critical for large-scale AI models, where datasets exceed the limits of traditional memory systems.

Why This Matters for Data Centres

The implications for data centre operators, integrators and partners are significant:

1. Infrastructure is shifting from compute-centric to data-centric

AI success depends on how efficiently data can be stored, accessed and moved, not just processed.

2. Memory and storage are now strategic components

DRAM and SSD performance directly influence AI model efficiency, cost and scalability.

3. Energy efficiency is a competitive differentiator

AI workloads are power-intensive. Solutions that improve performance-per-watt are becoming essential.

4. Supply chains are realigning around AI

The industry is increasingly prioritising enterprise and AI demand over consumer markets, reflecting the scale of this opportunity.

Micron’s Strategic Position in the AI Era

Micron’s pivot toward AI-focused memory and storage solutions reflects a broader industry trend: the convergence of compute, memory and storage into a unified performance layer.

By investing heavily in:

- High-bandwidth DRAM (HBM)

- Next-generation NAND

- AI-optimised data centre SSDs

Micron is positioning itself not just as a component supplier, but as a critical enabler of AI infrastructure.

Final Thoughts

The AI revolution isn’t just about smarter algorithms, it’s about faster, more efficient data movement.

As models grow and workloads intensify, the role of memory and storage will only become more central. Micron’s innovations in DRAM and SSD technology are helping to remove bottlenecks, unlock performance, and ultimately turn data into intelligence at scale.

Everything I read tells me this memory boom is not going to be a one-year wonder but will run and run.

Below are the numbers to look for when Micron reports on Wednesday.

As far as I see it, there are three main numbers that will influence the stock’s reaction after the report. First of all, Micron has guided for Q3 revenue of $33.5B and 81% gross margin. The consensus is $35.07B. I believe we will see a figure close to $37B. Let me explain why.

When we were focused on Nvidia, we also started talking about the big hyperscalers wanting to disentangle themselves from a dangerous overdependence on this supplier. So, companies such as Amazon, Alphabet, and Microsoft have been internally developing their own compute chips. Amazon, in particular, has disclosed that its chip business’s turnover is roughly $50B, with $20B for external customers. While this is a threat to Nvidia, it is a tailwind for Micron. All these new chips need memory. And the bottleneck is where Micron stands. So, when I see the hyperscalers continually increasing their capex guidance, I think that more money is flowing into Micron’s pockets, rather than into Nvidia’s. On average, Micron has beaten revenue estimates by roughly 20% in the past four quarters. With momentum building, I would not be surprised to see revenues above $40B. But let’s remain conservative: $37B is quite achievable.

Gross margin is another metric that deserves attention. The progression is 36.8% in Q3 FY to 74.4% in Q2 FY26, and a Q3 FY26 guidance at 81%. Since HBM4 has premium pricing and margins, if the sales shift is confirmed, then I would expect gross margins closer to 83%. If the print comes around this number, a re-rating is likely because unit economics change.

Finally, the key item: Q4 and FY27 guidance. Most investors expect a beat right now. But what they don’t know is how long this bonanza will last. My answer is: look at the hyperscaler’s capex. Last quarter, CEO Sanjay Mehrotra said that Micron’s

“fiscal Q3 single quarter revenue guidance exceeds the full year revenue for every year in our company’s history through fiscal 2024.”

This is the impact of the 4-to-1 catalyst. From an HBM4-DRAM trade-off ratio, it has become the new revenue multiplier, where the company makes in one quarter what it used to earn in one fiscal year.

Micron reported $37B in H1 revenues. When we add another $37B, we end up with $74B for the first nine months of the year. Clearly, $100B is in sight, but the goal for the end of the year will be at least $115B. If Micron guides above this threshold, it will be yet another tailwind for the stock.

Valuation

The stock is volatile, and I am assuming $1,150 as the share price to discuss the valuation. The FY27 EPS estimate is $61.24, which means that the stock is trading at a fwd PE of 18.7. I believe its fwd multiple is lower. In fact, the consensus still doesn’t embed the figures that will be released in a few days. If Micron reports $37B in revenues, its net income margin could land close to 55%. This means that we will be talking about $16.65B in net income, equal to EPS of $18, assuming 1.13B shares outstanding. This brings the 9M figure to $31.13. Since I am also expecting Q4 net income to be around $23.2B and Q4 EPS to be $20.54. The overall FY26 EPS figure is $51.67, which means the current fwd PE is 22.3. But this sets the base for FY27, where Micron should benefit from the ongoing hyperscalers’ capex boom. Therefore, I expect the company’s EPS to grow by 60% (by the way, analysts are forecasting 95% growth) to $82.67. This compresses the FY 27 PE to 14.1. Yes, the stock has done extremely well, but among the hot AI names, its valuation is extremely compelling. This is why I would increase ahead of the report, and, in case a buy-the-rumor/sell-the-news pattern materializes, I would use the dip to add.

Let’s remember that memory stocks are not the only game in town.

I had a look at the corporate profile which left me baffled.

Tower Semiconductor Ltd. (NASDAQ/TASE: TSEM), the leading foundry of high-value analog semiconductor solutions, provides technology, development, and process platforms for its customers in growing markets such as consumer, industrial, automotive, mobile, infrastructure, medical and aerospace and defense. Tower Semiconductor focuses on creating a positive and sustainable impact on the world through long-term partnerships and its advanced and innovative analog technology offering, comprised of a broad range of customizable process platforms such as SiGe, SiPho, BiCMOS, mixed-signal/CMOS, RF CMOS, CMOS image sensor, non-imaging sensors, displays, integrated power management (BCD and 700V), photonics, and MEMS. Tower Semiconductor also provides world-class design enablement for a quick and accurate design cycle as well as process transfer services including development, transfer, and optimization, to IDMs and fabless companies. To provide multi-fab sourcing and extended capacity for its customers, Tower Semiconductor owns one operating facility in Israel (200mm), two in the U.S. (200mm), two in Japan (200mm and 300mm) which it owns through its 51% holdings in TPSCo, and shares a 300mm facility in Agrate, Italy with STMicroelectronics.

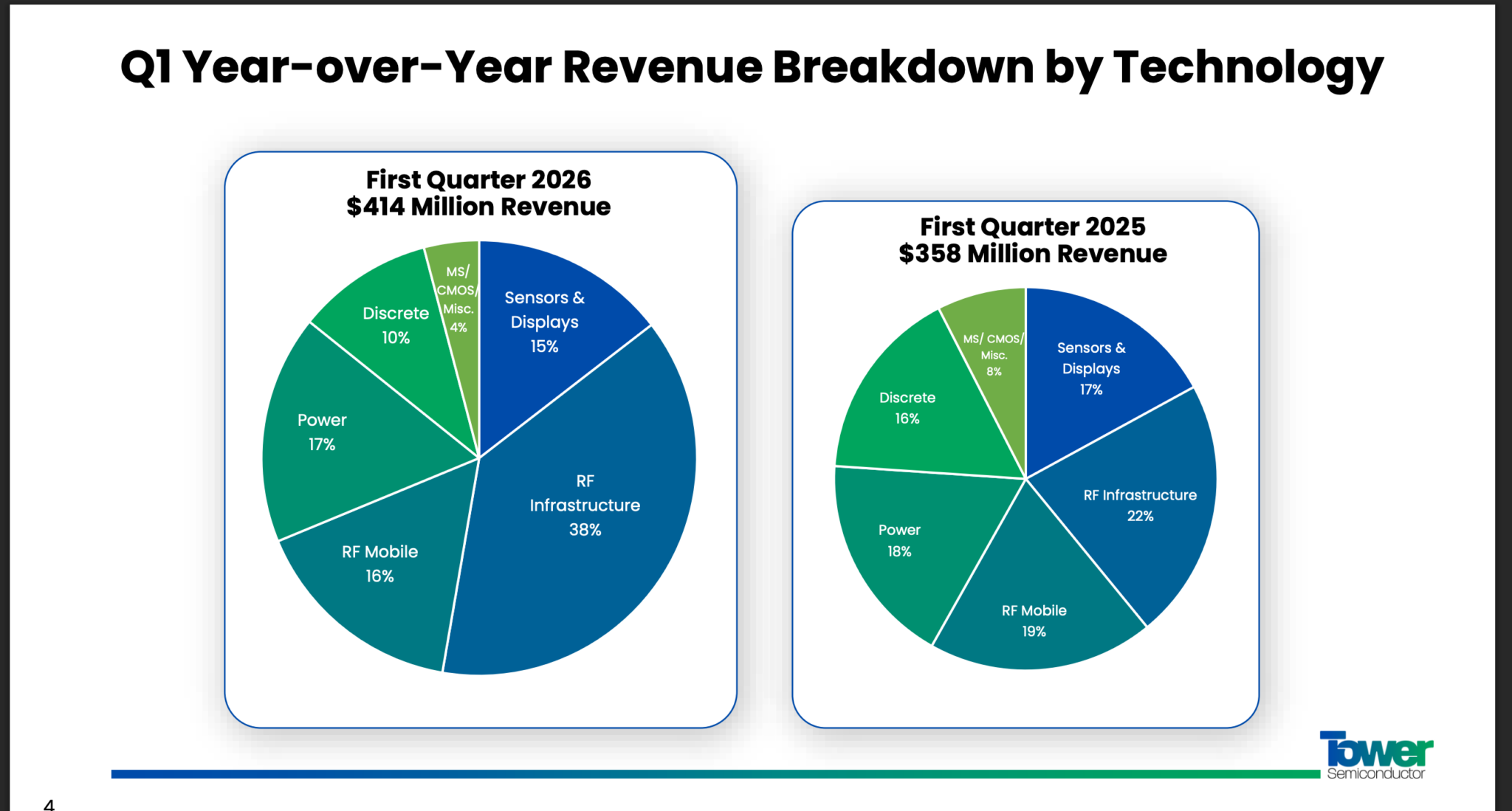

Big on tech, though, which is what we want these days, in an age of technology. The stand out in the slide below is that something called RF Infrastucture is growing at an incredible rate.

So what. is RF Infrastructure.

RF (Radio Frequency) infrastructure is the physical hardware, software, and transmission medium used to generate, transmit, receive, and manage radio waves. It acts as the backbone for all wireless connectivity, linking stationary networks to mobile devices, broadcast stations, and satellites.

Key Components

RF infrastructure consists of interconnected hardware that processes high-frequency signals:

- Transmitters & Receivers: Devices that generate and capture radio signals.

- Antennas: Convert electrical signals into electromagnetic waves for wireless travel, and vice versa.

- Amplifiers & Filters: Boost signal strength over long distances while isolating specific frequencies to prevent interference.

- Cabling & Connectors: Specialized coaxial cables and fiber optics (such as CPRI links) that transport RF signals between physical units.

Core Applications

RF infrastructure is the invisible scaffolding for several vital systems:

- Cellular & Mobile Networks: The macro towers, small cells, and base stations required for 4G and 5G communications.

- Broadcasting: The physical arrays used by commercial radio and terrestrial television.

- Public Safety & Transit: Mission-critical Land Mobile Radio (LMR) networks used by police and firefighters, as well as in-tunnel and trackside communication systems used by metros.

I am struggling to understand what is happening at Tower Semicnductors except that its growth engines are in explosive growth mode and, yet again, it is linked to the AI/ data centre buildout.

Moving specifically to first quarter of 2026 performance. This year has begun in a very strong fashion, led by Silicon Photonics with a revenue growth of 3x year-over-year, all major technology offerings demonstrated year-over-year growth with imagers up 9%, RFSOI up 12%, power management up 10% and silicon germanium up 24% year-over-year. Please see Slide 4 as reference for Q1 revenue breakdown by technology.

Focusing on RF infrastructure, last quarter was truly amazing, both in our team’s execution of aggressive capacity expansion as well as in demonstrating new breakthrough technology milestones. First, we continued a strong ramp of 200 gigabit per second products for multiple customers while continuing to support strong demand in older products by taking full advantage of new capacity coming online. We are in the midst of a SiPho production ramp in each of Fab 2 Migdal Haemek, Fab 3 Newport Beach, Fab 9 San Antonio and Fab 7 Uozu Japan 300-millimeter. Among this, we successfully achieved in Q1 first flow cycle revenue shipments from both Fab 2 and Fab 7, the latter having achieved impressive 95% yield for the first SiPho wafers leaving the factory.

Our expansion remains on track to grow SiPho capacity 5x from the base of our Q4 ’25 wafer revenue shipments by the end of this year 2026. In 2027, we anticipate our focus will turn primarily to additional 300-millimeter capacity expansion in the Uozu factory supported by the expected full factory ownership.

An important thing to note is that when certain parts of a business enjoy explosive growth the overall growth rate tends towards the growth being achieved in the fastest growing parts of the business. Tower is part of a sector doing well and I shall be doing my best to understand better what is happening and look at other opportunities in the sector.

Another look at what they do.

Tower Semiconductor is a specialty foundry that manufactures highly customized, analog, and mixed-signal semiconductor chips rather than standard digital processors. They operate global manufacturing facilities, producing specialized components for over 300 customers across automotive, industrial, medical, and mobile markets.

Their primary technology and manufacturing capabilities include:

- Silicon Photonics (SiPho): A key growth area for AI infrastructure, allowing data to be transmitted and manipulated using light.

- Radio Frequency (RF) & Silicon Germanium (SiGe): Powering wireless communications, high-speed data networks, and active optical cables.

- Power Management: Highly efficient chips designed to manage and reduce power consumption in mobile and consumer devices.

- CMOS Image Sensors: Specialized sensors used in industrial machine vision, medical devices, and automotive camera systems.

- Design Enablement: Offering specialized Design Services and process transfer optimization for fabless companies.

It is hard to tell if this is mainly about the AI infrastructure build out or whether we are seeing signs of another boom develloping related to all kinds of devices, perhaps as they adapt to the world of AI. WE are all accustomed to smart TVs; perhaps what we are seeing is everything becoming smart which puts a premium on connectivity solutions.

So here is another take on what they do.

Tower Semiconductor is not purely a “connectivity business,” but it is a leading specialty semiconductor foundry that manufactures the critical hardware (like Silicon Photonics and SiGe chips) that powers high-speed data networks, optical transceivers, and AI infrastructure. [1, 2]

Core “Connectivity” Capabilities

While they don’t sell consumer networking products themselves, they are the key manufacturing partner for companies building the backbone of global connectivity: [1]

- Silicon Photonics (SiPho): They produce high-performance optical modules and transceivers (such as 1.6T and 400Gbps) used by major tech leaders to speed up data-rate throughput in AI infrastructure and data centers.

- Silicon Germanium (SiGe): They are a premier foundry for SiGe chips, which are heavily relied upon for high-speed data transmission, RF (Radio Frequency) communications, and aerospace applications.

Their Primary Business Model

Instead of designing their own chips, Tower Semiconductor operates as an independent specialty foundry. They provide custom manufacturing, process technologies, and design enablement services to other tech companies, fabless semiconductor firms, and system builders.

Aside from connectivity, their customized analog manufacturing platforms also cater to a wide array of other growing markets, including:

- Power Efficiency: Integrated power management chips.

- Smart Systems: CMOS image sensors (CIS) and micro-electro-mechanical systems (MEMS).

- Automotive & Medical: Non-imaging sensors and high-performance analog solutions.

Two things are indisputable. They are very excited as a company about their prospects. The chart looks explosive. That’s good enough for me to start building a position and using that as a base to learn more about the business.

Share Recommendations

Tower Semiconductors. TSEM

Below is an insight into what Tower does.

Tower Semiconductor indirectly works with Credo Technologies. Since Credo is a fabless semiconductor company, they do not manufacture their own chips. Credo’s manufacturing goes through foundry partners, and they rely specifically on Tower Semiconductor’s silicon photonics foundry capabilities to produce wafers for their optical interconnect products.

This manufacturing relationship became even more direct when Credo acquired DustPhotonics. DustPhotonics is a silicon photonics company that uses Tower Semiconductor as its main wafer foundry. With the acquisition, Tower now serves as a key commercial foundry partner bringing Credo’s silicon photonics integrated circuit designs to life.