Peloton Interactive has brought to the world a new concept – connected fitness. It is the healthy counterpart to the lockdown inspired trend of working from home only with Peloton you exercise at home. Thanks to lockdown business is booming. Demand is so strong the company is struggling to keep up and is building new capacity to supplement the contract manufacturers who have been the main suppliers to date. However it is not all about lockdown. Peloton is a true disrupter and the business was growing explosively before anyone ever heard of Covid-19. CEO and co-founder, John Foley, says the global opportunity for connected fitness is vast.

Gyms are social places. I love going to my gym (albeit, I am not going at the moment) but like working from home we are going to mix and match in future. I can easily imagine still going to the gym but also having a Peloton bike. Sometimes it is just so much more convenient to exercise at home. Wherever you exercise you get that endorphin-fuelled adrenaline rush, which makes you feel great and with interactivity and charismatic instructors Peloton makes exercise great fun; that is why their churn rate (the number of subscribers they lose) is tiny, typically around 0.6pc. This really is a great business with a very exciting future.

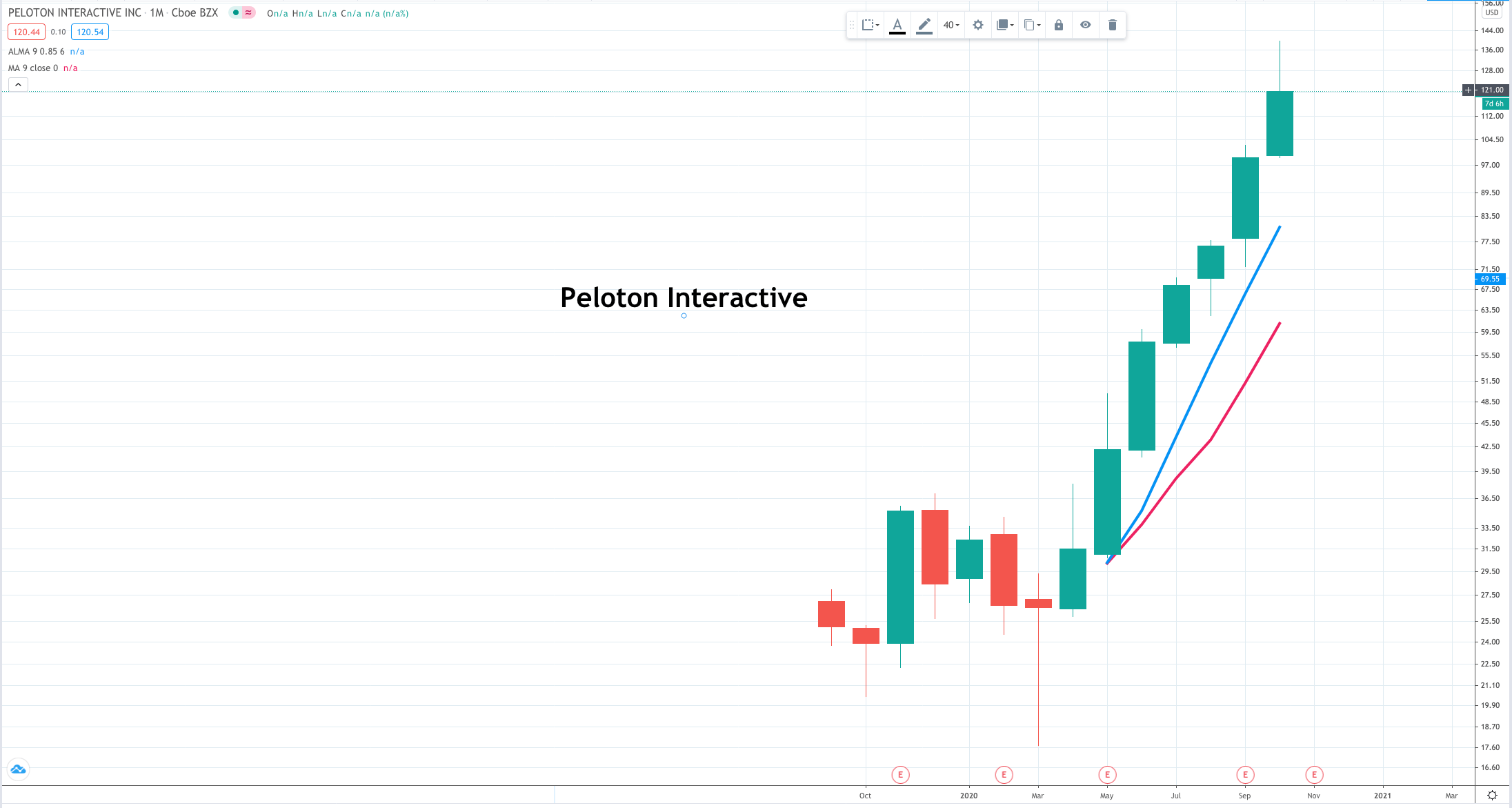

Peloton Interactive PTON Buy @ $120 MV: $35bn Employees: 3,800 Number of times recommended: 5 First recommended at $45.11

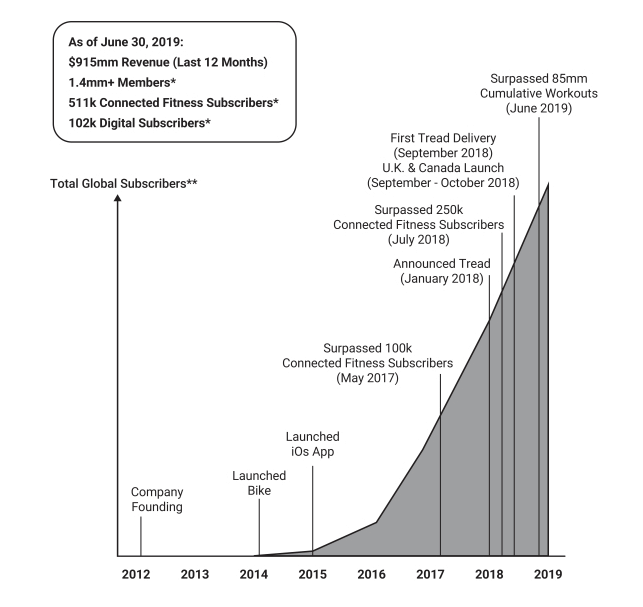

I took the chart above from the 2019 annual accounts. It shows what was happening to the business before anyone had ever heard of Covid-19. Since March 2020 an already fast-growing business has experienced an even more dramatic surge. The statistics are staggering. In the year to 30 June 2017 there were 6.2m workouts using Peloton equipment. By June 2019 that had grown to 58m. The figure for the year to 30 June 2020 was 165m with 333pc growth in the fourth quarter.

There are two things extraordinary about that figure. One is how fast it is growing; two is how small it is in relation to what it could be. If you think of Peloton as the Facebook of the exercise world, 165m workouts in a year is nothing. There are 3.5bn owners of smart phones in the world. Peloton is still barely scratching the surface of the opportunity. It is also still overwhelmingly about cardio exercise, bikes and treadmiils and mostly the former. There is a whole world of other types of exercise out there from yoga to building strength, which the company has barely touched so far but which it is very much targeting. As CEO JOhn Foley noted in the Q4 report.

“Clearly, if you’re going to move all of your fitness programmings into the home Strength is another complement to your Cardio that we need to win. I will remind you that with our new studios in New York and London, we have dedicated Strength studios within those broader studios. We’re going to have more and more programming for Strength training, not just the Bike Bootcamp but with the lower price Tread. The treadmill workouts and Tread Bootcamp. I think these are the best workouts because they’re both cardio and strength. And so we think that our approach will be a winning approach with respect to other products in the marketplace. We haven’t seen anything that I’m not excited about. I like to work out with free weights, and bands, and body weight. And we’re going to offer that in such volume that we think we’re going to be able to win with our current approach.”

There were five founders of the business but the key figure is CEO, John Foley, who is now in his late 40s. He was the guy with a young family who became frustrated with the difficulty of getting to the gym and booking the classes he wanted with his favourite instructors. He decided that with the help of technology there must be a better way and the obvious solution was to have a really great exercise experience at home.

At first nobody agreed and he struggled to raise any money for his new venture. In sunny open air California he was told there are two kinds of bikes, on-road and off-road. Nobody was interested in stationary bikes at home even though Foley insisted that there was a very different perspective in places like New York. He needed money because he was determined to do things properly. He wanted to use technology to blend exercise, media, music and great equipment to give his customers a really special experience.

His timing was perfect. Just as Bezos put half the world’s booksellers out of business by selling an unlimited selection of books online at great prices so Foley is challenging the world’s gyms by offering a better exercise experience more cheaply and with far greater convenience online. He is able to offer this connected fitness experience because we live in a connected world. In the US 95pc of the population are permanently connected to the world wide web through their phones, which are increasingly linked to their other devices. No wonder Foley talks of all the Peloton members and subscribers as being part of a community. They are because they are all linked into the same Internet.

The measure of his success in doing that is the incredibly low churn rate, which hovers around half a per cent. Peloton is successful because the customers love the experience. They exercise on state-of-the-art bikes to pounding music (from four speakers on the recently launched Peloton+ bikes) with touch screens, where they can connect with great instructors and absorb a ton of data about their performance. When they finish they feel great, buzzing with endorphins and ready to take on the world. Exercise is a kind of drug, a good one, which is why Peloton describes classes with their instructors as almost addictive experiences.

It is this achievement, Peloton’s ability to really deliver for its subscribers, which underlines the potential of the business. Based on one great product, the Peloton bike, launched in 2014 (see chart above) they have started to add other products like a Digital App for workouts (for which you don’t need Peloton equipment) and in 2018 the Peloton Treadmill. Since then they have launched a new, more fully featured bike while reducing the price of the original bike. They have also launched a more compact, cheaper Treadmill because the original treadmill, now called Treadmill+, is an expensive piece of kit costing over $4,000.

The way the business works is that the hardware, bikes and treadmills, are bought separately from the subscription, which gives you access to the instructors and the connected fitness programmes, of which there are loads with more being created all the time. The bikes cost around £2,000 in the UK but are made more affordable because you can pay over 39 months interest-free. This makes the cost £49 a month for which you get the high quality, high spec bike delivered to your home. Many people then pay an additional £39 a month for the full connected service.

Membership costs at my gym range between £169 and £240 a month and many of the members don’t use the club all that much, whereas they almost certainly would use their Peloton at home. It is much easier and especially for lone exercisers in gyms much more fun. Personally, I only go to classes at my gym but many people exercise alone and if they use a personal trainer the cost goes through the roof.

The new Peloton mini-Tread is due to be launched at the end of December 2020 and costs around the same as the original Peloton bike before the price cut or the new Peloton bike+ now. The company expects it to be a game changer not least because the treadmill market is three or four times the bike market. Go into any gym and there will be far more people on treadmills than bikes unless there is a spinning class in progress. The problem is that because of the huge demand triggered by widespread lockdowns the company is battling to produce enough bikes, let alone the new treadmills. Because of this they say that they don’t expect revenues from the new treadmill to really kick in before the financial year ending 30 June 2022. However when they do arrive they could ramp up very quickly if early experiences with the Peloton bike are a good indicator.

Below is a summary of what Peloton does in the company’s own words.

“We are an innovation company at the nexus of fitness, technology, and media. We have disrupted the fitness industry by developing a first-of-its-kind subscription platform that seamlessly combines the best equipment, proprietary networked software, and world-class streaming digital fitness and wellness content, creating a product that our Members love. We have a direct-to-consumer multi-channel sales platform, including 74 showrooms with knowledgeable sales specialists, a high-touch delivery service, and helpful Member support teams. Our Members are as devoted to us as we are to them—92pc of our interactive fitness equipment ever sold, which we refer to as our Connected Fitness Products, still had an active Connected Fitness Subscription attached as of June 30, 2019.

Our Connected Fitness Product offerings currently include the Peloton Bike, launched in 2014, and the Peloton Tread, launched in 2018. [Since then they have cut the price of the original bike, launched the Bike+ with more features and the dramatically more affordable, mini Tread]. Both our Bike and Tread include a state-of-the-art touchscreen that streams live and on-demand classes. Our products have a multitude of interactive software features that encourage frequent use, facilitate healthy competition on our patented leader board, build community among our Members, and inspire our Members to track performance and achieve their goals with real-time and historical metrics. As of 30 June, 2019, we had sold approximately 577,000 Connected Fitness Products, with approximately 564,000 sold in the United States. Our world-class instructors teach classes across a variety of fitness and wellness disciplines, including indoor cycling, indoor/outdoor running and walking, bootcamp, yoga, strength training, stretching, and meditation. We produce over 950 original programs per month and maintain a vast and constantly updated library of thousands of original fitness and wellness programs. We make it easy for Members to find a class that fits their interests based on class type, instructor, music genre, length, available equipment, area of physical focus, and level of difficulty.”

The company is very aware of the global opportunity and also the need to gain first mover advantage in as many countries as possible so it is very much on the front foot driving international expansion. The company has already expanded into Canada, the UK and Germany, albeit it is still early days. As they say in the Q4 2020 report: “We have global ambitions and we are excited to get into more countries in more languages as soon as we can.”

It also spends heavily on research and development to launch more products and improve the existing ones. Last but not least is the massive spend on sales and marketing as the company races to win the all-important battle for territory. The company markets partly through all the usual media and also through its showrooms, which have grown in number from 74 in 2019 to 103 currently. So far there are three in London in Marylebone, Spitalifields and Canary Wharf respectively.

The last element in the marketing mix is a digital App, Peloton Digital, which offers loads of classes in all sorts of disciplines from bootcamp classes to yoga and dance but without the hardware so no bike or tread. This is much cheaper at $19.99 a month or even less. It has been growing dramatically from 102,000 subscribers in June 2019 to 500,000 currently helped by a free trial offer during Covid. Growth is expected to slow from this incredible rate but the App is more a marketing tool than a potential profit centre. Many people start with the app but move on to become a Connected Fitness subscriber.

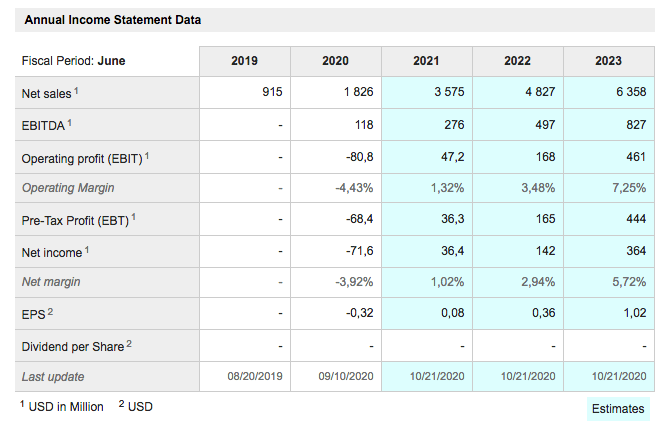

The spend on both r&d and marketing is exploding. R&d has gone from $13m in 2017 to $89m in 2020 (to 30 June year end). Sales and marketing has gone from $86m to a staggering $477m. This explains why even after making a gross profit of $837m in 2020 the group still managed to lose $71.6m (see table below).

This might seem disconcerting to some people but makes good sense. There is a powerful network effect with Peloton in that the more the group scales the more valuable the group is to its community of members and subscribers and the more it can use massive economies of scale to reduce the hardware costs so encouraging yet more people to subscribe.

“So the original Bike and the Bike+ carry similar gross margins but as we continue to build 1m, 2m, 3m we are going to realise even more product efficiencies and we love the idea that we are able to give a lot of those efficiencies back to the customer to continue to plow that into growing the top line.”

It is also spending on state of the art studios, which are helping instructors to deliver a cinema quality experience even before the global roll out of 5G networks which will help to make the experience even better.

The gross profit figure of $837m is important because it shows how Peloton will eventually become very profitable. Most likely it will keep growing r&d and marketing costs for the foreseeable future as it chases its “vast” opportunity but even so they will over time shrink as a proportion of sales and once the group starts to become profitable, which could happen as early as next year according to the table below, profits should ramp very rapidly.

The group also sees another opportunity with corporates and insurers, who both have an interest in keeping employees healthy. Quite what form this relationship might take is hard to say but Foley noted in answer to a question

“You’re absolutely right about the opportunity we see with corporates and insurers. We think this is a massive opportunity and potentially a very big growth vector for us in coming years.”

It is obviously not true to say that investors don’t understand the potential of Peloton Interactive. A valuation of nearly $35bn for a business making losses and with 2020 sales of $1.8bn is not ungenerous. Nevertheless I think Peloton really is still in the early innings of a massive opportunity.

On way of looking at that opportunity is summed up in a quote from the 2019 prospectus.

“We consider our market opportunity in terms of a Total Addressable Market, or TAM, which we believe is the market we can reach over the long-term in our current and announced markets, and a Serviceable Addressable Market, or SAM, which we address with our current product verticals and price points.

According to our research, our TAM is 67m households, of which 45m are in the United States. Within our TAM, we estimate that 52m households are interested in learning more about our Connected Fitness Products without seeing the price. We estimate that our SAM is 14m Connected Fitness Products, with 12m represented in the United States. Historically, our SAM has grown as our brand awareness has increased. With low brand awareness in our current international markets, we believe we will see SAM expand as we make further investments in building brand and product awareness in these regions. We will grow both TAM and SAM as we expand beyond our current geographies and grow SAM as we develop new Connected Fitness Products and content in new fitness verticals. With approximately 577,000 Connected Fitness Products sold globally as of June 30, 2019, we are approximately 4pc penetrated in our SAM of 14m.”

You could say that by already reaching significant scale the group has already reached critical mass and cemented first mover advantage. it is hard it is hard to imagine it will be winner takes all for Peloton but to be the market leader in a huge market is a stunning opportunity.

“As the largest interactive fitness platform in the world, our rapidly growing and scaled Member base is a highly strategic asset. With our first mover advantage, we have achieved critical mass, which improves our platform and Member experience. As of June 30, 2019, on average, nearly 6,400 Members participated in each cycling class, across live and on-demand. As our community of Members continues to grow, the Peloton fitness experience becomes more inspiring, more competitive, more immersive, and more connected. Over time, Members are embedded in the Peloton community and we become a part of their lives, increasing the opportunity cost of Members leaving or potential Members not joining our platform.”

Also striking is the level of engagement.

“By making fitness fun and motivating, we help our Members achieve their personal goals. We analyze millions of workouts per month to help us develop features that improve our Member experience and create new, on-trend fitness and wellness content that our Members crave. Engagement is the leading indicator of retention for our Connected Fitness Subscribers. We have consistently seen workouts increase over time. On average, our Connected Fitness Subscribers completed 7.5, 8.4, and 11.5 workouts per month in fiscal 2017, 2018, and 2019, respectively. Usage drives value and loyalty, which is evidenced by our exceptional weighted-average 12-month Connected Fitness Subscriber retention rate of 95pc across all fiscal year cohorts since fiscal 2016.”

The latest figure for workouts per month per subscribers is an incredible 25. Even if that owes something to lockdown it is a staggering figure and highlights how much the subscribers love the Peloton experience and that experience is only going to become even better over time.

Another testimonial is provided by the Net Promoter Score (NPS). Remember than anything positive is good, over 50 is very good. Peloton has an NPS which has ranged between 80 and 93 since they began measuring it in 2016.

This is what John Foley says about Peloton.

“Seven years later (from 2012 when the business was born), it is very clear to me that we have an immense opportunity in front of us at Peloton. Peloton is so much more than a Bike — we believe we have the opportunity to create one of the most innovative global technology platforms of our time. It is an opportunity to create one of the most important and influential interactive media companies in the world; a media company that changes lives, inspires greatness, and unites people. And it is an opportunity to create one of the best places to work in the cities where we operate — we prioritize culture as much as any other business objective.”

I have decided to stop taking about superstocks and call them ‘great businesses of the 21st century’ instead. I like that name because it so clearly implies that these stocks are for buying and holding. If you own a piece of one of the great 21st century businesses, why would you ever want to sell it.

You may be thinking – how on earth can an exercise bike business be worth $35bn. People thought something similar about Netflix. How can a video streaming business be valued in the billions. Surely anyone can stream videos. The trick lies in the execution. I can go down to the pub and come up with loads of great business ideas. Ideas are 10 a penny. What is much more rare is individuals who can take an idea and run with it. John Foley is clearly one of those individuals. Another is Reed Hastings of Netflix which is why that business is valued at $212bn even after disappointing investors with its latest results.

I see many parallels between Peloton and Netflix. Both companies have first mover advantage in huge markets, health and fitness and entertainment respectively. It is no surprise that they have the opportunity to build correspondingly large businesses.