Hong Kong is going after the Chinese technology shares that typically list on Nasdaq, hoping to encourage them to list in Hong Kong. As part of this process it has developed an index (see above) measuring the performance, so far pretty good, of the 30 largest technology companies listed in Hong Kong, including names like Alibaba and Tencent. As it happens the four Chinese technology shares above are listed on Nasdaq and are not in this index. Most likely they will all do well, those listed on Nasdaq and those listed in Hong Kong.

BeiGene BGNE Buy @ $345 MV: $30.6bn Employees: 4,600 Next figures: 3 March Times recommended: 5 First recommended: $181 Last recommended: $307

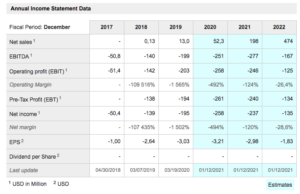

BeiGene is one of two biopharma stocks in this quartet. China is very keen to develop home grown pharmaceutical companies and has been moving rapidly into the 21st century in regulatory terms. Chinese biopharmas, like all biopharmas, want to research and develop their own drugs but that is a slow, risky and very expensive process. As they move towards this goal they have a more immediate opportunity to act as a gateway and even co-developer of western developed drugs going into the vast Chinese market, which means investing in local capabilities like manufacturing, distribution and the ability to conduct clinical trials. There is a good chance that some serious Chinese biopharmas are going to emerge in the current decade. Hence my enthusiasm for likely candidates in Quentinvest. Both BioGene and Zai Lab (see below) have made it clear that building leading global biopharma businesses is exactly what they are trying to do and that means businesses valued in the $100s of billions. However, as has been seen with BioGene, it can be quite a bumpy road so investors need to be prepared for share price volatility but that is the norm with most high growth, high ambition businesses.

Income and cash flow definitely helps but early stage biopharmas are typically valued on news flow as much as actual results so you need to invest in companies with dynamic managements and lots of exciting things going on. Since Christmas, Beigene has issued five press releases. On 27 December it announced the inclusion of three innovative oncology drugs in the China National Reimbursement Drug List. On 7 January it said it would present at the 39th JP Morgan annual healthcare conference (Zai Lab is going to be there too). On 11 January it announced an agreement with Strand Therapeutics to develop solid tumor immuno-oncology therapeutic products based on Strand’s next generation multi-functional mRNA technology. Also on 11 January the company said it was collaborating with Novartis to develop and commercialise Anti-PD-1 antibody, Tislelizumab. On 13 January the group announced that the China National Medical Products Administration had approved Tizlelizumab in combination with chemotherapy in first line advanced squamous non-small cell lung cancer.

I don’t try to do an in-depth analysis of companies like Beigene. There is no point. I don’t remotely have the expertise to assess whether any particular new drug is going to succeed or not. It is all about getting the feeling that this is a business with the ability and dynamism to succeed. BeiGene was founded by an American, John Oyler, who is the CEO but most of the top team and staff are Chinese. The group has made great progress since it was founded in 2010 and is committed to developing new oncology treatments and helping patients in China. It looks very exciting and, thanks to its growing list of important partnerships, sales are on a strong growth path.

BiliBili BILI Buy @ $122 MV: $32.1bn Employees: 4,791 Next figures: 3 March Times recommended: 3 First recommended: $62.5 Last recommended: $101

Here is one description of BiliBili that I like. “Up-and-coming Chinese entertainment platform Bilibili has a catchy name and an even catchier business model. The company has a diversified revenue stream, riding the growing demand for online games, live streaming, e-commerce, and other paid subscription services. By combining the playbooks of modern entertainment giants like YouTube, NetEase, Twitch, and Netflix, Bilibili is seemingly one of a kind.

Despite being just 24pc of the population Gen X consumers make up 62pc of the Chinese online entertainment market valued at $102bn in 2020. This is key for BiliBili because 80pc of their audience are Gen Z. They are also moving into content ownership. BiliBili recently acquired a 9.9pc stake in Hong Kong-listed Huanxi Media marking its formal entry into the business of video production and intellectual property ownership. As part of a five-year deal with Huanxi — a studio with a track record of box office hits including 2020’s highest-grossing film globally, The Eight Hundred — Bilibili now has exclusive rights to broadcast existing and upcoming films and series from Huanxi, outside of the latter’s video-on-demand platform. Bilibili has also obtained the right of first refusal to all forthcoming films and series from the studio. It has also entered into a strategic partnership with Riot Games for a three-year exclusive license to live-broadcast League of Legends esports global events in Mandarin.

Last but not least, the company has powerful backers. Alibaba , Tencent and Sony own 13.3pc, 7.2pc and 5.0pc respectively, which helps with access to high quality content and with developing a live streaming ecommerce business. Revenue grew in excess of 70pc in the first nine months of the year. Gross profit surged 117pc thanks to revenue growth and improved operating leverage. Average monthly active users (MAUs) increased on a year-over-year basis by 54pc to 197m and average daily active users (DAUs) grew 42pc to 53 m — both new quarterly records. MAUs exceeded 200m in August, a new monthly record. User engagement has been strong, with users spending an average of 81 minutes per day in its ecosystem. Collectively, users viewed an average of 1.3bn videos per day, up 77pc year over year.

The company is also getting better at turning free users into paying customers. Bilibili has multiple avenues to make money from its users, including mobile games, live-streaming, membership subscriptions, advertising, and e-commerce. In the latest quarter, 15m users spent money on the platform, up 89pc year over year. Out of these, 12.8m are premium subscribers, an improvement of 110pc compared to last year. Nor is this just a Covid phenomenon. Subscribers have more than quadrupled from 2.7 m in September 2018. BiliBili calls paying customers MPUs and in the third quarter their number reached 15m. The ratio of paying users to total users, a key metric of business performance, improved from 6.2pc a year earlier to 7.6pc.

One major strength that Bilibili has demonstrated is its ability to diversify not only its content offerings, but also its income streams. It has grown far beyond animation, comics, and games content to incorporate other themes such as lifestyle, drama, variety shows and technology and also expanded into new formats like live-broadcasting and movies. Moreover, Bilibili could continue to introduce new services to delight its users, which would further help improve user engagement. The idea here is that as users become more engaged and familiar with Bilibili’s platform, they end up consuming more content and spend more money.

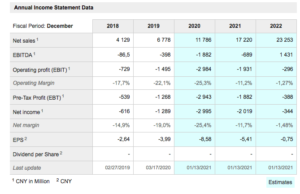

Bilibili’s management are excited about prospects as well they might be for a business that is projected to grow revenues from CNY4.1bn to over CNY23bn between 2018 and 2022 (US$1 – CNY6.45 so CNY23bn is fast approaching US$4bn). “We see a golden opportunity to expand our reach in today’s market. To seize this window, we stepped up our approach to user growth, with a focus on further growing our content, expanding our brand awareness and targeted channel acquisition.“

They are also making a determined effort to spread beyond the Gen-Z demographic. While Bilibili have become a household name among young generations, there are large groups of potential users who are just beginning to learn about them. “The Gen Z community acts as our anchor as we begin to cast an even wider net. Today we are gaining traction with more diverse demographics than ever before. Marketing campaigns such as our newly introduced slogan Bilibili-All the Videos You Like has helped us to define and promote our appeal to mass audiences. During the third quarter, we launched a series of online and offline campaigns to promote our brand proposition to an even broader audience across different demographics. This strategy is working, and we’re carrying these efforts into the fourth quarter.”

The opportunity looks enormous. “China represents the largest online video population in the world. According to the CNNIC report, by the end of the first half of 2020, near 890m users in China consumed online content in video format. Faster networks and smarter hardware enable more accessible content creation and consumption. Our experience over the past decade has made us the pioneer of the video-lization movement. We are committed to capturing this market opportunity by further executing our growth strategy, which we believe will yield considerable return in the long run.“

There is loads more going on at Bilibili, which is a super innovative company and looks to me like a very exciting investment.

Futu Holdings FUTU Buy @ US$69.38 MV: US$4.67bn Employees: 847 Next figures: 24 March Times recommended: 4 First recommended: $29.4 Last recommended: $57

Futu Holdings is a broker based in Hong Kong. This is how they describe what they do. “Futu Holdings Limited is an advanced technology company transforming the investing experience by offering a fully digitized brokerage and wealth management platform. The company is pursuing a massive opportunity to facilitate a once-in-a-generation shift in the wealth management industry and build a digital gateway into broader financial services by primarily serving the emerging affluent Chinese population.” It sounds like an exciting opportunity, especially given Hong Kong’s efforts (see above) to turn itself into Nasdaq for Chinese companies.

So far the strategy is working. “Our net paying client addition [for Q3 2020] was approximately 115,000, bringing the total number of paying clients to over 418,000, up 137pc year-on-year. This marks our highest quarterly paying client addition. Our China mainland and Hong Kong paying clients both experienced triple-digit growth in the quarter, driven by a number of industry tailwinds including continued market volatility and the surge of high-profile Hong Kong IPOs. Organic growth continued to contribute over half of our new paying clients. During our second quarter earnings call, we guided for 280,000 net new paying clients in 2020. We are well on track to deliver this guidance.”

Client assets are also growing at a steep rate. “Besides total paying clients, we also witnessed robust growth in total client assets. As of quarter-end total client assets reached HKD201bn (US$25.9bn), representing 178pc growth on a year-on-year basis and 41pc growth on a quarter-on-quarter basis. Average asset balance for paying clients was HKD481,000, up 17pc year-on-year. Our quarterly paying client retention rates surpassed 98pc for the seventh consecutive quarter.”

The company is also eyeing other areas of growth. “We have been reaching new milestones with internationalization. Futu Singapore Private Limited was officially granted the capital market services license from the Monetary Authority of Singapore. We aim to launch the Singapore business in the first half of 2021 and we are excited about our growth prospects in the country. Besides, I’m pleased to share that on 13 November 2020, Futu Futures Inc. application for National Futures Association member was approved. Futu Futures Inc. is now a commodity futures trading commission registered merchant.”

In the past stockbroking/ asset management businesses like Futu have been cyclical, booming in good times and then being stuck with high costs from previous over-expansion in bad times. However, I think what we are seeing in Hong Kong is more of a secular phenomenon. China needs a credible stock market, which is not Shanghai, which is more of a casino than a proper stock market. Hong Kong has a long history of being a credible financial centre so investors from all over the world are ready to buy shares in companies quoted in Hong Kong. It could emerge very rapidly as the Chinese financial and stockbroking capital. Sadly this is more likely to happen if China feels in control as has been happening in recent months with the mainland authorities moving to tighten their grip.

Founder and CEO, 42 year old, Leaf Hua Li, who was Tencent’s 18th employee and founded Tencent Video, says there are five parts to Futu’s growth strategy. “Number one is our retail brokerage business; number two, our financial management business that provides a lot more earnings visibility by its nature; third is our enterprise service Futu I&E [the brand name for the new business combining ESOP and IPO] with ESOP [employee stock ownership systems] and IPO [Initial Public Offerings] distribution services. Number four, is our international expansion. We want to expand our client site and we think that overseas market will contribute to a meaningful share of our overall paying client base in the mid to long run. Number five, is that we want to develop Futu into an ecosystem that is centred around users and provides connectivity to different stakeholders like the investors, TLLs (I don’t know what these are), media etc. and we want to construct a self-reinforcing ecosystem. Our strategy is to become a one stop financial services platform for our clients.”

Futu is operating in a highly competitive market place. Critical to its efforts to succeed are the emphasis on technology (74pc of the workforce are in r&d). CEO, Leaf Hua Lion, also describes himself as chairman of the technology committee and says of the company. “Futu Holdings Limited is an advanced technology company transforming the investing experience by offering a fully digitizsed brokerage and wealth management platform. Technology permeates every part of the business, allowing the company to offer a redefined user experience built upon an agile, stable, scalable and secure platform. Futu primarily serves the emerging affluent Chinese population, pursuing a massive opportunity to facilitate a once-in-a-generation shift in the wealth management industry and build a digital gateway into broader financial services.”

Futu strikes me as another phenomenally exciting investment with a real ground floor opportunity in Hong Kong and China. On 8 December the group announced that “a leading global investment firm has agreed to purchase approximately 50,000,000 Class A ordinary shares of the Company in the form of prepaid warrants for an aggregate purchase price of approximately US$260,000,000.” Different from most UK stockbrokers the average age of its clients is low at just 36. They are typically high earners working in areas like finance and technology.

Xai Lab Limited ZAI Buy @ $170 MV: $15bn Employees: 910 Next figures: 5 May Times recommended: 1 First recommended: $145

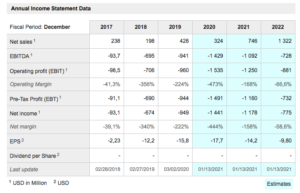

If you thought (see above) that BeiGene was moving fast, Zai Lab may be moving even faster. The company was only founded in 2014 yet it already is heading for revenue of $474m by 2022, according to analysts and has put together a formidable pipeline of drugs under development and partnerships with western biopharma businesses. One measure of the pace at which the group is moving is that employee numbers have risen roughly sixfold since the 2017 flotation. The group says it is on track to be a leading global biopharma company in three years time and who is to say they won’t achieve their goal and won’t use that as a springboard to even greater achievements over the medium to longer term.

Zai was founded by Dr Samantha Du, who previously played a key role in the formation of Hutchison China Meditech. another ambitious biophama backed by the powerful, CK Hutchison, a company with links to the original Hongs, who made Hong Kong the thriving entrepot it went on to become. In market value terms Zai has already left Hutchison Meditech far behind.

The company describes its strategy as follows. “Zai Lab is an innovative, research-based, commercial stage biopharmaceutical company based in China and the U.S. focused on bringing transformative medicines for cancer, autoimmune and infectious diseases to patients in China and around the world. Headquartered in Shanghai since our founding in 2014, our experienced team has secured partnerships with leading global biopharma companies, generating a broad and late-stage pipeline of innovative drug candidates. Based on our extensive track record of execution and delivering results, Zai Lab has earned the reputation as a trusted partner of choice for global biopharmaceutical companies seeking to not only access the Chinese market but also find a long-term strategic partner for global clinical development. Through these partnerships, Zai Lab has built the strongest late stage oncology portfolio among innovative Chinese biotech companies, with global first-in-class and/or best-in-class profiles. We are further supplementing our pipeline with an in-house discovery effort aiming to produce 1-2 global INDs [investigational new drugs] per year. Zai Lab is rapidly expanding into a fully integrated biopharmaceutical company, discovering, developing, manufacturing and commercializing innovative medicines. To that end, we have built our internal R&D centre to advance our discovery pipeline, a strong clinical development and operations team, and our own manufacturing facilities in China. We have also established a highly specialized commercial team to support marketing of our innovative products in China. We believe this integrated approach will provide sustainable competitive advantages for Zai Lab.”

As with BioGene exciting developments are coming thick and fast. Here is what the company has announced since last September. NMPA [National Medical Products Administration in China] approval of Zejula for first line maintenance treatment of ovarian cancer for patients in China; a secondary listing for the shares in Hong Kong; phase 3 NORA data for Zejula demonstrating significant PFS benefit, regardless of biomarker status with an improved safety profile when given with individualised starting dose regimen in Chinese women with platinum-sensitive recurrent ovarian cancer [it is the company’s ability to achieve these results that makes western biopharmas so eager to partner with Zai]; first patient dosed in China in a global phase 3 study of retifanlimab in patients with NLCSC [non small-cell lung cancer]; first patient dosed in Greater China in the global phase 2/3 MAHOGONY study of Margatuximab in gastric and gastroesophegal junction cancer; first patient dosed in China in a potentially registrational study of Retifanlimab in patients with endometrial cancer; Zai Lab partner Five Prime Therapeutics announces Bemarituzamab plus chemotherapy demonstrates significant progression-free and overall survival benefit compared to placebo plus chemotherapy in front line advanced gastric and gastroesophegal junction cancer; appoints Alan Sandler, MD as president, head of global development oncology; partner, MacroGenics, announces FDA approval of MARGENZA for patients with pre-treated metastatic HER-2 positive breast cancer; Zai Lab and Cullinan Oncology announce strategic agreement and license collaboration for CLN-O81 in Greater China; announces inclusion of ZEJULA in China’s national reimbursement drug list; announces strategic collaboration with Argenx for Efgartigimod in Greater China and a broader collaboration with partner Turning Point, a quoted US biopharma.

China is now the home to some of the fastest-growing companies in the world including the selection featured here. Like American businesses they have the advantage of a large home market, which means they can grow big at home without even addressing overseas markets but once they do go global they have the scale and cost efficiencies to compete. So far there hasn’t been much impact by Chinese companies outside their home turf but maybe they have their hands full at home. Consider this quote from a survey of Chinese consumers by management consultancy, McKinsey & Co. “The overall pace at which Chinese consumption has grown is almost hard to imagine: just a decade ago, most urban Chinese had enough money to cover basic needs like food, clothes, and housing (92 percent had annual household disposable incomes of 140,000 renminbi or less). Today, half are living in relatively well-to-do households (annual disposable incomes of 140,000 renminbi to 300,000 renminbi) where they have ample funds for perks like regular meals out, beauty products, flat-screen TVs, and holiday travel (300,000 renmimbi is around $46,500).

China has also been fast in adopting technology. Smart phone ownership in China reached 96pc in 2018 so 5G is going to have a huge impact and we have already seen the emergence of a string of giant technology and e-commerce businesses in China to rival what has happened in America. China now has over 700m people considered to be middle class and not only are their numbers still growing but their purchasing power is also rising rapidly, by around 12pc a year on some estimates.

On top of that there are often no legacy businesses in China thanks to the almost overnight switch from communism under Mao Tse Tung to ‘let 1000 flowers bloom’ capitalism under Deng Tsao Ping. Unlike say Russia, China also had the advantage of not possessing resources like oil so they had to develop proper businesses and the full panoply of a functioning capitalist economy to compete and prosper in world markets.

Against this background it is no surprise that China has become a fertile source of explosively growing emerging companies. Better still, the lack of a decent home stock market and undeveloped banking and investing systems mean that many of these exciting companies have chosen to IPO on Nasdaq. The combination of a Nasdaq quote with access to unlimited supplies of risk capital allied to the potential and the closed nature of the Chinese market has produced and is producing a string of explosively performing investments like BiliBili and Futu.

I am often wary of biopharma companies which so often end up as high risk bets on a single blockbuster drug. If the bet does not come off the shares can plummet. Part of the appeal of BioGene and Zai Lab Limited is that they haven’t bet the ranch on one single possible blockbuster but have an ever growing portfolio of drugs from which to generate high returns. They also have the priceless advantage of being a gateway able to offer western drug companies access to a huge, affluent and massively underpenetrated market in China. I cannot help feeling that, as a result, both BioGene and Zai, have something of a license to print money.

As Zai CEO, Samantha Du, said during their latest earnings report “Let me first say that at Zai, we have really built a strong reputation over the last few years as a partner of choice for western companies when it comes to this part of the world. And we also have a very robust business development pipeline currently in the backlog. And most of these are actually, by the way, inbound interests from, good, reputable U.S. companies. And a lot of them – the strategic objective for them to do a deal is really looking for help, not only to access the Chinese market quickly, but also to help them accelerate their global development.” The clear implication is that Zai is in a strong bargaining position, spoiled for choice and likely to announce many more deals and partnerships in coming months and years, ditto for Beigene, with its secret weapon in the form of an American-born CEO and founder. It is a great time to be a Chinese biopharma with a serious infrastructure in China, an opportunity to grow very fast indeed.

Many recently floated Chinese companies, like the four above, have relatively small free floats, which adds to the tendency for the shares to be volatile but also creates the potential for big long term moves.