Keeping An Eye On Nvidia, Broadcom, Credo Technologies And The Hardware Explosion

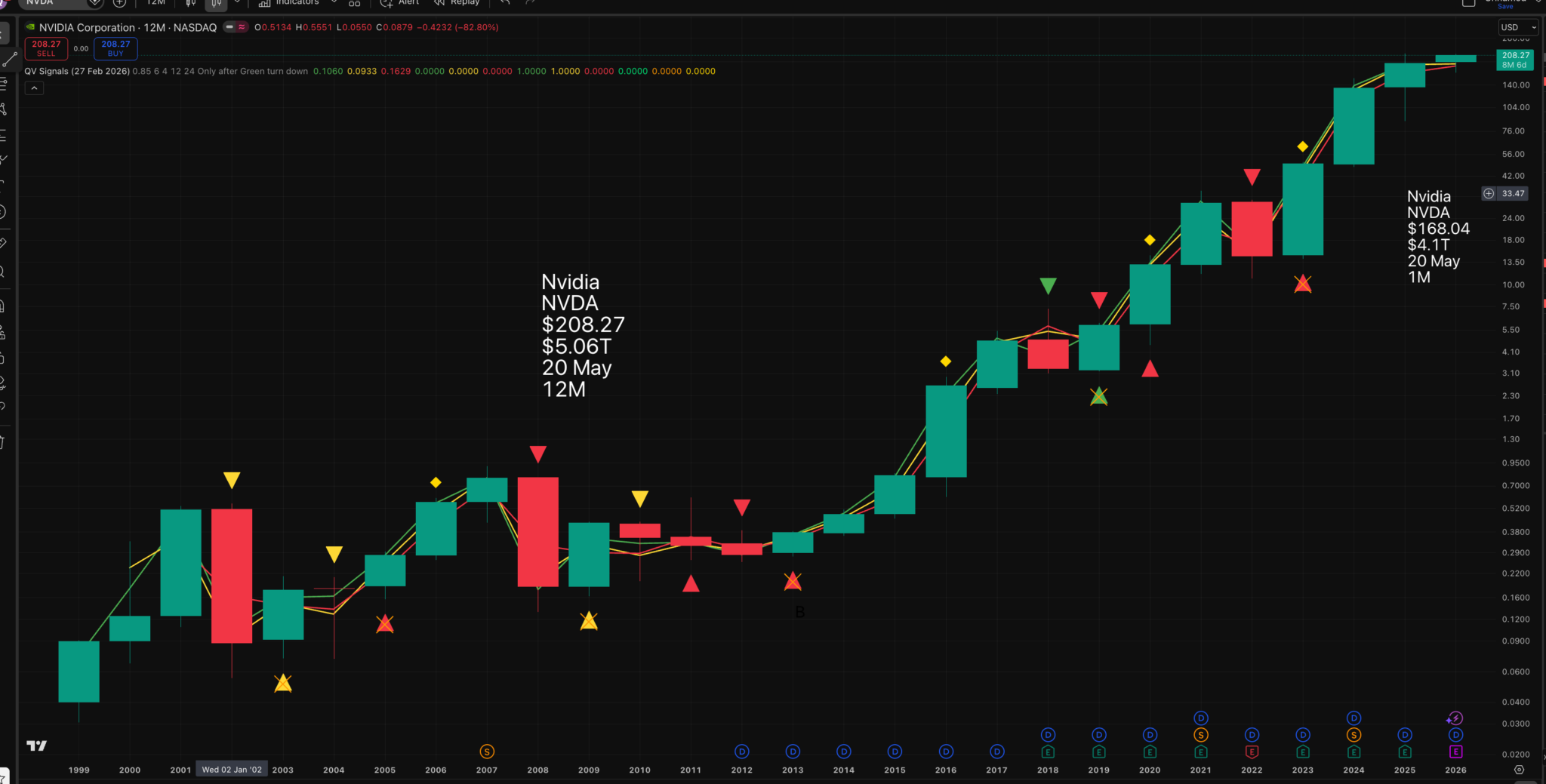

Nvidia is the greatest AI hardware stock in the world. This incredible technology revolution would not be happening without Nvidia. This super long-term chart (each candlestick represents a year) looks good, and the shares have given a yellow-line buy signal on the monthly candlestick chart. They have also staged an exciting chart breakout.

When Nvidia shares first took off in 2016, analysts remained behind the curve for ages because they saw Nvidia as a cyclical semiconductor stock. The reality was that everything changed in 2016: GPUs replaced CPUs as the must-have semiconductors, the AI data centre boom kicked in, and everything went ballistic.

Analysts are still looking for a cyclical peak for many of these hardware stocks. SanDisk has only just begun to boom, and they are looking for the downturn. My simple argument is that the staggering potential of AI means the hardware boom is still early days, with spending set to move from the billions to the trillions, and software is fast becoming a commodity with no pricing power.

On Friday, helped by Quentinvest’s resident tech guru, I began to see what AI can do. It needs to be trained. We used Google’s Gemini, told it that I was a journalist and researcher, and explained to GeminiAI that we wanted it to do deep research and use tools to come up with a report on SanDisk.

The results were staggering. This is what came back from Gemini.

The Pure-Play NAND Renaissance: A Strategic Analysis of SanDisk Corporation in the Global AI Infrastructure Supercycle.

This was followed by 13 pages of detailed analysis and a long list of sources. I have not quoted the whole thing here, but after reading it, I could not have been hotter for SanDisk shares. No wonder they have blasted from nowhere into the Nasdaq 100 index, kicking out software business, Atlassian, in the process.

Below are some snippets from the report.

The rationale for the split (separation of Western Digital and SanDisk, effective 25 February 2025) was centered on “velocity”—a term used by management to describe the need for each business to move at the speed of its respective market.3 While the HDD business was transitioning into a high-capacity, enterprise-focused model catering to massive cloud providers, the flash business was entering a period of explosive demand driven by AI inference workloads and data lakes.2 By breaking the companies apart, SanDisk was able to return to its roots as a pure-play NAND powerhouse, allowing Wall Street to better assess its performance without the earnings drag of the HDD business, which had previously struggled with the cyclical volatility of the NAND market.

The timing of SanDisk’s independence coincided with a paradigm shift in the global memory market. Artificial intelligence has transitioned from a theoretical workload to a physical infrastructure requirement, necessitating a fundamental re-architecture of storage systems.4 Traditional storage models, which relied heavily on HDDs for massive datasets, are increasingly giving way to all-flash arrays in the data center to support the low-latency requirements of AI model training and real-time inference.4

In the 2026 landscape, the data center has emerged as the single largest market for NAND by exabyte consumption, eclipsing the mobile segment for the first time.4 This transition is driven by the massive storage requirements of Large Language Models (LLMs) and the proliferation of “data lakes” where AI models ingest petabytes of unstructured data.4 Management characterizes this as a “step change” in demand, where the incremental exabyte growth for AI-driven workloads is tracking in the high 60% range for calendar year 2026.4This demand is not merely a cyclical spike but appears to be a structural evolution. Nvidia’s Jensen Huang has highlighted the concept of “terabytes of NAND per GPU” for KV cache use cases, where the intermediate states of AI computations must be stored and accessed rapidly.4 This single demand signal is estimated to add 75 to 100 exabytes of incremental demand in 2027, potentially doubling the following year.4 As a result, SanDisk is no longer viewed as a commodity memory supplier but as a critical infrastructure partner in the AI “supercycle”.

After dramatic growth to date prospects look even more exciting.

The path forward for fiscal 2026 and 2027 is projected to be even more aggressive. Management has guided for fiscal third-quarter revenue between $4.4 billion and $4.8 billion, with non-GAAP gross margins projected to climb as high as 67%.8 This level of profitability is unprecedented in the NAND industry and reflects the “higher and more sustained pricing peak” that some analysts believe could lead to earnings per share (EPS) of $25 or more in the June-ended quarter.13

SanDisk’s business is changing.

SanDisk’s competitive moat is constructed around its Bit Cost Scaling (BiCS) technology, which it co-develops with its long-term joint venture partner, Kioxia.4 The current flagship technology, BiCS8, utilizes a 218-layer architecture that maximizes bit density and performance.4 In the first fiscal quarter of 2026, BiCS8 accounted for 15% of total bits shipped, but management expects it to represent a majority of total production by the end of the fiscal year.4

The most significant product application of BiCS8 is the “Stargate” enterprise SSD.4 Stargate is engineered as a 128-terabyte storage-class SSD using BiCS8 QLC (Quad-Level Cell) NAND.4 This drive is designed to replace traditional HDDs in “AI data lakes” where capacity and power efficiency are paramount.4 As of early 2026, Stargate was undergoing qualification with two major hyperscalers, with a third hyperscaler and a major storage OEM expected to begin revenue shipments within the next several quarters.4 This product represents SanDisk’s move toward higher-value system-level solutions rather than raw NAND wafers.4

There is more such as the potential for the alliance with SK hynix but I think you get the idea. SanDisk has a huge opportunity to deliver sustained, explosive growth. Like me you probably don’t understand all the jargon; it is more the sense of what is happening.

At Quentinvest, we are just beginning to learn how AI can improve our operations. We need to push hard to see just what AI can do. Other people will be doing something similar, but AI can’t do it all alone. I have something AI doesn’t have: 60-plus years of deep involvement in stock markets. AI can do the classical stuff, the number and data crunching, but it still needs me for the zen bit, the bit you can’t put into words.

The stock market is hitting new highs.

I know, mea culpa, it is not that long ago that I was becoming increasingly bearish, but as Keynes said to a House of Commons committee, when he was accused of changing his mind – ‘when the facts change, I change my mind; what do you do?’ I think I have moved with commendable speed (a) to change my mind and (b) to grasp that AI is driving an incredible hardware boom and killing software.

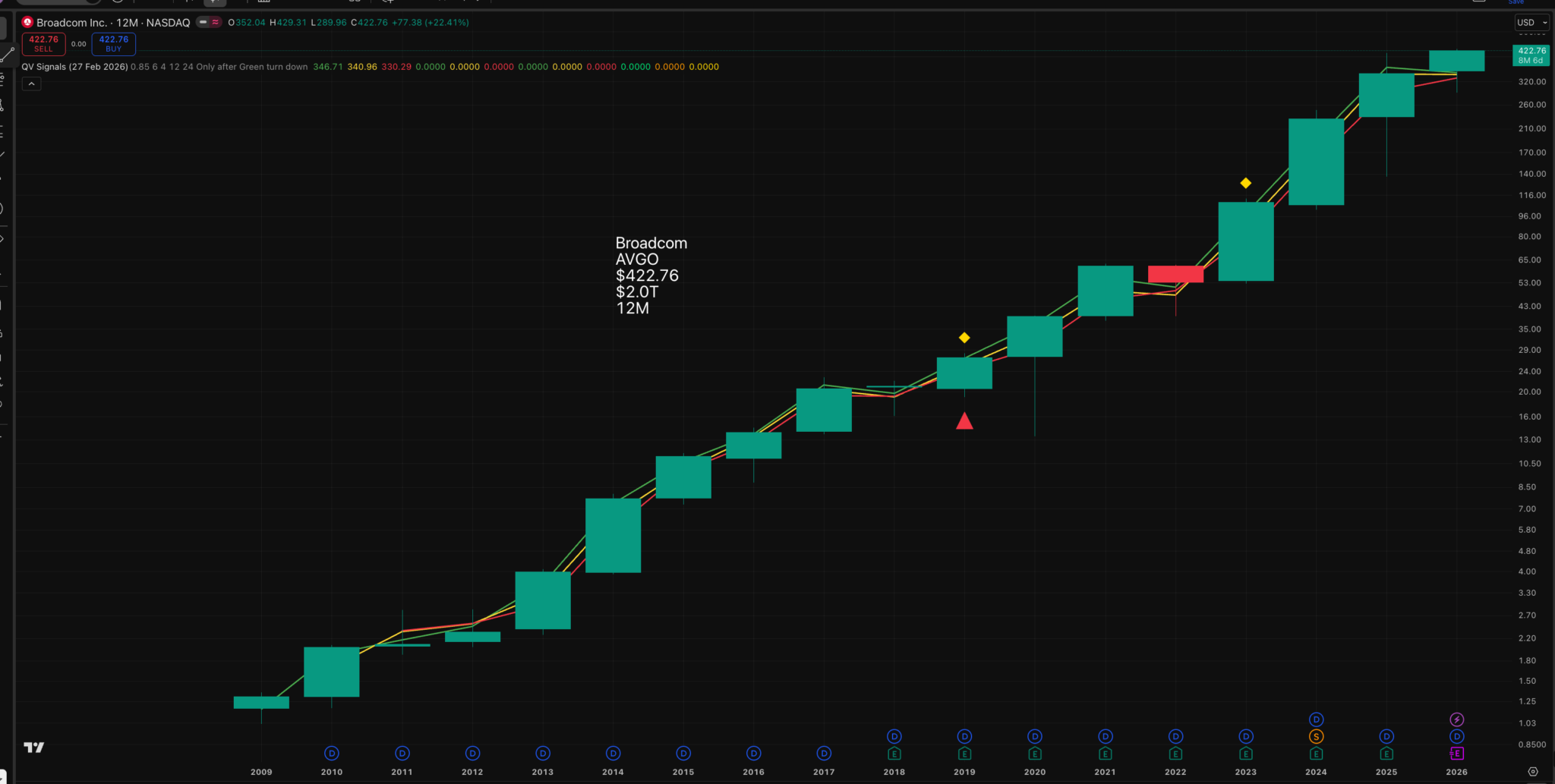

Software has been king for a long time, ever since the old long-time superstar of hardware, IBM, made the wrong choice in the 1980s desktop computer boom and Bill Gates seized the software opportunity to become the world’s richest man. Hardware has been in the shadows ever since, well, not entirely. Intel did well working in tandem with Microsoft in the so-called Wintel boom (Intel’s chips plus Microsoft’s Windows software operating system), but generally, software ruled until things began to change with the success of companies like Nvidia and Broadcom.

What an incredible stock is Broadcom? It is like a perpetual motion machine as strong growth is buttressed by a series of well-judged acquisitions. Below is what CEO Hock Tan said about the latest results.

In our fiscal Q1 2026, total revenue reached $19.3 billion, up 29% year on year, and exceeding our guidance on the back of better than expected growth in AI semiconductors. This top line strength translated into exceptional profitability with Q1 consolidated adjusted EBITDA hitting a record $13.1 billion, which is 68% of revenue. These figures demonstrate that our scale continues to drive significant operating leverage. Now we expect this momentum to accelerate as our custom AI XPUs hit their next phase of deployment among our five customers. Looking ahead to next quarter, Q2 2026, we are guiding for consolidated revenue of approximately $22 billion, which represents 47% year on year growth.

What is happening? Why are these companies doing so well? Because AI, training, inference, self-driving cars, space travel, war, robots, whatever, has an insatiable appetite for more compute. Ever vaster data lakes are being crunched by inconceivably fast and powerful computers, which need memory, energy, networking and who knows what other stuff, which is powering the greatest hardware boom in history, maybe the greatest boom in anything ever. It is like humanity is starting to reach out for the stars, which means there may not be a cyclical peak. In a nutshell, AI has a limitless appetite for more computing power, which makes it hard to see an end to this hardware boom.

Software, by contrast, is in the front line. Almost the whole point of AI is that everything software can do, AI can do as well or better and much more cheaply. This raises a question about Palantir, which is a software business, a very special one, but still maybe vulnerable. The chart is struggling for direction. I am watching it closely. Palantir is also in the sights of the Green Party crazies as the new hard-left leader, Zack Polanski, mops up the old Jeremy Corbyn vote. A debate between Polanski and Alex Karp of Palantir could be fun.

I thought Corbyn had been clever to launch a new party, but Polanski saw him coming and has outmanoeuvred him. Who cares about the planet? Much more fun to rant on about the evils of capitalism and berate the rich or anyone who has more of this world’s goods than the average.

When shares are doing so well, profit-takers move in, but the pattern can change dramatically when a piece of good news comes along.

Credo is prone to dramatic sell-offs, but the fundamentals remain exciting, and investors have reacted with huge enthusiasm to the latest acquisition news.

Credo Technology Group Holding Ltd (Credo) (NASDAQ: CRDO), an innovator in providing secure, high-speed connectivity solutions that deliver improved reliability and energy efficiency for the next generation of AI-driven applications, cloud computing, and hyperscale networks, today announced it has entered into a definitive agreement to acquire DustPhotonics, a leading developer of Silicon Photonics Photonic Integrated Circuit (SiPho PIC) technology for optical transceivers. The acquisition will position Credo with a vertically integrated connectivity stack spanning SerDes, Digital Signal Processing (DSP), Silicon Photonics and system integration for scale out and scale up networks — addressing both electrical and optical interconnects across the full AI infrastructure buildout.

The acquisition of DustPhotonics directly accelerates Credo’s optical interconnect roadmap and significantly expands its served addressable market in the global optical industry. DustPhotonics has developed a differentiated portfolio of SiPho PICs spanning 400G, 800G, and 1.6T, with a roadmap extending to 3.2T, that integrates key optical functions onto a single chip, reducing component complexity, improving manufacturing yields, and enabling meaningfully lower cost at scale as port speeds advance beyond 800G. In combination, these factors improve AI cluster reliability, a critical factor for data center operators. These SiPho PICs are deployed in transceivers at leading hyperscale AI clusters and are also in design for leading Near Port Optics (NPO) and Co-Packaged Optics (CPO) applications. According to LightCounting1 and Credo estimates, the SiPho PIC market is expected to grow to $6 billion by 2030.

Critically, SiPho PIC technology is a foundational component of Credo’s ZeroFlap (ZF) Optical Transceiver platform. Bringing this capability in-house mitigates external supply dependencies, accelerates product development cycles, and creates a pathway to substantial cost structure improvement at volume. Combined with Credo’s industry-leading SerDes and DSP intellectual property and products, the acquisition creates an end-to-end optical connectivity solution platform.

Credo believes it has reached an inflection point in its optical business. With the addition of DustPhotonics, the company expects its combined portfolio of ZeroFlap Optical Transceivers, Optical DSPs, and Silicon Photonics products to generate greater than $500 million in optical revenue in fiscal 2027, reflecting strong customer traction and expanding adoption across hyperscale AI deployments.

Credo CEO, William Brennan, described the acquisition as follows:

“Combining forces with DustPhotonics marks a defining step in Credo’s strategy to lead across the full spectrum of AI connectivity. We’ve built a strong position in high-speed electrical solutions, and this move decisively expands that leadership into Silicon Photonics with best-in-class PIC technology that complements our ZeroFlap Optical Transceivers and DSP portfolio.

This combination positions us at an inflection point in optical. As adoption accelerates across hyperscale AI infrastructure, we expect our optical business to scale into a meaningful and rapidly growing contributor by fiscal 2027.

More importantly, we are building a vertically integrated connectivity platform that spans from copper to optical and from chip to cluster—allowing us to solve for the two constraints that matter most at scale: reliability and power efficiency, while deepening our role as a strategic partner to our customers.”

Share Recommendations

Nvidia. NVDA

Broadcom. AVGO

Credo Technology. CRDO

SanDisk. SNDK

Strategy – Great Opportunities In Hardware Boom

America and the world are going through the greatest infrastructure transformation in history as planet Earth becomes a gigantic networked supercomputer, crunching its way through vast data lakes to give us insights on a scale light-years greater than anything humanity has enjoyed previously. We are in a period of seismic change. Who would have thought, some 2m years ago, when the first species in the homo genus evolved on Earth, that this was coming? Homo Sapiens Sapiens may not be the nicest of guys, but the drive and energy of the species is incredible. If there are aliens out there, they may have a surprise coming!

I am not recommending them here, but both Intel and Nokia shares have exploded recently, perhaps partly as they enter partnerships and even investments from Nvidia. The Nokia chart breakout is a classic.