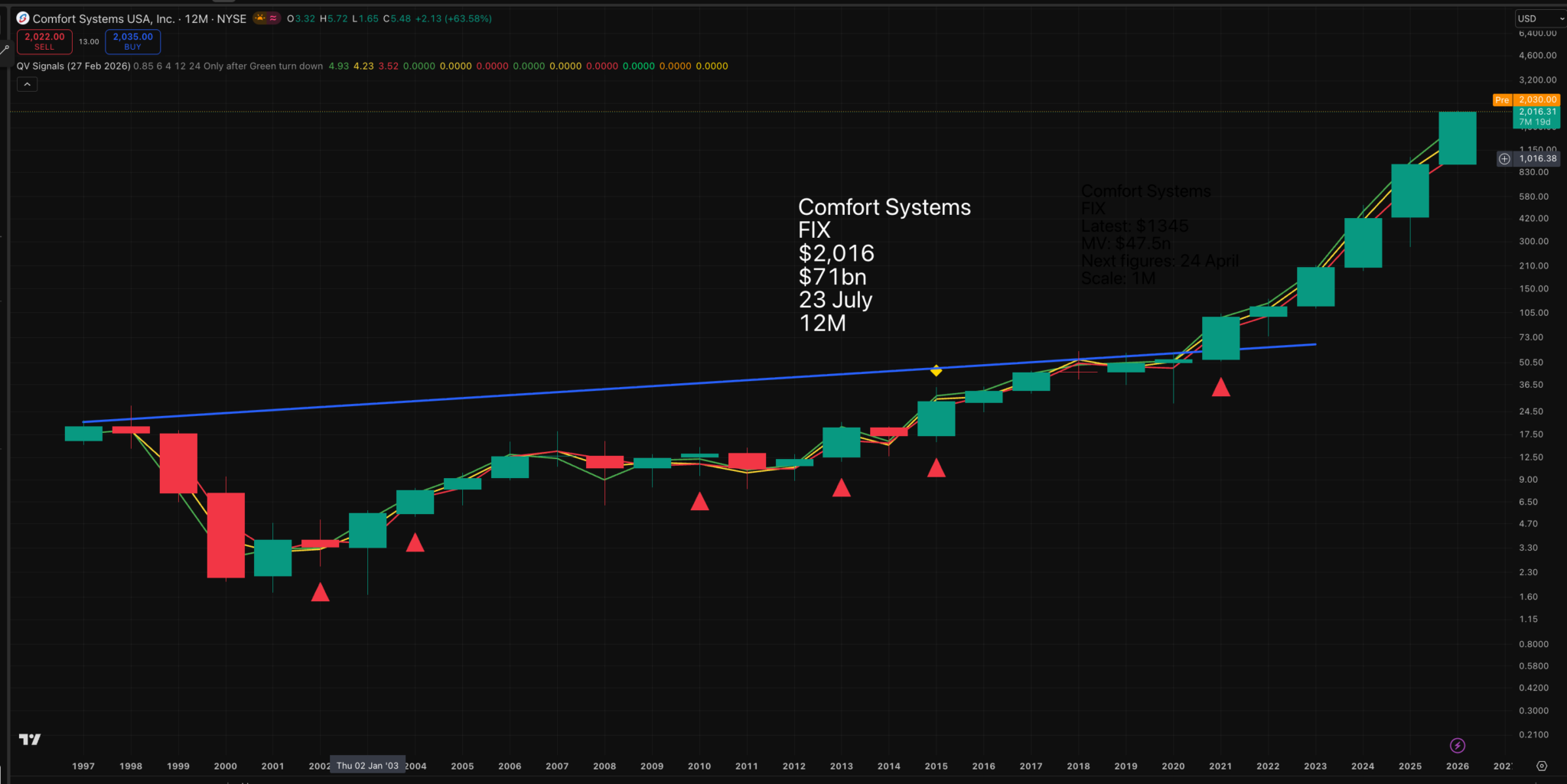

At one level, Comfort Systems (FIX) is about plumbers and electricians, but that doesn’t explain a market value of $71bn and climbing. Two other things are happening. One is that (FIX) is an acquisition machine. And secondly, AI and the data centre boom, which has added a huge and explosively growing source of demand.

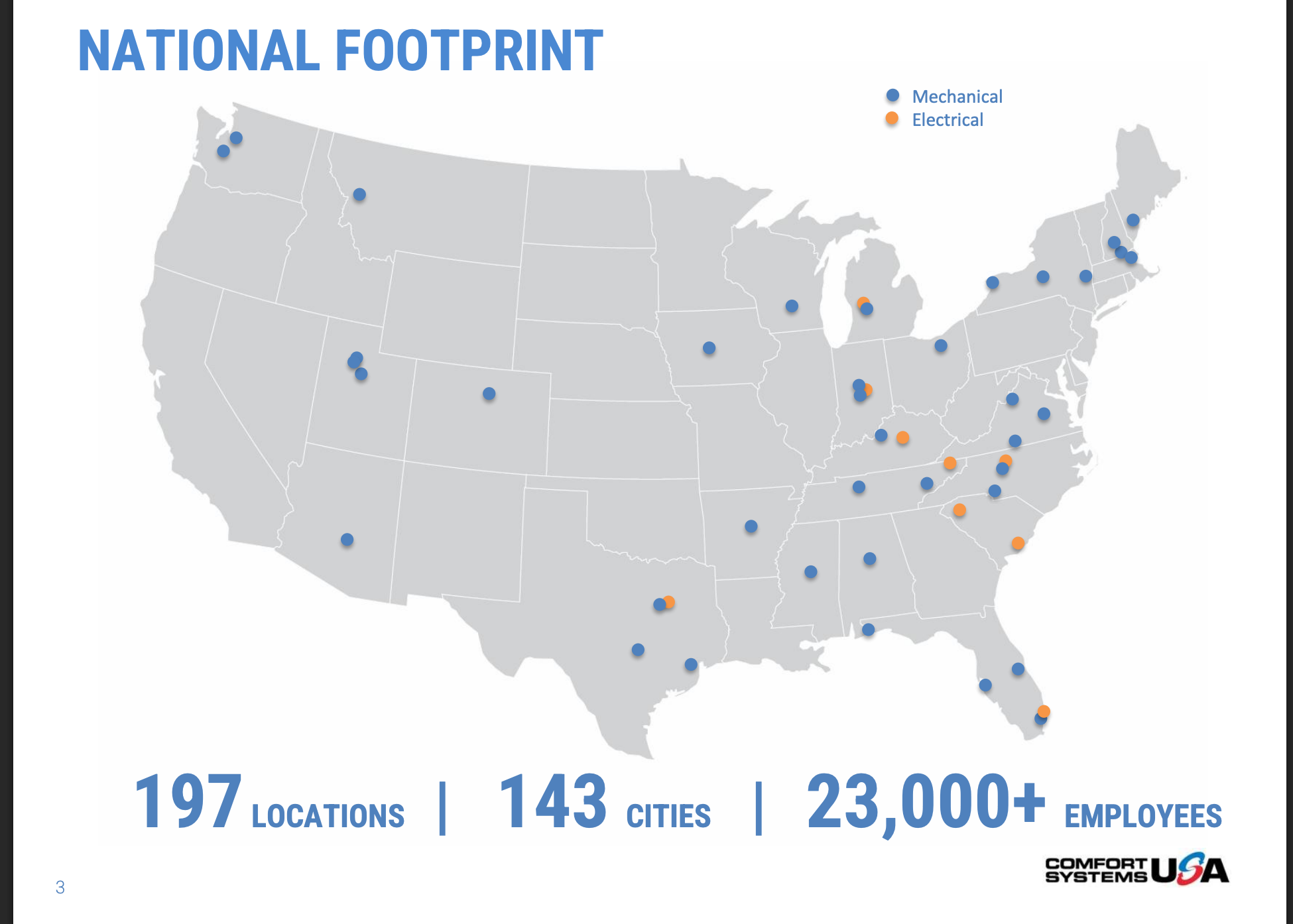

FIX has more in common with McDonald’s than with your local plumber, and they can handle massive jobs. Just look at the markets they serve and the trends from which they are benefiting.

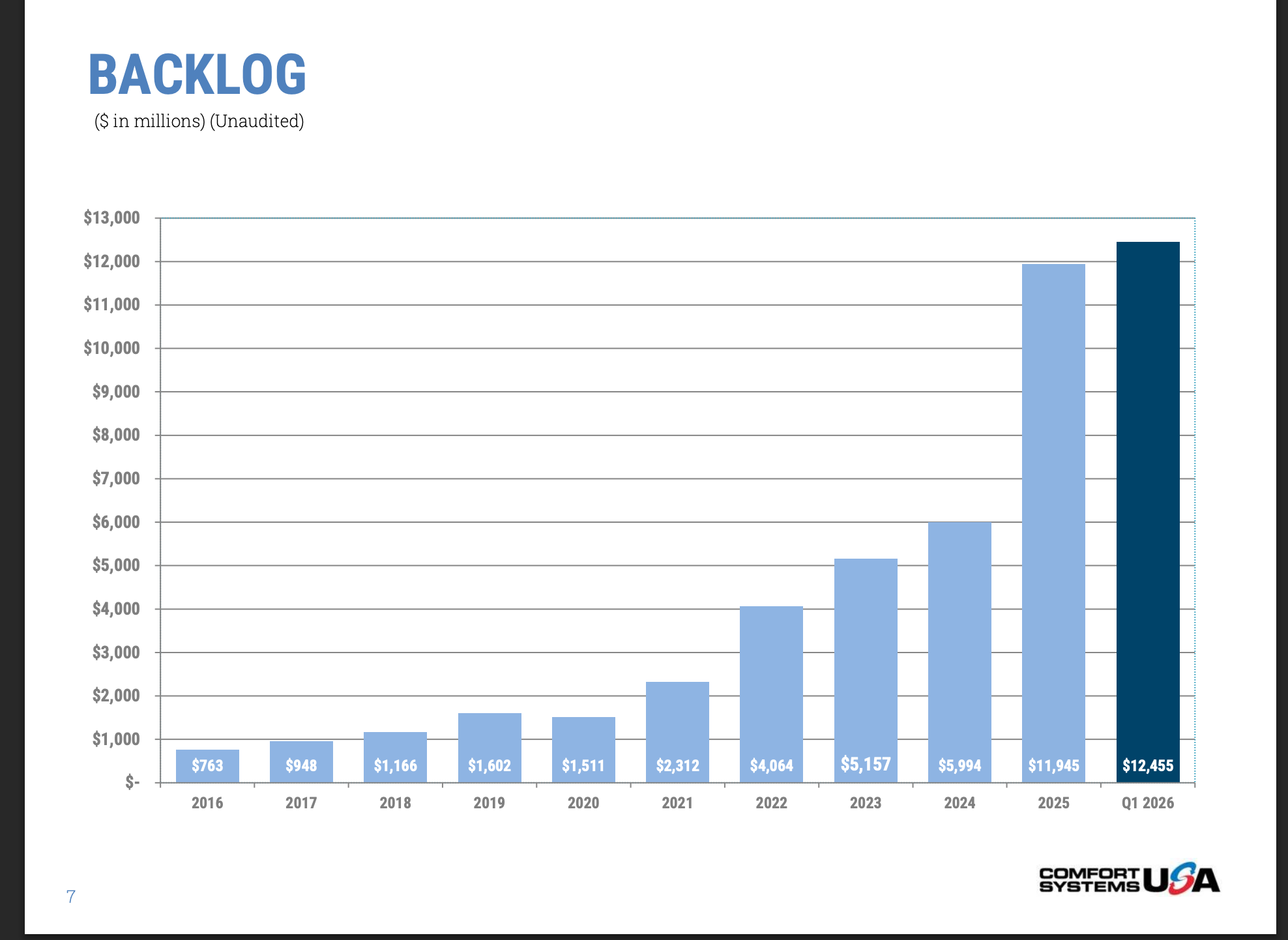

The next chart shows how the business has exploded. All the bars reflect annual growth except for the last one, which is for one quarter.

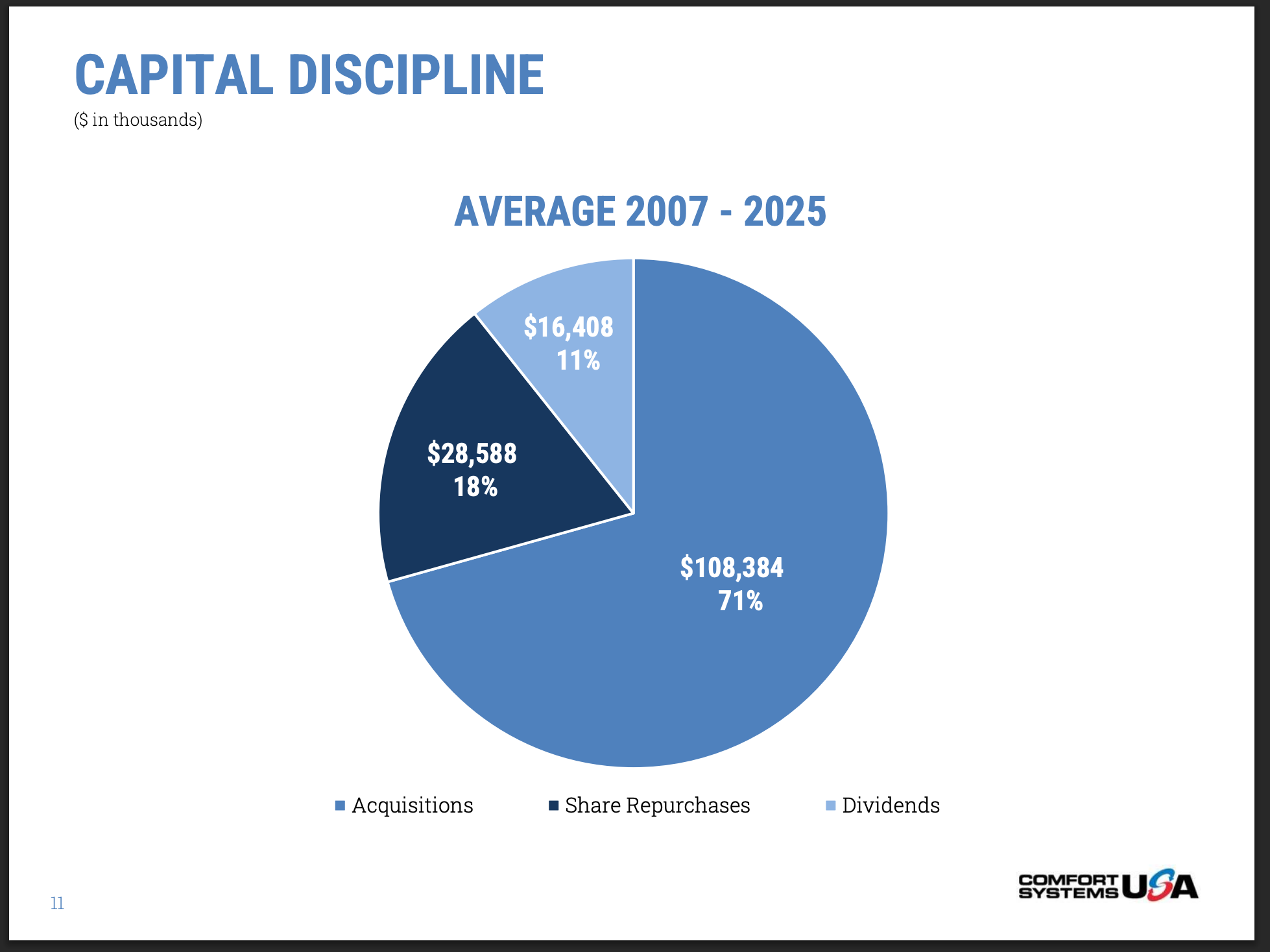

The next chart shows what FIX does with its cash flow. It is pouring money into share repurchases and dividends, which benefit shareholders immediately, and acquisitions, which will benefit them in the future.

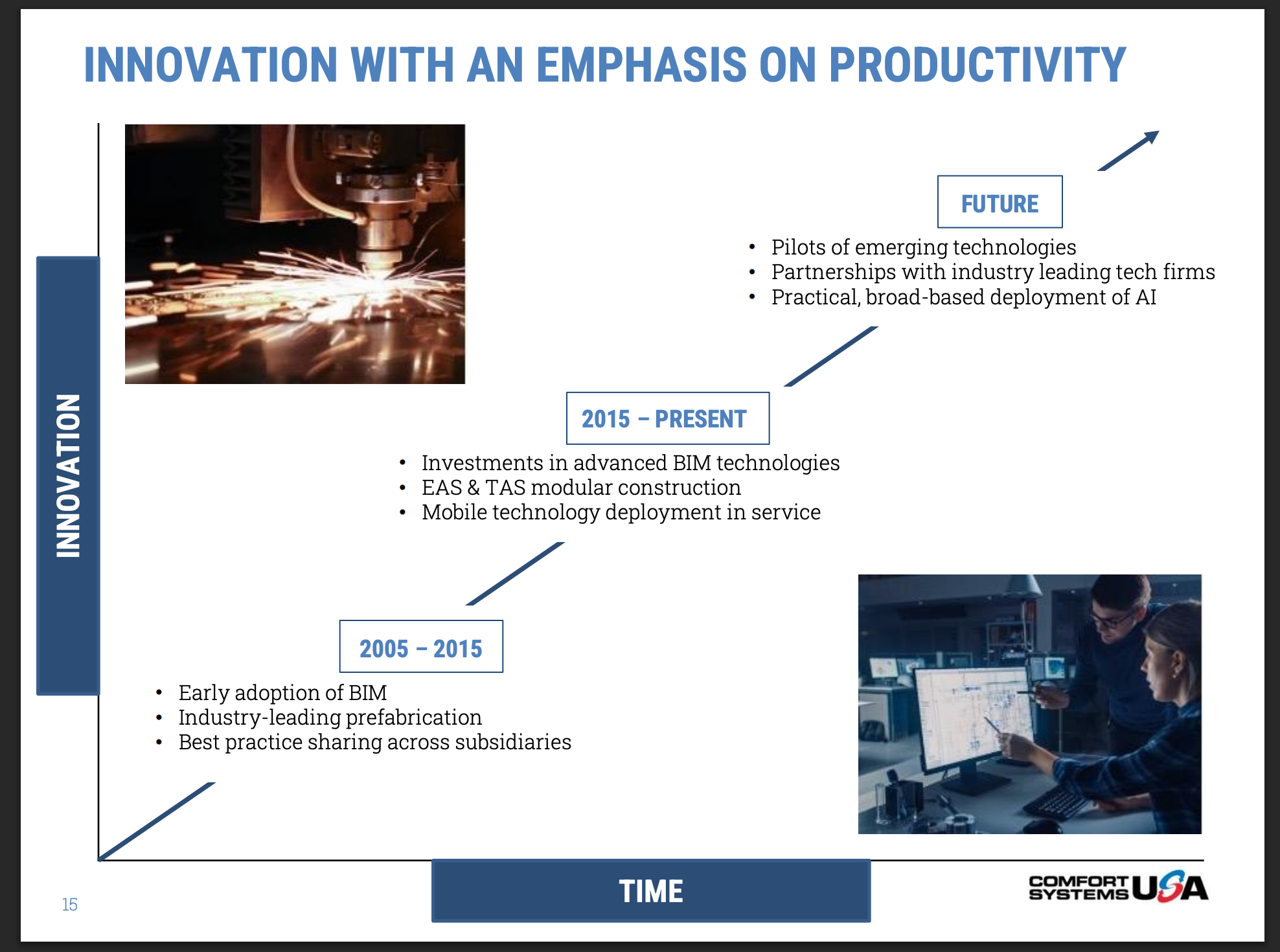

Like any good business, FIX is also embracing technology.

So what is BIM?

Building Information Modeling (BIM) is a collaborative, technology-driven process for creating and managing digital, information-rich 3D models of built assets (buildings, bridges, infrastructure) throughout their entire lifecycle—from planning and design to construction and operation. It ensures better decision-making by enabling teams to visualize, simulate, and exchange data-packed, intelligent models.

Key Aspects of BIM

- Intelligent Digital Models: Unlike simple 3D models, BIM objects contain embedded, data-rich information about physical and functional characteristics (e.g., material types, performance, manufacturer details).

- Lifecycle Management: BIM covers the entire process, including planning, design, construction, maintenance, and potential demolition.

- Collaboration: Architects, engineers, contractors, and owners work together on a shared model to reduce errors and improve efficiency.

- Types of BIM: Often includes 3D (design), 4D (time), 5D (cost), and 6D (sustainability) data, supporting better cost certainty and reduced waste.

Comfort System’s business is booming. This means that forecasts can be taken with a pinch of salt. Latest quarterly earnings were up 129pc. Full year forecasts are for eps around $40 rising to $50 for the year to end-August 2027.

Analysts are projecting a dramatic slowdown in earnings growth between 2026 and 2027. There are two reasons why this might be a massive underestimate. First, the company is extremely positive on prospects.

With unprecedented backlog and strong project pipelines, and given the confidence we feel in our best-in-class workforce, we expect continued strong performance in 2026. And we feel confident in our prospects.

Second is the potential impact of acquisitions. In the last 20-odd years, the company has made some 40 acquisitions. They are unlikely to stop now and have never had greater resources to do deals and a better market in which to build a bigger footprint.

I am going to make a wild guess. I think their earnings per share in the 2027/ 28 time scale, so one to two years out could reach or even exceed $100.

Share Recommendations

Comfort Systems. FIX

Strategy – Hardware Shares Look Too Cheap

Investors love, or used to love, until AI came along, software stocks. They delivered recurring revenues which grew and grew every year and had sustainable super high profit margins. AI has busted that model and created huge demand for all the hardware involved in the great data centre build-out.

But investors have a problem with hardware because they think it is a cyclical business. The minute it starts to boom, they worry about increased supply leading to a cyclical downturn. Palantir, a software business which looks less vulnerable to AI-inspired commoditisation, is valued at around 40 times expected 2026 revenues even after the shares have dropped sharply.

Makers of memory devices like Micron Technology and SanDisk are valued at less than 10 times sales, maybe much less, and even their prospective PE ratios are in single figures. Investors are super cautious about hardware shares.

Even Nvidia suffers from something of the same problem. Fiscal 2027 (year-end 31 January 2027) sales are expected to reach between $300bn and $400bn, and who knows, maybe $500bn is in prospect for the year to end January 2028.

I am pulling numbers out of a hat, but given the explosive expected growth in the markets they serve and prospects for physical AI in factories, autonomous cars and robots, coming on stream, my numbers are as plausible as anyone else’s. This means the shares could be on 11 times sales, and Nvidia is extremely profitable with an operating margin of around 66pc.

Whether that is cheap or not is like arguments about the length of a piece of string, but it does mean that the share price could rise significantly without making the shares look obviously expensive.

The fact is that investors are wary of the new hot sector – hardware, and there is scope for more optimistic valuations if investors become less cautious about business models which are being consciously changed by the companies to deliver more predictable earnings growth. Bottom line, there is a good chance of the whole sector being rerated.