As I write, shares in memory stocks are drifting lower even as the overall US stock market heads higher. This is understandable because they had become stupendously overbought, but to me, they look insanely cheap.

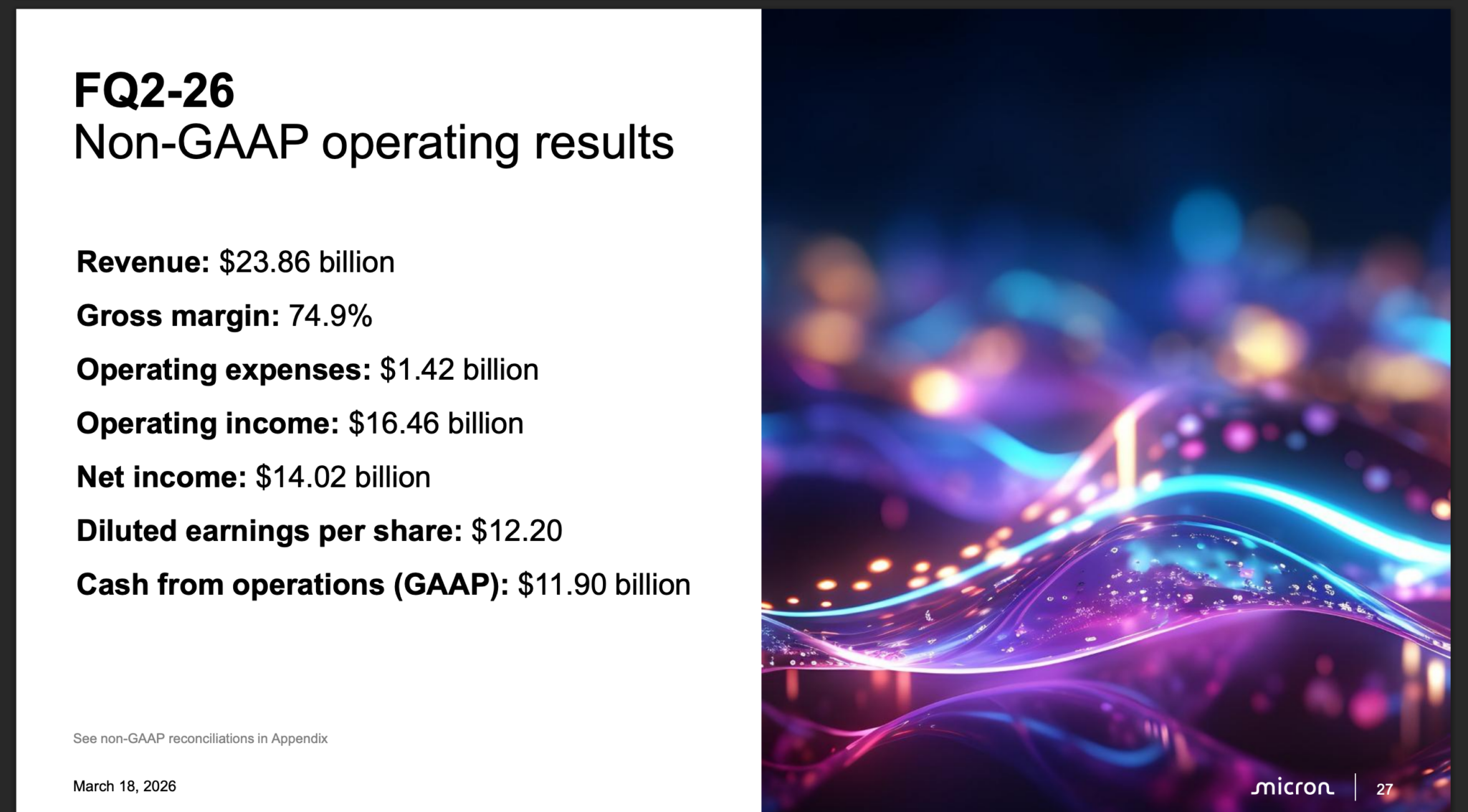

Take the example of Micron, which is growing so fast that in Q2 2026 (for a full year ending late August 2026), reported sales were higher than in any full year up to 2024. Sales are running at around $100bn a year. I am curious what they will be running at by the end of fiscal 2027, let alone by the end of fiscal 2028.

The company is blazingly bullish.

This implies no numbers, but quarterly revenue nearly tripled from its level a year earlier. If momentum like this is maintained, we could see revenue running at $200bn per year sometime in 2027.

Micron Technology is valued at $825bn. We could be looking at one of the world’s fastest-growing companies valued at four times sales. Many slower-growing companies are valued at 20 times sales.

Now look at these numbers.

Cash from operations is running at almost $12bn a quarter or close to $50bn a year. Such a tsunami of cash will transform the business; that is, almost $1bn a week. It is as though Micron Technology had jumped from the UK’s Football League One to competing in the Champions League in one season.

Nvidia’s free cash flow is running at around $100bn a year, and it is valued at $5.71 trillion. It is within the bounds of possibility that Micron’s free cash flow could be running at around $50bn or more a year from now since it reported $6.9bn of free cash flow for the latest quarter and is scaling rapidly. I am no analyst, so I am plucking these figures out of the air, but they are plausible. Combine the numbers being delivered by Micron with its statements on prospects, and the incredible boom in AI-generated demand for memory products, and I could even be conservative.

Micron is approaching $1000 a share (before the latest sell-off). I don’t see why they shouldn’t reach $5,000 a share on a relatively short-term time horizon. Maybe I am crazy. Maybe I am missing something, but if I am, I don’t know what.

That’s it; ‘that’s all’ as Miranda Priestly says to end conversations in The Devil Wore Prada.

Share Recommendations

Micron Technology. MU

Anything to do with memory (SanDisk, Seagate Technology, Samsung, SK hynix, Kioxia, Western Digital Corporation)

Strategy – Keep Taking The Pills

There can be amazing disconnects between share price behaviour and underlying fundamentals. All the memory companies insist that because of AI, their world has turned on its axis. Sales, profits and free cash flow are visibly exploding. Their hyperscaler customers are more concerned with supply security than with price. It’s the ultimate perfect storm.

It just seems to me from my little eyrie in Kensington that these shares are screaming buys. I think the main thing dragging them down is that they have risen so much. They had become fantastically overbought. But as soon as buyers and sellers have absorbed those gains, the shares will explode higher again and probably again and again.

The latest news on Friday is that memory stocks are being hammered; that is, stock markets for you. This has nothing to do with the fundamentals and is all about profit-taking. There is no one quicker to sell than an investor/ speculator sitting on fast-disappearing profits, especially in a news vacuum. As soon as we have reassurance from these companies that the boom is running as hot as ever, the shares will rebound.

Below is what Forbes Magazine has just said about Micron Technology. with the heading – ‘Why Micron Stock’s 9x Rally Might Just Be The Start’.

Micron Technology’s stock has increased by nearly 9x in the past year, raising its market valuation above $800 billion – marking one of the most substantial single-year increases in the company’s forty-year trading history. This increase is fueled by heightened demand and a deficit of high-bandwidth memory, the specialized chips that complement AI accelerators within data centers. Talk of a potential labor strike at Samsung has also added volatility. Micron has pre-ordered its entire HBM output until 2026 under binding contracts. Hyperscalers like Microsoft (MSFT), Alphabet (GOOG), and Meta (META) are expected to invest around $700 billion in AI infrastructure this year, with memory being a vital component throughout all phases of this development. The stock may also seem undervalued at just 14x projected FY ’26 earnings and 8x next year’s earnings. Nevertheless, the memory markets are highly cyclical. So how has the stock historically responded during downturns?

While cloud computing has significantly driven AI demand, the edge may be the next frontier.

How Memory Cycles Typically Collapse

The memory sector has experienced several significant price crashes over the last fifteen years, all stemming from the same fundamental issue. Establishing a new DRAM fabrication facility takes two to three years and requires tens of billions of dollars. After construction, the economics tend to favor operating it at full capacity, irrespective of the current price. Demand spikes, prices soar, manufacturers invest in additional capacity, and by the time this new capacity is operational, the market for which it was intended often no longer exists.

The 2022-2023 Memory Crash: The downturn from 2022 to 2023 was among the most severe in monetary terms. Demand diminished post-pandemic. Supplier stockpiles hit 31 weeks by early 2023. Micron reported a GAAP net loss of $2.31 billion within a single quarter, its highest to date; reduced its workforce by 10%; and drastically cut its capital expenditure. The stock dropped approximately 50% from the early 2022 levels, trading at about 11x forward earnings at its peak.

The 2018-2019 Inventory Adjustment: In 2018 and 2019, cloud operators over-purchased memory in 2017, subsequently reducing orders throughout 2018 as stocks grew. NAND prices fell by approximately 60%, and DRAM prices declined around 40%. Micron reached a peak of nearly $64 in May 2018, falling to about $28 by year-end, a decrease of roughly 57%. At the stock’s May 2018 peak of around $64, the forward price-to-earnings ratio based on fiscal year predictions was around 4.5x.

The 2014-2016 DRAM Decline: During the crash from 2014 to 2016, DRAM capacity had expanded in anticipation of PC demand that never materialized as consumers pivoted to mobile devices. Prices consistently fell throughout 2015. Micron’s stock plummeted roughly 70%, from around $37 in late summer 2014 to below $10 by February 2016.

What Sets This AI Cycle Apart?

Three structural elements differentiate the present landscape from previous upturns.

First, demand intensity. The demand for memory per AI system is no longer increasing linearly with deployment but geometrically. Nvidia’s (NVDA) H100 utilized 80GB of HBM, while its Rubin Ultra successor aims for 512GB per GPU module. Expanding model sizes further fuel this demand. Initially, HBM was predominantly used for training large language models (LLMs), but as of 2026, the focus has shifted towards inference, or executing models for end users. Applications like real-time video generation and sophisticated AI agents necessitate the ultra-low latency that exclusively HBM can provide.

Second, contract structure. HBM is increasingly sold through long-term commitments with hyperscalers instead of the spot market, which minimizes sudden order cancellations that have historically caused sharp price reductions. In March, Micron secured the industry’s inaugural five-year HBM supply agreement, encompassing both volume and pricing, which signals a transition towards more transparent, contracted revenue streams.

Third, supply limitations. HBM demands significantly more wafer capacity per bit than standard DRAM, while its production complexity restricts how quickly competitors can ramp up output. This constrained supply environment has allowed established firms like Micron to rapidly gain market share. Micron’s HBM revenue share increased from 9% of the global market in Q4 2024 to 21% in Q4 2025, while the overall HBM market approximately doubled during the same timeframe.

The Risk of Oversupply Remains

None of these factors dismisses the economic realities of semiconductor manufacturing. Micron has projected fiscal 2026 capital expenditures exceeding $25 billion, while SK Hynix is anticipated to spend around KRW 40 trillion, roughly $27 billion, as per S&P. Samsung Electronics is also pursuing aggressive expansion. Historical trends suggest that when all three primary memory producers increase capacity simultaneously, oversupply tends to arise within a two to three-year window.

Simultaneously, the cycle continues to hinge on sustained AI investments by hyperscalers such as Alphabet (GOOG) and Amazon (AMZN). If hyperscalers encounter pressure to deliver increased returns on their substantial capital expenditures, spending could decelerate, impacting memory demand directly.

There are risks with all investments, and Micron Technology is not immune. But the AI/ Datacentre revolution and associated infrastructure spending are orders of magnitude above anything that has ever happened before. It is conceivable, even likely, that supply will be chasing demand for years to come, creating powerful tailwinds for the memory industry.

At this point, I refer you back to the chart showing an explosive breakout from decades of consolidation. Nor is it just Micron. The whole sector is behaving similarly.

We will hear from Nvidia on Wednesday. I expect Jensen Huang to confirm that the AI infrastructure boom is running at full throttle. Remember also that so far the AI boom has been a digital phenomenon, but with robots, autonomous vehicles, unmanned warfare and automated factories all becoming or close to becoming present realities, an even bigger market is poised to open up.

Analysts and investors have been scarred by three massive downturns in the memory industry in the last decade, and everybody understandably dreads the expression – it is different this time, but sometimes it is. Remember the duck test, a classic of deductive reasoning. If it looks like a duck, swims like a duck, and quacks like a duck, then it probably is a duck.

This latest memory boom may be just another cyclical episode, but it feels very different and much more enduring to me and to the people who should know what they are talking about – the CEOs of key companies in the sector.

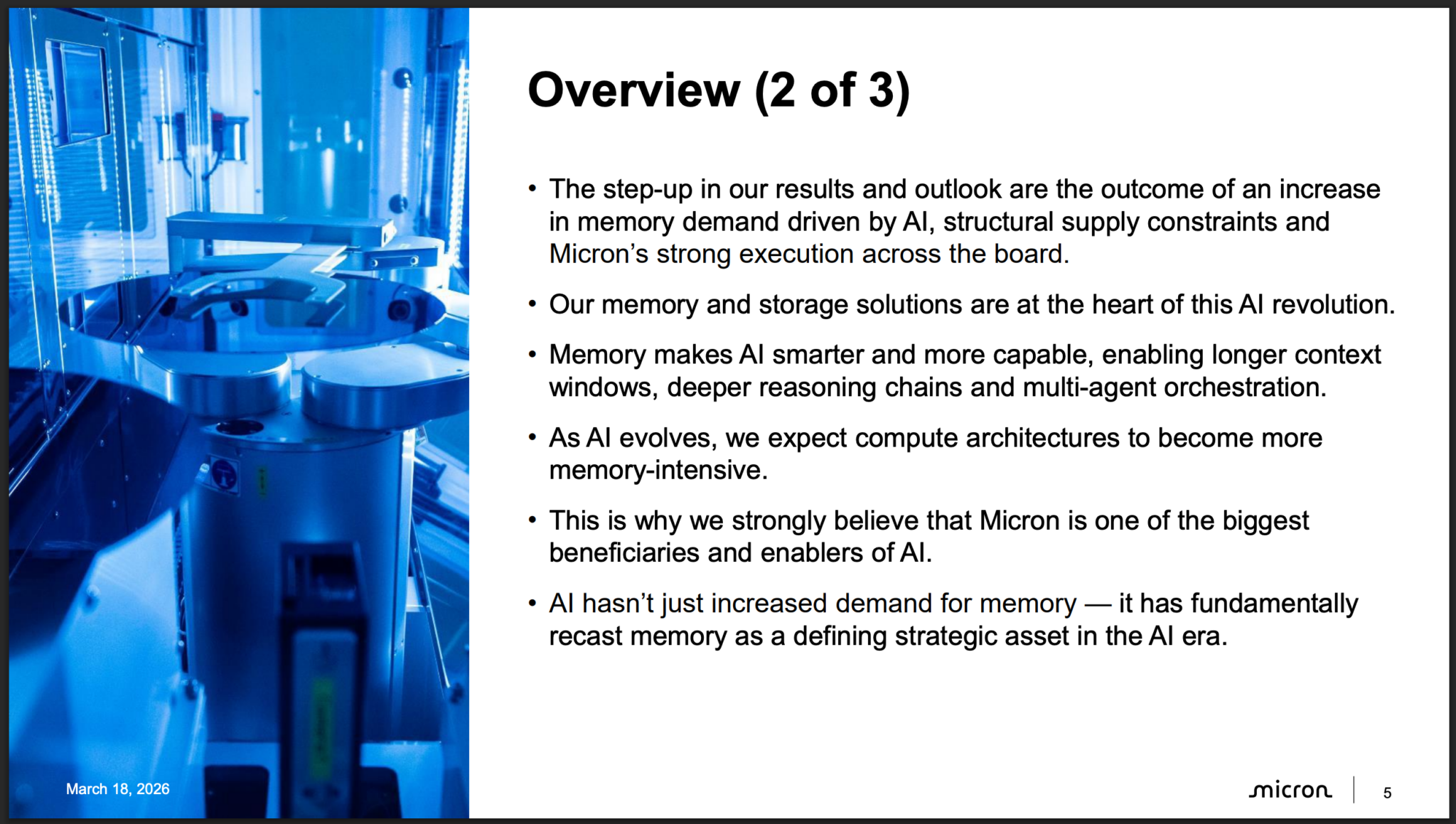

Listen to Sanjay Mehrotra, CEO and co-founder of Micron Technology.

Our memory and storage solutions are at the heart of this AI revolution. Memory makes AI smarter and more capable, enabling longer context windows, deeper reasoning chains, and multi-agent orchestration. As AI evolves, we expect compute architectures to become more memory intensive. This is why we strongly believe that Micron Technology, Inc. is one of the biggest beneficiaries and enablers of AI. AI has not just increased demand for memory; it has fundamentally recast memory as a defining strategic asset in the AI era.

We see an unprecedented set of opportunities in memory and storage to enable the AI era across market segments and expect to meaningfully increase our R&D investments in fiscal 2027.

Rapid growth in AI is driving the emergence of new architectures optimized for the token economics of specific workloads. Micron Technology, Inc.’s broad portfolio of HBM, LP, DDR, and SSD is a critical enabler across these architectures. At GTC, the recent announcement of NVIDIA Grok 3 LPX implements up to 12TB of DDR5 in a rack-scale architecture.

We are seeing an acceleration in NAND-based demand in the data center due to AI use cases such as vector database and KV cache offload, and due to growing share of SSDs in capacity storage tiers. Micron Technology, Inc.’s data center SSD product portfolio, enabled by our technology leadership and vertical integration, covers the spectrum from highest performance to highest capacity. We are now in high-volume production of our G9 NAND-based PCIe Gen6 high-performance data center SSDs. Our 122TB high-capacity SSD is seeing strong adoption, and delivers 16 times the sequential read throughput per watt of a capacity-matched HDD configuration. Our strategy and execution are delivering results.

Believe he is right, and shares in his company are dramatically underpriced.

You could argue that it was the cyclicality of the industries they were serving that caused problems for memory companies in the past, leading to endless boom and bust. This time, they are serving a new industry, which is bigger, growing faster, is more demanding in its technological requirements, less price sensitive, and ultimately driven by the insatiable requirements of AI. Micron and its competitors have been hit by a tsunami of new demand and are battling to react. Using the duck test, this seems to be a highly favourable position for the companies serving this demand. They are growing so fast that their share prices are struggling to keep up.

Maybe some weird market panic will take the shares even lower. As Buffett says, investors sometimes exhibit manic depressive behaviour. If they do fall, or if they don’t, my advice is to buy aggressively. All these shares are heading much higher.

There is a lot of opinion here, opinions are 10 a penny, and what do I know about the memory industry? That’s true, but there is something I do know. Experts are ALWAYS wrong at key turning points because that is when they need to think outside the box. Remember the BBC weather forecaster who famously reassured a worried viewer on live TV that no hurricane would hit the UK in October 1987. What a silly old dear! He wasn’t saying that a few hours later when he saw her and half the trees in Kensington Gardens flying past his window.