Three More Explosive Chart Breakouts – Seagate, Bloom Energy And Lumentum

Seagate has just reported figures that put a rocket under the shares in a sector (memory drives and storage) which is in one of the most explosive uptrends I have ever seen.

The statements coming from these companies could hardly be more positive.

Seagate delivered a very strong March quarter. underscoring both the durability of demand and the leverage in our model. We grew revenue 44% year-over-year, achieved record gross margins, more than doubled non-GAAP operating income and generated one of our highest ever levels of free cash flow at close to $1 billion. Momentum continues to build for our Mozaic HAMR-based platforms with 2 of the world’s largest CSPs now qualified on our 4+ terabyte per disk product. For both of these customers, qualification timelines were in line with PMR products, underscoring the maturity of the platform, and our team’s outstanding execution as we work to meet customers’ accelerated demand requirements.

Our strong Q4 guidance issued today demonstrates our growing conviction in the business and future opportunities. As we look ahead, we see Seagate now entering a period of structural growth. Our belief is rooted in 3 pillars. First is the sustainability of rising storage demand. AI-enhanced applications are accelerating data creation, expanding retention and increasing reliance on historical data sets for advanced reasoning, extending beyond cloud data centers to the enterprise edge, these trends require storage solutions that deliver cost and energy efficiency at scale, making high capacity hard drives essential to modern data center architectures. Second is our strategic technology roadmap.

Anchored by the Mozaic platform and HAMR innovation, we are delivering critical technology breakthroughs at the right time to support our customers’ rising demand now and into the future. Third is our proven strategy focused on converting demand into profitable growth and value creation. Our build-to-order model enhances demand visibility and supports pricing and supply discipline. Our HAMR-based product roadmap enables margin expansion as we scale. And our capital allocation framework enables us to leverage our earnings growth and cash flow generation into strengthening our balance sheet and enhancing shareholder returns over the long term.

The combination of these pillars, robust market demand, a proven technology roadmap and disciplined operational execution is already driving performance ahead of the financial targets outlined at our analyst event a year ago. The progress we have made gives us confidence to significantly increase our annual revenue growth target from the low to mid-teens, to a minimum of 20% over the next few years. This confidence is reinforced by the strength of the current demand environment shaped by ongoing momentum from cloud investments. The March quarter marked our tenth consecutive period of revenue growth from cloud customers, who have committed hundreds of billions of dollars in infrastructure CapEx investment to support their own long-term growth in AI transformations.

I am looking for shares in companies that tick all the boxes and in this market, that means explosive charts, explosive fundamentals and a story so strong it blows your socks off. The outlook for Seagate is amazing.

Using Remaining Performance Obligations, or RPO, as a proxy for future revenue potential, the top 3 global CSPs alone have nearly doubled their RPO to staggering $1.1 trillion, a clear indicator of sustained growth ahead. Assurance of reliable supply is our customers’ highest priority, particularly for nearline products, which accounted for close to 90% of total Exabyte shipments in the March quarter. We have Exabyte scale supply agreements in place with nearly all major cloud and hyperscale customers, with nearline capacity almost fully allocated through calendar 2027. At the same time, we are finalizing build-to-order contracts with these customers through the end of fiscal 2027, which defines specific configuration and pricing.

This chart breakout has just happened. These shares have miles to go. No wonder the shares are up over 14pc on the day.

Agentic AI pushes this even further, transforming sporadic engagements into autonomous workflows that continuously ingest inputs, generate reasoning and store durable outputs that are dramatically increasing data intensity and long-term storage requirements. AI is amplifying demand across existing applications such as video, where large cloud providers are integrating AI into platforms to boost user engagement and revenue opportunities, driving new video creation and the need to store it. We believe demand will further accelerate as AI applications move beyond the data center into the physical world, powering manufacturing systems, autonomous vehicles and robotics. These physical AI deployments generate massive data streams from sensors, cameras and telemetry with a single autonomous vehicle producing up to 4 terabytes per hour.

A portion of this data is reused for simulation, validation and retraining with retention requirements stretching 5 to 10 years to meet compliance standards. These inference-based applications are creating a growing need for both cloud and local storage. We have started to see interest from sovereign and neo cloud data centers for our enterprise nearline drives and system solutions. To manage these intensifying workloads, cloud and edge data centers deploy storage tiers that work in concert to optimize performance, cost, energy efficiency and data durability. Hard drives are critical to these modern data center architectures, delivering scalable capacity along with energy and cost efficiencies that form the foundation of the mass data storage tier.

Bloom Energy is at the forefront of a once-in-a-generation opportunity to become the global standard for onsite power.

Powerful stuff, but the company is walking the talk.

- Delivered 130% year-over-year revenue growth, driven by 208% product revenue growth

- Raised full year 2026 revenue growth guidance midpoint to ~80% year-over-year, up from prior guidance of ~60%

- Continued operating leverage, increasing gross margin and operating income guidance

The business is fizzing.

KR Sridhar, Founder, Chairman and Chief Executive Officer of Bloom Energy, said, “We at Bloom are ushering in the era of digital power for the digital age. Bloom is rapidly becoming the standard and “go-to choice” for on-site power.”

Simon Edwards, Chief Financial Officer of Bloom Energy, added, “Bloom is a generational company with differentiated technology, a compelling strategy, and a mission-driven team focused on disciplined execution. I’m excited help scale the business and support Bloom’s next phase of growth.”

I am a bit of a new boy as far as Bloom is concerned, although I have recommended the shares before. They are world-class for excitement.

I want to give you a perspective on why we are experiencing the hyper growth because it will shape how you think of Bloom going forward? For over 25 years, we built this company around the conviction that clean, reliable, affordable on-site power would become essential to a digital world. The market is now validating that vision at scale and AI power demand is simply accelerating it. Time to power has gone from a procurement consideration to an existential necessity. The company is driving the AI transformation are raising against each other on the one hand.

And on the other, bumping into the bottlenecks comment to building conventional infrastructure such as permissions, permits and community acceptance. The winner will be the one who can grow and deploy faster and on the schedule, the market demands. You see that’s a different game than the one the legacy power industry is set up to play. Their model is industrial.

Long cycle times, capital heavy capacity additions, product improvement measured over decades rather than quarters, our model is different at every layer we innovate and improve continuously, be it in our technology, in our product in how we manufacture in our capital intensity in how we deploy in how we operate and service our systems and in time to market. That is what allows us to deliver double-digit cost reductions year after year expand capacity with materially less capital than industrial era players and meet our customers’ schedule needs. Our differentiated and unique operating rhythm and mindset will be obvious to you if you visited our factory floor.

It’s a state-of-the-art production facility a busy construction zone and a buzzing innovation hub. We are manufacturing product on schedule to meet customer needs, adding lines and expanding capacity to meet growing demand and innovating to reduce cycle times, space needs and costs. Product manufacturing, capacity expansions and innovation, all occurring concurrently all the time, all under the same roof and all with factory floor team members and engineers working as 1 team for 1 common purpose. To be better tomorrow than we are today and keep marching towards the north star of maximum entitlement. This is an example of our operating model. We call it the Bloom way.

As a result of this approach, the contrast and outcomes is simple. Their supply to current orders arrive only in 2029 or later, irrespective of the customers’ needs. Hours arrived this year or the next or whenever the customer is ready. Based on demand profile, we have now shifted to adding capacity continuously. Hundreds of megawatts a quarter as opposed to lumpy one-off additions to be completed in a year’s time. How we think about and execute on capacity addition is one of the clearest ways to see what makes Bloom different. The traditional power industry has been the past 2 years, celebrating its backlog that is 4 and 5 years out.

Backlog at that scale and time frame in the age of AI is a result of their constrained supply. At Bloom, we see it differently. Our ability to expand capacity is our competitive advantage. We want to rapidly build capacity, build product help build productive AI factories to help build commercial and industrial facilities and help build our economy, not just be satisfied with simply building backlog. Our current manufacturing footprint will allow us to deliver 5 gigawatts of product annually. We will expand to that capacity and meet the delivery dates needed by our customers. In other words, today, we are not order constrained and not capacity constrained.

The pace of our revenue growth is decided by how fast our customers can build their greenfield sites, not how fast we can power them. We will never be a bottleneck to our customers. We built our business around that promise. Going beyond the 5 gigawatt capacity, our supply chain and manufacturing strategy and planning allows us to build that capacity significantly faster than any other option in the market using our copy exact model. We will strive to bring power to our customers faster than they can stand up their greenfield facilities. We were able to make that promise because we invested deliberately ahead of demand.

CEO and founder, K. R. Sridhar, says Bloom is at an inflexion point, and it certainly looks that way.

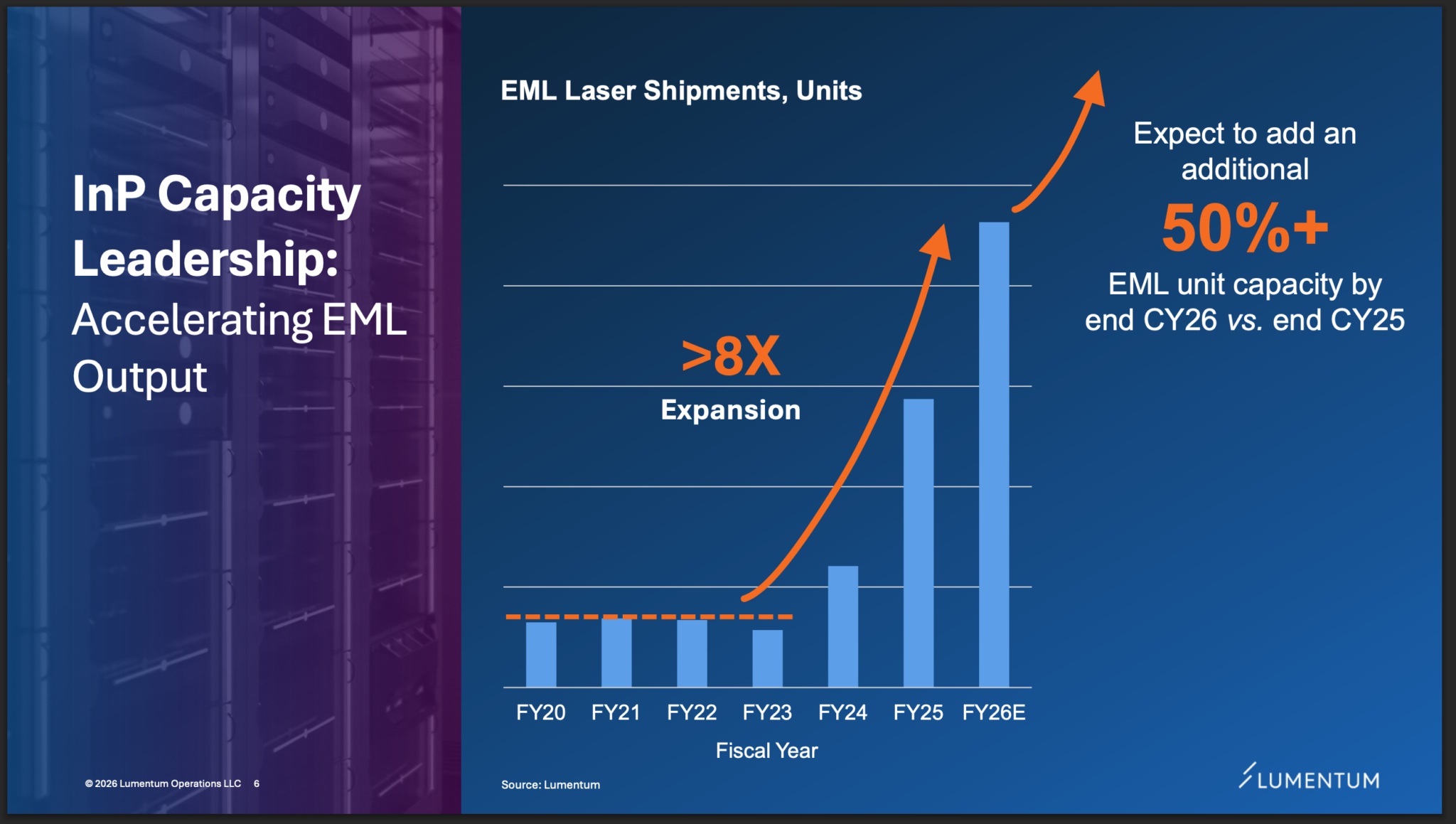

Below is a clue that exciting things are happening at Lumentum.

Another chart with a similar message.

Like other hardware stocks exposed to the AI revolution, Lumentum is on fire.

Lumentum delivered a standout second quarter with over 65% year-over-year revenue growth and non-GAAP operating margin increasing by greater than 1,700 basis points. At $665.5 million, we set a company record for quarterly revenue for the second reporting period in a row. We are now recognized as a foundational engine of the AI revolution. Virtually every AI network is powered by Lumentum technology, either through our direct hyperscaler partnerships or as the critical component supplier that enables our network equipment manufacturer customers. Our momentum is accelerating. While we previously projected crossing $750 million in quarterly revenue by mid-2026, we now expect to comfortably surpass that milestone next quarter.

Our March revenue guidance, with an $805 million midpoint, represents an impressive 85% plus year-over-year increase. We previously identified three primary catalysts for Lumentum’s future growth: cloud transceivers, optical circuit switches (OCS), and co-packaged optics (CPO). The headline for this quarter is that the vast majority of this growth is still ahead of us, and we have increased confidence as to the timing and magnitude of the ramps. While our Q2 results and Q3 guidance reflect meaningful contributions from cloud transceivers, we are only just beginning to unlock the massive potential of OCS and CPO.

Copper is the past; optical connectivity is the future.

While copper has long been the gold standard for scale-up for simplicity and cost, it is hitting a physical wall. An industry pivot is underway to bypass the scaling limits of copper. By late calendar 2027, we would expect our first scale-up CPO shipments replacing longer copper connections. We are already deeply embedded in design-in cycles for this, leveraging our ultra-high-power lasers and external light source modules. As we look into the not-so-distant future, it is only right to assume that optics begins to capture more and more of the connectivity, eventually subsuming copper. In response to these demand projections, we have initiated proactive capacity planning.

Having discussed the many exciting things happening at Lumentum, CEO Michael Hurlston had this to say.

With all that said, we continue to believe that our current performance is only a precursor of things to come.

Below is an explanation, long but worth it, by someone, not me, who understands all this stuff, and it tells us why Lumentum has such a glittering future.

Those stocks have performed quite well this year, but Lumentum has put them and virtually every other company to shame— LITE is up more than 1300% in just the last twelve months! The obvious question is what turned the company from a decently sized optical supplier to one of the most valuable engines of the AI infrastructure build-out?

The answer is pretty simple (in explanation, not in practice)— consistent execution at the highest level of laser design and manufacturing. More on this later. Let’s take a step back and look at the products Lumentum offers and the niche it fills in the data center.

How to Network a Data Center

For those unfamiliar with how optical transceivers in a data center work and what they actually do, we’ll begin with a quick explanation-by-example. If you’re quite confident you grasp this already, you can skip to the section titled “Leading In Lasers.“

Imagine that you’re a software engineer at, say, Google (GOOG), and there’s a particularly annoying task, like formatting a YAML file, that you’d rather have AI do for you. You boot up Gemini (or Claude if you’re feeling a bit rebellious), upload your YAML file, and prompt it for the desired result, which, if you’re me, is probably something like “fix pls.” Your browser takes that request and sends it on a long (in terms of distance, not time, of course) road to the nearest Google data center, where it is staged for processing.

As soon as compute becomes available, your request is sent through a series of network switch tiers before finally reaching what is called a top-of-rack (“ToR”) switch, which, as the name suggests, sits at the top of a server rack. The job of this ToR switch is to pass instructions to the GPU nodes within the server telling them what computations to perform and to receive the results of those computations, shepherding them back up the switch hierarchy, then to the Internet then back to your browser. Easy, right?

Back in the olden days, before data centers got so massive and hot, copper was used for nearly every connection— it was used to connect the processors to the switches and the switches to other switches. However, copper has two major downsides in the modern data center: signal degradation and heat. Essentially, as transmission speeds go up, a signal sent over a copper medium degrades over a shorter distance, limiting viability. For example, at next-generation 1.6T (terabits per second), copper can only maintain the integrity of a signal up to about 1 meter.

An innovation by Credo within the last few years has been to create what is called an active electrical cable (“AEC”), which has digital signal processors (“DSPs”) at each end of the cable in order to boost the electrical signal, increasing the maximum distance to ~5-7 meters at 1.6T, depending on use case and cable quality. While this has certainly extended the lifespan of copper, every time transmission speed doubles (every 2-3 years), these max lengths will be cut in half again. The “copper wall” is coming.

Enter, lasers.

Sending signals with lasers over fiber has been around since the dawn of the data center— photons don’t lose nearly as much signal integrity as electrons, making them perfect for long-haul connections. However, lasers have two downsides that make them ill-equipped for shorter distances: 1) cost and 2) power. For 1), copper is dirt cheap, so data center operators will always prefer to use it if possible. For 2), computers only understand electrons, which means to move data around with lasers, inputs and outputs have to be converted from electrons to photons, sent where they need to go, then converted back. That uses a ton of energy.

But, as hyperscalers have seen the writing on the copper wall, the math has changed. The first copper casualties were the inter-rack connections between switches— as data centers expand their footprints and dissipating heat becomes a primary concern, server racks are getting further away from each other. AECs might keep inter-rack doable for copper at 1.6T, but at 3.2T, expected in 2028, these connections will almost surely be lasers.

Just a note, when I say “lasers,” I’m specifically referring to an optical transceiver, which is a fancy way of saying the entire package that takes electricity, converts it into light, and then converts it back. In a modern pluggable transceiver, this usually includes various components to convert between electricity and light, a DSP at each end to clean, amplify, and regenerate the signal, and a fiber conduit for the photons.

But this isn’t the shift that has catapulted optical into the limelight; as the performance and heat of these systems increase, copper is fast losing ground within the server, which is known as the intra-rack domain as well. The first area this is happening and accelerating is in the connections between the GPU nodes and the switch— passive and active copper cables are being replaced by pluggable optical transceivers using lasers to send data instead of electrons. However, the pace of innovation is such that even these are now being replaced by a technology that has recently stepped out from the shadows and into the spotlight: silicon photonics (SiPho).

Before an explanation, let’s discuss the root cause. A primary problem in the current optical landscape is that, when a processor wants to send output to the switch, it needs to send an electrical signal over copper links to the edge of the PCB, where that signal is converted into light by an optical transceiver with a power-hungry DSP and then converted back to electricity by either the switch itself or another DSP. The heat generated by pushing a signal through copper at higher transmission speeds and by maintaining these DSPs is more than these systems can effectively dissipate at higher speeds.

Silicon photonics, broadly, is the idea that we can replace the copper links on a PCB with silicon and send photons over that substrate instead of electricity. This has previously been too expensive to be worth implementing but is now becoming a necessity because it enables what is being dubbed co-packaged optics (“CPO”). Using SiPho, the optical engines can be fabbed either directly onto the same silicon as the processor (this is CPO) or onto a separate piece of silicon that sits right next to the processor (near-port optics or NPO).

This allows the system to convert GPU output from electricity into light immediately, which can then be beamed straight out to the switch. This cuts out the copper links in the PCB and also allows for a much leaner DSP because the higher signal integrity of light over fiber vs. electrons over copper means the signal doesn’t need to be cleaned and amplified to the same extent. By some estimates, CPO reduces power consumption by 30-50%, which in the age of AI is well worth the cost.

Okay, there you have a slightly comprehensive, extremely simplified view of how networking works in an AI data center! We should probably also discuss the stock, which is the subject of this article, at some point, so next on the docket is how Lumentum fits into this ecosystem.

Leading in Lasers

In our overview of data center networking, I glossed over the “lasers” part of the optical transceivers to keep things high level, but, in reality, these are extremely complex and precise machines that require a highly specialized supply chain to manufacture. Lumentum is one such manufacturer.

The company’s main products include:

- In-house pluggable optical transceivers using electro-absorption modulated lasers (EMLs).

- Silicon photonic modules, known as photonic integrated circuits (PICs), that can be co-packaged within other suppliers’ processors and switches, using continuous wave (“CW”) lasers.

- The individual EML and CW lasers, which are sold to other equipment manufacturers to make their own transceivers.

Holy heck, that was a lot of acronyms.

The main takeaway you should get from this list is that Lumentum sells the products that data centers are heading towards in the next few years.

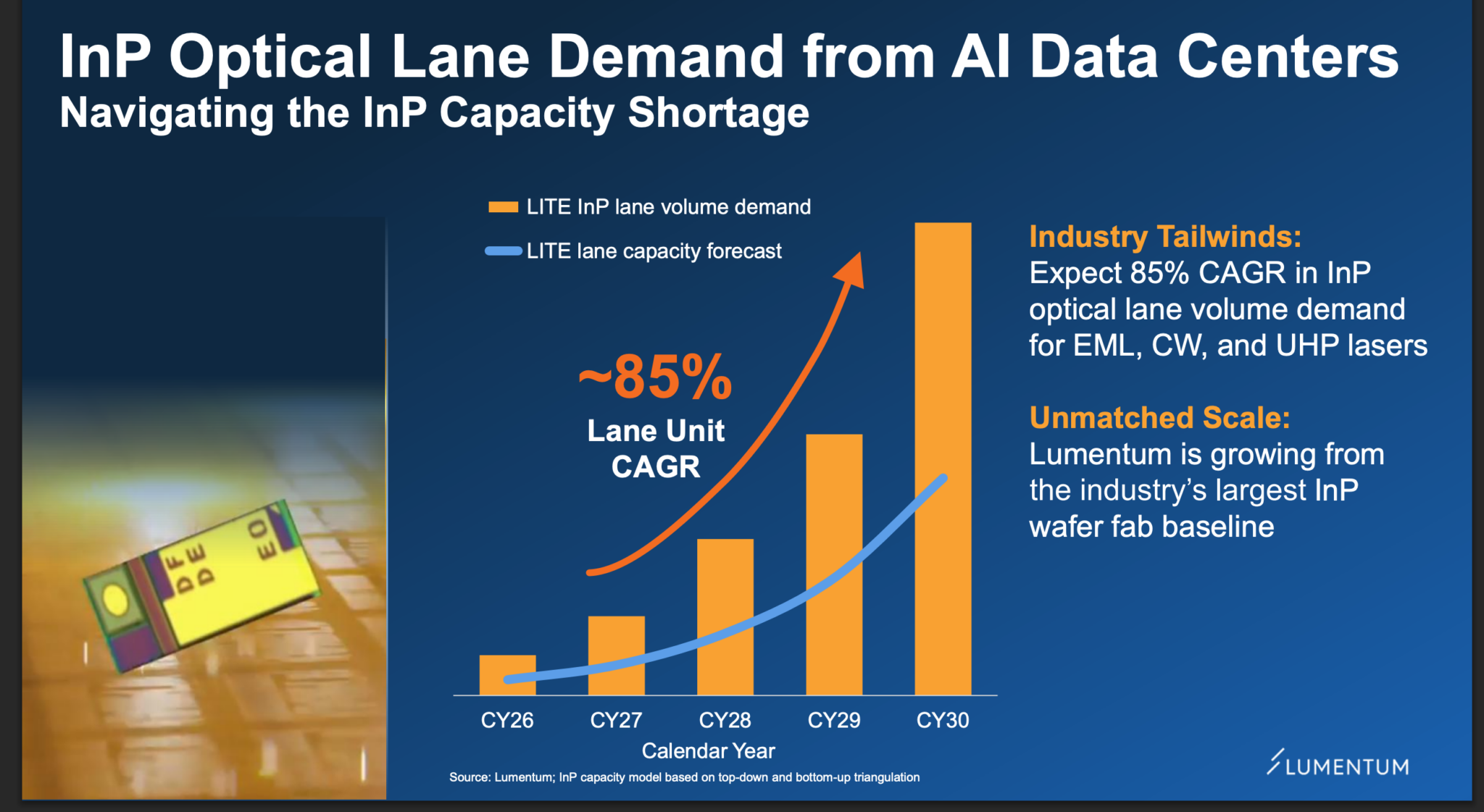

Right now, pluggable transceivers with EMLs are in high-demand and short supply, as Lumentum is really the only volume manufacturer of EML for 1.6T networks, which has contributed significantly to increasing revenue and margins.

We’re seeing this across the industry— supply is short nearly everywhere you look, but the cutting-edge is sold out potentially years in advance. In the most recent earnings call, CEO Michael Hurlston said the following in response to a question about pricing and demand in 2026 and into 2027:

Yes. I mean look, we really are sold out. I mean I think that we’ve talked about sort of trailing demand, even as we add capacity, it seems that the demand-supply imbalance increases. We talked about that last quarter. And I’d say again, even as we’ve added this 20% additional capacity, the demand, supply imbalance has increased.

1.6T pluggable transceivers and the EML lasers that make them tick are being sent to customers as soon as they come off the production line; this is the perfect environment for a company like Lumentum that sells at the very high end of the market because hyperscalers with deep pockets are usually willing to pay whatever it takes, especially when they’re all trying to win the AI arms race. The persistence of this shortage and the expectation for it to continue potentially for years is a big reason why LITE is soaring.

But EML is falling out of favor in most applications at higher transmission speeds because it’s expensive and difficult to manufacture, which has opened the door to silicon photonics sporting CW lasers.

First, SiPho PICs can be made with existing and widespread CMOS manufacturing, which is used to fab all manner of silicon, in contrast with indium phosphide-based EMLs.

Second, at 1.6T speeds, if you’re using an EML-based transceiver, all eight 200G lanes require a separate EML, whereas SiPho can accomplish the same eight 200G lanes with just two CW lasers.

Take both of these together, and I think it’s apparent why the industry is rapidly making this transition— silicon photonics is cheaper, easier to produce, and more energy efficient, all of which are AI data center imperatives.

What makes Lumentum so attractive is that it is successfully straddling both sides of the market and is raking in high-margin revenue from EMLs even as it benefits from the shift to silicon photonics. Hurleston summed it up well on the CC:

That being said, I still think, consistent with what we’ve said over the past, we would expect silicon photonics to be the majority of the transceiver shipments in — at the 1.6T node. We think the numbers are so large based on what we’re seeing in terms of the demand from our customers, that our EML shipments even in the face of a mix shift toward silicon photonics. The absolute number of EMLs will go up for us and rather appreciably. So we feel really, really good about the way the market is shaping up. Our lead on EMLs is second to none, we’re introducing 200-gig differential EMLs now to give us another leg up in that market. So we feel pretty good about the way that’s setting up.

So the product mix will shift towards SiPho at 1.6T (and likely even more at 3.2T), but EMLs will remain a significant part of the equation for years to come.

Lumentum is rapidly investing in additional capex to take advantage of the market opportunity, which is likely to lead to an increase in bottom-line numbers as the AI-induced supply-constrained environment continues. Expanding this manufacturing footprint was a significant factor in Nvidia’s $2 billion investment in LITE since, as the leader of the AI revolution, it has a vested interest in maintaining an ongoing supply of lasers to data centers. The deal also included a multi-billion-dollar purchase commitment that cements Lumentum as a key player in the future of the AI infrastructure build-out.

There is a lot to read, but if you are going to make a serious investment in Lumentum, and I think you should, it’s worth it. The author of the above thinks the shares are worth buying.

So, yes, the stock is trading at a forward P/E above 100, but operating results are accelerating quickly as optical adoption surges, and investors are pricing in years of growth beyond just the next four quarters. The run-up has been sharp, and volatility in this space will likely remain elevated in the short-term, but hyperscalers have committed to hundreds of billions of dollars in AI capex this year, which will likely turn into trillions over the next five years.

These build-outs will require optical components in ever-increasing quantities as the number of projects increases and the viability of copper recedes. It is this robust trend that I think will continue to lift shares in the medium-term even as the valuation appears stretched. I should note that this stock and the sector at large are not for the faint of heart right now— wild swings are a daily occurrence, and an industry pullback or macro headwinds could easily knock shares down by a substantial margin. However, I think those who don’t mind a bit of a rollercoaster and have at least a five-year time horizon for a LITE position can still jump in at current levels.

Share Recommendations

Seagate Technology. STX

Bloom Energy. BE

Lumentum. LITE

Another author puts the case for Lumentum more succinctly.

Lumentum Holdings Inc. (LITE) is having its NVIDIA Corporation (NVDA) moment.

The stock is up over 1400% in the last year, and with good reason.

This is a company that controls something fundamental to the next phase of AI, the movement of data.

While a lot of investors are still focused on compute, bandwidth is now the real problem.

As data centers push beyond 800G speeds, the industry is running into a hard physical constraint, which is the limitations faced by copper.

The only real alternative is optical solutions, and Lumentum sits at the center of that transition.

This is physics forcing a new layer of infrastructure into existence.

Just as GPUs and NVIDIA Corporation (NVDA) became unavoidable as AI workloads scaled and compute demand exploded, Lumentum is becoming unavoidable as the data that feeds those systems needs to move faster and more efficiently.

Like SanDisk, Lumentum is changing.

What has changed over the past year, and what the market is still catching up to, is how Lumentum’s role in the ecosystem has evolved.

This is a company that has historically been considered a cyclical supplier tied to telecom demand.

But like with so many other companies, AI has changed that.

Today, Lumentum is increasingly dealing directly with hyperscalers, who are choosing to source optical components independently rather than bundling them through integrated systems from companies like Nvidia.

The most important validation of this shift came recently, when Nvidia itself committed roughly $2 billion in strategic investment into Lumentum, alongside multi-billion dollar purchase commitments for advanced laser components.

The way I see it, Lumentum is no longer just a supplier in the ecosystem; it is now directly aligned with the most important company in AI infrastructure.

This is how hardware moats are built, not through software, but through deep integration into systems that are too complex and too critical to easily replace.

I am still learning about Lumentum, but it looks exciting. The key point with all three of these stocks is that they are the total package: explosive fundamentals, exciting story and near vertical charts, with breakouts as explosive as the fundamentals. In the moment, it is easy to wonder how they can climb anymore, and maybe, in the moment, they can’t, but a year or two from now, they could be massively higher. I expect they will be.