Exciting times for markets and the QV portfolio – I look at seven star performers already in the portfolio and add two exciting new names

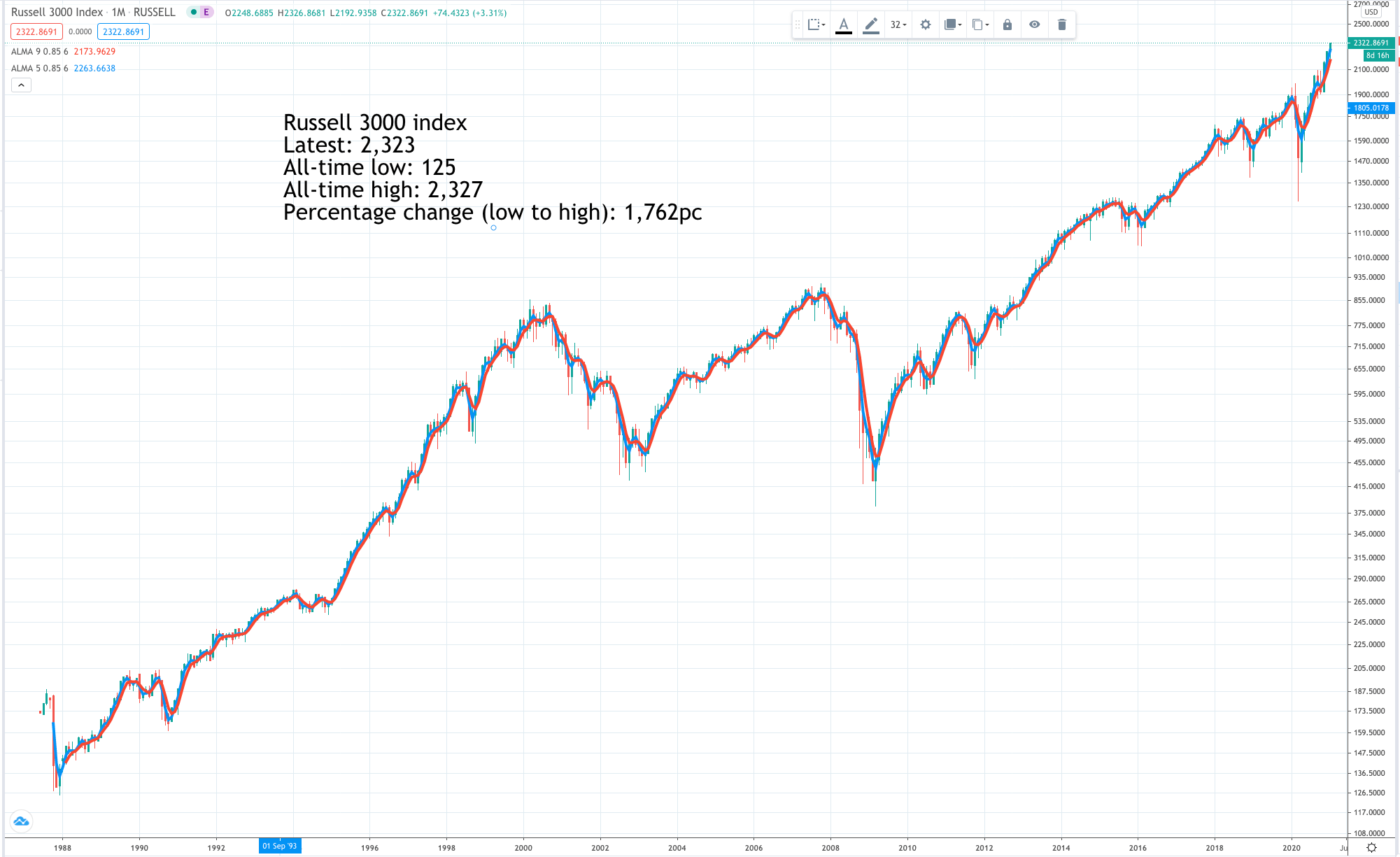

By way of a change I am showing the performance of the US Russell 3,000 index. There are three related indices, the Russell 1,000, the Russell 2,000, and the Russell 3,000, which is the 1,000 and the 2,000 combined so a bit like the UK’s FTSE All-Share index, albeit that has 350 constituents, the FTSE 100 plus the FTSE 250. The Russell 3,000 is all the shares quoted on US stock markets deemed suitable for institutional investment. The Russell 1,000 is the largest companies by market value and the Russell 2,000 is the next largest.

The index has performed very well since it was launched, up nearly 19 times since 1988 but that pales into insignificance against the performance of the Nasdaq Composite (most of the shares listed on the Nasdaq market), which is up 244 times since 1974 and 43 times since 1988.

And that is comfortably topped again by the performance of the Nasdaq 100 (the 100 largest shares in the Nasdaq Composite excluding financial shares), which is up 82 times since 1988.

These huge differences are mainly explained by the performance of technology shares, especially the giants like Apple, Alphabet, Amazon, Microsoft and Netflix. The Nasdaq Technology index, which is not so heavily weighted for the big tech giants, is up eightfold since launch in February 2006, which is slightly better than the 7.8 times gain delivered by the Nasdaq 100 and compares with the 3.1 times gain by the Russell 3,000 over the same period.

These performances may seem incredible; the Nasdaq Composite up 244 times since 1974 and the Nasdaq 100 up 82 times since since 1988 but it is partly explained by the miracle of compound interest, described by one financier as the eighth wonder of the world.

I was doing a quiz over Christmas with my son and one question was which would you rather have, £100,000 now or 1p, which doubled every day for a month. I did the calculations in my head and came up with the right answer. Stop reading now if you want to do the same. The answer is the penny, which incredibly, after doubling every day for 31 days reached over £10m!

This explains how shares can rise 10-fold, 100-fold and even 1,000-fold if the underlying business keeps growing at an impressive rate. It helps explain why I can be so aggressive with my recommendations even for shares that have already risen strongly. I know how far they can go if the execution is good enough and the opportunity is big enough.

Below are some shares, which I hope are going to demonstrate exactly what compound growth can achieve if sustained for long, albeit that is what I am looking for from all the shares added to the Quentinvest portfolio.

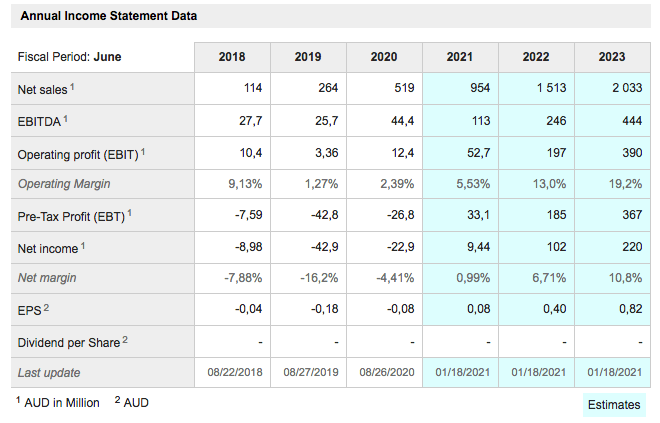

Afterpay APT Buy @ A$141 MV: A$38.2bn/ US$29.6bn Employees: 665 Next figures: 1 March Times recommended: 10 First recommended: A$54.52 Last recommended: A$113.50

I have illustrated the table because it shows how fast this business is growing. Analysts are looking for sales to rise from A$114m for 2018 to A$2,033m for the year ending 30 June 2023 and I am sure that even then the management will insist that they are just getting started.

Afterpay is a buy now pay later (BNPL) business, which dominates the ANZ market, is growing so fast in the US that market will soon account for 50pc of turnover, is also growing fast in the UK and Canada and has well developed plans to expand into continental Europe and Asia.

The BNPL space is hugely competitive. Klarna is the leading UK player by number of customers and, in North America, Paypal has entered the market in the US and Shopify from Canada. The reason I like Afterpay is that I think they are the most focused, the most ambitious in this space and will deliver the best execution.

The guys who founded and run Afterpay, Anthony Eisen and Nick Molnar, are amazing. The latter is still only 30. Their service is loved by their customers and by the merchants, who sign up with them. I expect Afterpay to become huge and to use its key role in the payments space to grow into other areas.

People say Afterpay should be worried by Paypal, which is 10 times bigger. I sometimes wonder if Paypal shouldn’t be worried by Afterpay although most likely the market is so huge there is plenty of room for both and it is traditional banks who should be worried.

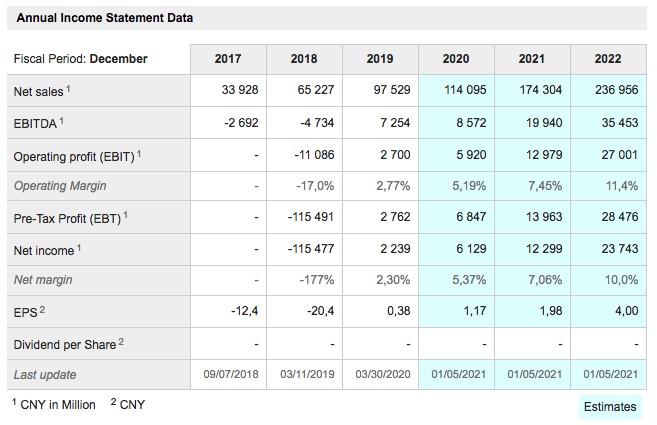

Meituan 3690 Buy @ HK$380 MV: HK$2,177bn/ US$280bn Employees: 54,580 Next figures:15 March Times recommended: 4 First recommended: HK223 Last recommended: HK$302

Again the table tells a very strong story with sales projected to rise some eightfold in five years, while ebitda (earnings before interest, tax, depreciation and amortisation) goes from negative to seriously positive. It is incredible to think that a business founded in 2010 could already be valued at US$280bn and have nearly 55,000 employees.

Meituan is the largest food delivery platform in China, which makes it the largest in the world. It has built a vast army of bike-peddling couriers and has already come a long way from its beginnings as a Groupon copycat. What adds to the excitement of Meituan as a company is that it has already been described as one of the world’s most innovative businesses and clearly intends to use its existing platform as a launchpad to expand into related areas and build an even larger business.

It is also doing this in the perfect place as China’s domestic consumer market is in a phase of explosive growth that still looks at an early stage. Meituan is by no means the only Chinese company experiencing hyper growth but it ticks all the boxes for a very exciting investment.

In reading the table above note that US$1 equals CNY (CHinese renmimbi) 6.45.

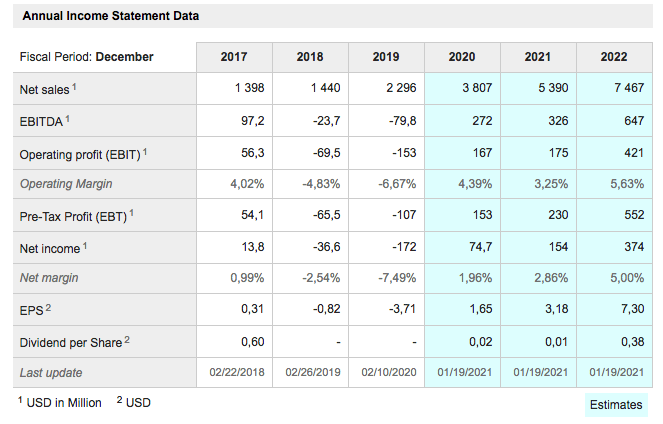

MercadoLibre MELI Buy @ $1925 MV: $97bn Employees: 9,703 Next figures: 25 February Times recommended: 13 First recommended: $316.17 Last recommended: $1650

Another sensationally fast growing business, MercadoLibre (MELI) can be thought of as a South and Central America cross between Amazon and Paypal, so much so that the latter company cleverly invested $750m in MELI back in March 2019, as part of a $1.8bn fund raising by the latter.

Covid-19 lockdowns have accelerated growth at ecommerce businesses like MELI but the results are still astonishing.

“MercadoLibre’s consolidated gross merchandise volume growth accelerated to 117pc year on year on an FX-neutral basis. At the regional level, Brazil and Argentina accelerated to 74pc and 242pc respectively. Mexico’s performance is notable given how COVID-19 impacted the region, delivering yet another quarter of GMV growth above 100pc year on year.”

The payments business, Mercado Pago, is growing exponentially.

“Mercado Pago reached almost 60m unique payers during the quarter, adding 7.5m payers, mainly attributable to Brazil. FX-neutral consolidated total TPV [total payments volume] grew by 161pc year over year during the quarter. Our off-platform payments business accelerated sequentially to 197pc year on year, not only with a robust performance of online payments, but also an improvement in our in-store payment solution, particularly mobile point-of-sale devices.“

FX-neutral is important in south and central America because so many countries have weak local currencies.

MELI says “the opportunity ahead of us remains sizable, and we feel increasingly confident that we can capitalize on it.” I couldn’t agree more.

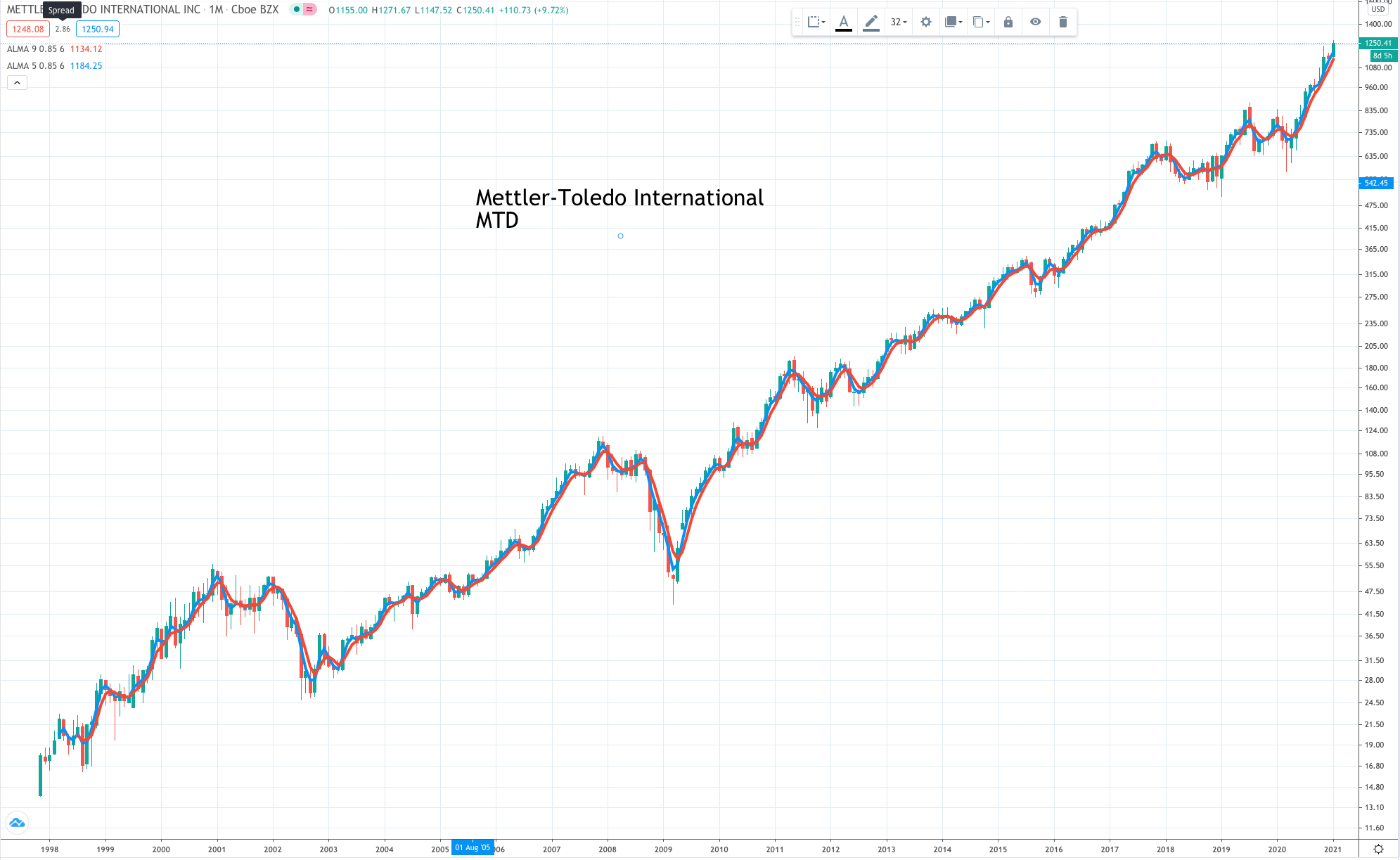

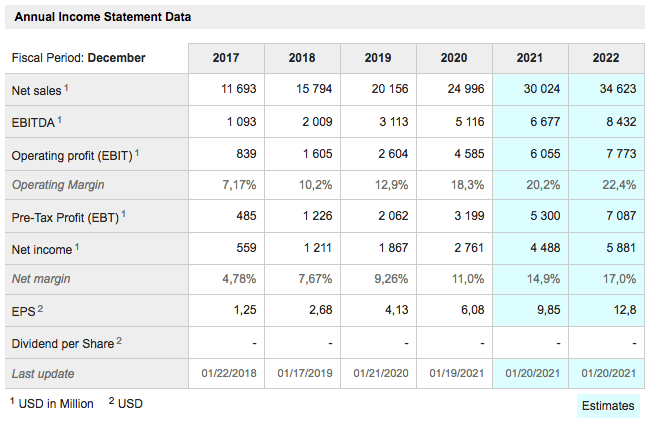

Mettler-Toledo International MTD Buy @ $1235 MV: $29.75bn Employees: Next figures: 4 February Times recommended: 2 First recommended: $1145 Last recommended: $1176

In the case of Mettler-Toledo (MTD) the chart tells the story. MTD is the ultimate stayer, not quite the tortoise that catches the hare because it often grows quite fast but the very long-term performance is astonishing. Since the shares joined the stock market in November 1997 the price has risen 90 times. It looks odd-on to become what famous fund manager, Peter Lynch, would call a 100-bagger.

The company supplies lots of bits of kit that you need in a laboratory. Many of them are consumables, twhich don’t typically cost that much so nobody bothers to shop around. All their stuff is good quality, the service is excellent and because they are not especially price sensitive, profit margins are excellent. In recent years the operating profit margin has ranged between 24.1pc and 27.2pc.

MTD has very strong free cash flow as you would expect from a business which effectively operates loads of mini monopolies but another twist in the tale is that they have never paid a dividend and probably never will. Instead they are the king of share buybacks.

As the CFO noted with the latest Q3 2020 results. “We now expect full year free cash flow to be in the $600m range and to repurchase approximately $775 million of shares in 2020.” And that is expected to rise to $850m worth of share buybacks in 2021, which is significant for a business valued at under $30bn.

Another attraction of MTD is the exposure to fast growing developing markets. China alone accounts for around 18pc of sales.

The shares may not do that much in any given year but over a decade you can expect a sensational result. The CEO is called Olivier Filliol and the headquarters are in Switzerland, which no doubt helps persuade the customers of the precision engineered quality of the products.

Nasdaq Inc. NDAQ Buy @ $139 MV: $23.1bn Employees: 4,776 Next figures: 27 January Times recommended: 5 First recommended: $92.50 last recommended: $129

As an investment Nasdaq Inc., which is the Nasdaq counterpart to London Stock Exchange plc in the UK, is not a bad proxy for the performance of the underlying Nasdaq market. Since 2009 the shares are up almost 10 times and the Nasdaq Composite is up around 11 times. You might have thought it should have done better but so far that hasn’t happened. However if you comnpare Nasdaq Inc. to the FTSE 100 since 2009 the latter has less than doubled so for a UK investor Nasdaq Inc. makes an outstanding investment.

It may also do better in future because of the growing activity around the Nasdaq market. The pace of IPOs is stepping up smartly and trading volumes are rising. These are important positives for Nasdaq Inc. and should generate substantial revenues.

If a full-on raging bull market develops and despite what you might think that has not yet happened, Nasdaq Inc. would do very well. As CEO, Adena Friedman, noted “Nasdaq delivered another quarter of strong performance, driven by great efforts by our team, coupled with favorable market conditions. We welcomed 105 IPOs to Nasdaq during the period, which represents the highest number of IPOs for a quarter on a US exchange in the past decade. Conviction by investors to increase exposure to Nasdaq’s focus of thematic indexes, coupled with robust market performance, continues to support our expanding Index business. As a result, we saw the AUM [assets under management] in our Index products achieve another quarter of record highs alongside high-trading activity in Nasdaq licensed index derivatives.”

The other thing to note from the table above is that Nasdaq Inc. does pay dividends and they are growing very nicely. In a world of near zero interest rates an upwardly mobile dividend is something well worth having.

Netflix NFLX Buy @ $571 MV: $253bn Employees: 8,600 Next figures: 19 April Times recommended: 20 First recommended: $174.53 Last recommended: $535

Netflix has been a long time favourite of mine. It has already been alerted 20 times in Quentinvest and if we go back before the launch of Quentinvest to include Quantum Leap and Chart Breakout (now known as Great Stocks and Great Charts respectively) it has probably been recommended over 50 times starting at $9.43 (adjusted for a subsequent 7:1 share split) in 2010.

I thought Reed Hastings was a genius almost from the first time I came across him and he now has the equally talented Ted Sarandos as co-CEO as well as being chief content officer.

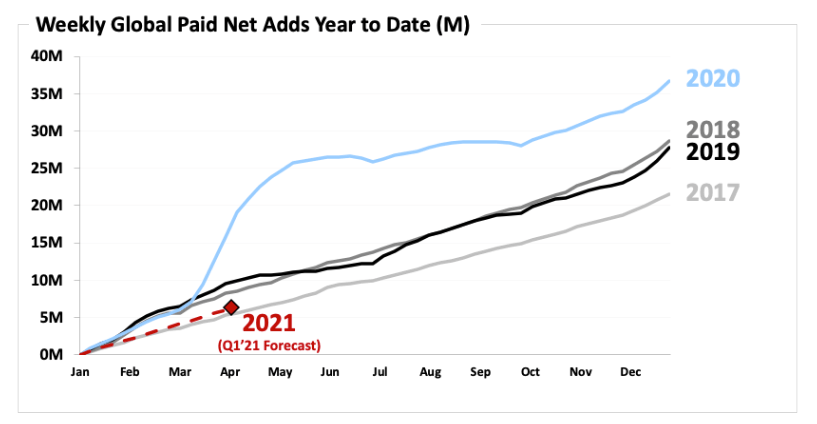

The company which invented the streamed video paid for by monthly subscription business model has had an outstanding 2020 as you can see from the chart below.

“For the full year, our 37m paid net additions represented a 31pc increase from 2019’s 28m paid net adds.We’re becoming an increasingly global service with 83pc of our paid net adds in 2020 coming from outside the UCAN (US and Canada) region. Our EMEA (Europe and Middle East) region accounted for 41pc of our full year paid net adds, while APAC (Asia Pacific) was the second largest contributor to paid net additions with 9.3m (up 65pc year over year).

The Netflix service is brilliant. It is good value; it is easy to sign up and to cancel; and the content, much of it original to Netflix, is very good. My family subscribes to Netflix with a family package, so five people can watch simultaneously different things on different screens, and we are regular viewers. We also have Amazon Prime and my daughter has Disney+ and all together they are still fantastic value versus things like cable TV; hence the massive cord-cutting (cancelling cable) taking place in the US.

The global opportunity looks enormous. Worldwide there are something like 4bn smart phone users. Against that number Netflix’s 200m subscribers still looks modest. I fully expect them to cross a billion subscribers one day not least because the more their revenues grow the greater their ability to create stunning original content adding further fuel to their virtuous circle/ flywheel effect.

Meanwhile you can see from the table above that after years of losses earnings per share are projected to grow dramatically. This plus ever strengthening cash generation means the group could soon be able to fund share buybacks. “As we generate excess cash, we intend to maintain $10B-15B in gross debt and will explore returning cash to shareholders through ongoing stock buybacks, as we did in the past (2007-2011)”.

I have always loved Netflix\s confident long-term approach.

“Our strategy is simple: if we can continue to improve Netflix every day to better delight our members, we can be their first choice for streaming entertainment. This past year is a testament to this approach.Disney+ had a massive first year (87m paid subscribers!) and we recorded the biggest year of paid membership growth in our history.”

Sea Limited SE Buy @ $233 MV: $83.7bn Employees: Next figures: 2 March Times recommended;7 First recommended: $79.80 Last recommended; $198

Sea Limited, a South East Asian gaming, ecommerce and online payments business, is another extraordinarily fast-growing business. Covid-19 and the lockdowns it has necessitated may have accelerated growth but the company was already expanding at a ferocious pace and is bursting with ambition.

The company has first mover advantage in the region in each of its three main divisions and also benefits from an outstanding top management team. The senior management team all look ridiculously young to me with only 43 year old CEO and founder, Forrest Li, showing even the faintest hint of a line on his forehead. Half the rest look like teenagers and like him they are all highly qualified. Li, who is Chinese-born, has a degree in engineering from Shanghai University and an MBA from Stanford.

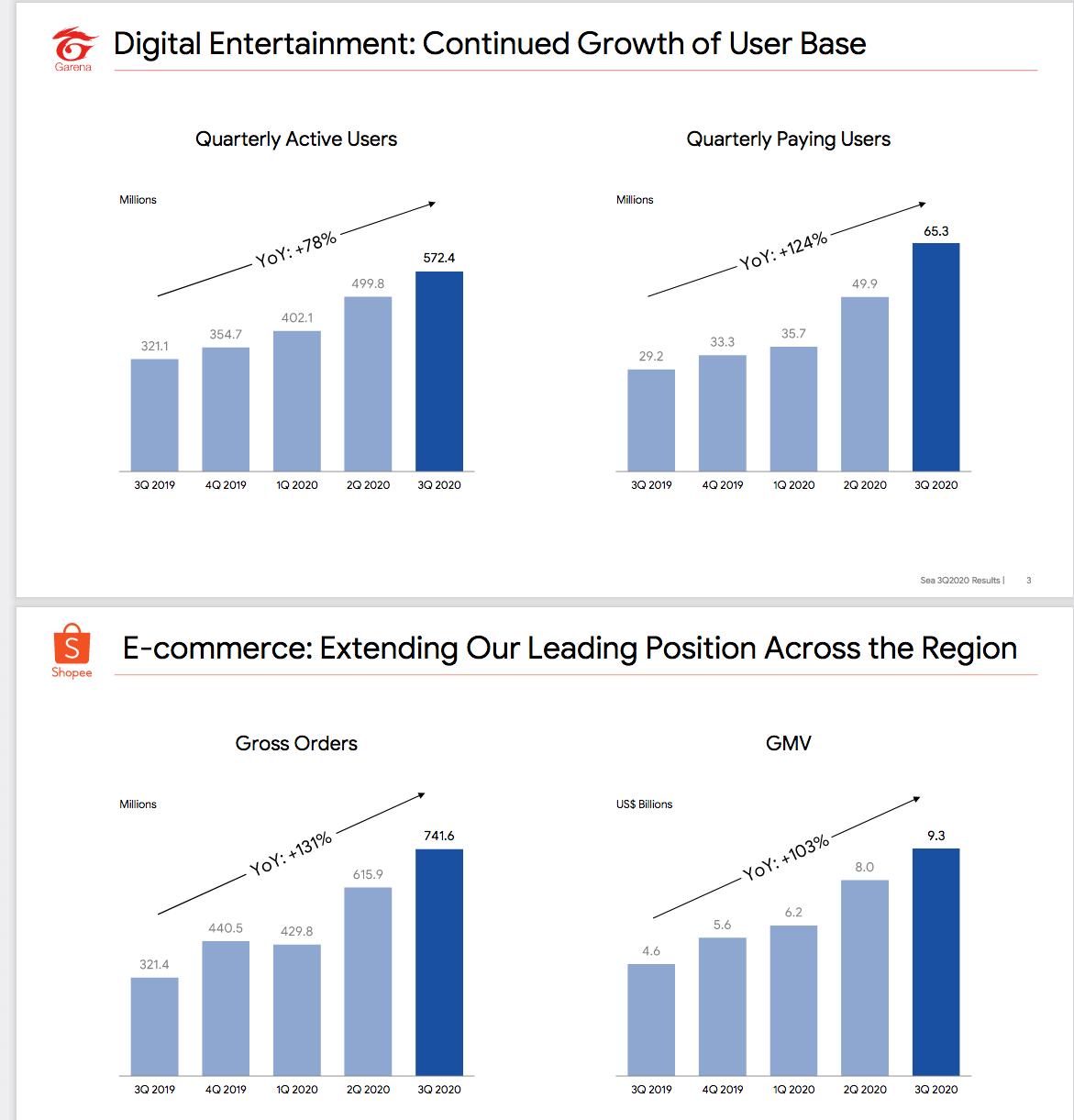

Q3 2020 results portrayed a business on fire.

“We continued to see robust user growth and deepening of user engagement on each of our platforms during the quarter. We believe the accelerating shift to digitalisation in our global market is a sustainable trend. As the market leader in our core segments, we are well positioned to capture the growth opportunities presented by this acceleration. Quarterly revenue grew 99pc to $1.2bn. Gross profit grew 101pc to $407.6m. We also recorded very strong bottom-line results, with adjusted EBITDA reaching $120.4n. This further demonstrates the strength and efficiency of our business model. We will continue to drive rapid growth with efficiency as we further extend our market leadership. In line with our strong results, we are raising our guidance for both digital entertainment and e-commerce for the full year of 2020.”

The cash cow of the business is online video games. Indeed Sea’s gaming business, Garena, generally and its Free Fire game particularly, are absolute phenomena.

“The third quarter was another standout quarter for Garena with strong performance across all our key metrics. Bookings were $944.7m, up 110pc. Adjusted EBITDA was $584.5m, up 120pc, representing 62pc of bookings. Quarterly active users reached 572.4m, an increase of 78pc. Quarterly paying users reached 65.3m, up 124pc and representing over 11pc of quarterly active users. We are particularly encouraged by the strong active and paying user growth for the quarter. This reflects our ability to continually deliver high-quality content that attract and engage users.

Free Fire sustained its strong performance. According to App Annie, it continues to be the highest grossing mobile game in Latin America and Southeast Asia in the third quarter. A key factor in Free Fire’s continued success is our ability to constantly deliver high-quality content tailored for the taste and the preferences of our huge global user base. In recent months, Free Fire partnered with celebrities such as Bollywood actors and global artists to create playable characters and other in-game content inspired by these celebrities. For example, in September, we released a playable character of a Bollywood star who was the lead actor in the highest grossing Indian film in 2019. We have also worked with a popular global artist to create another song exclusively for Free Fire which is a play inside game. Within two weeks of being launched, the song was streamed more than 25m times across various online platforms. We introduced more social and community features into the game. Free Fire’s tournaments held during the quarter have accumulated over 150m online views to date. In August, we hosted a national tournament for Brazil spanning two months. This tournament has recorded over 47m online views to date. We are also extending the reach of our e-sports events beyond our strong online audience. The grand final for Free Fire Indonesia Masters 2020 Fall was broadcasted on national TV reaching an even broader fan base, online and off-line. Our highly local and interactive content and community activities increase the ability of our users with Free Fire. These efforts also ensure that game stays fresh and relevant for our users over time. This, in turn, grows our user base and improves engagement.“

The cash generated by the hugely successful gaming business is fueling the expansion of Sea’s ecommerce, Shopee, business.

“We continue to capture more share of our region’s rapidly expanding e-commerce segment. We also continued to deliver more value to our sellers and buyers, while deepening monetization and driving efficient growth. Shopee recorded 741.6m gross orders, up 131pc, and GMV of $9.3bn, an increase of 103pcr. Revenue for the third quarter was $618.7m, up 173pc. We also continue to drive efficiencies across the business with adjusted EBITDA loss per order decreasing by 48pc to $0.41 during the quarter. In the third quarter, Shopee continues to rank as the No. 1 in the shopping category across Southeast Asia and Taiwan by download, average monthly active users and the total time spent in app on Android based on App Annie. On a global level, Shopee was also the second most downloaded app in the shopping category according to App Annie. In our largest market, Indonesia, Shopee continues to further extend its market leadership. It registered over 310m orders at a daily average of around 3.4m orders, an increase of over 124pc year on year. It was also ranked 1st in Indonesia for average monthly active users, downloads and the total time spent in app on Android in the shopping category in the third quarter, according to App Annie. As e-commerce growth is important across the region, we have been focused on delivering more value for our merchants across the Shopee ecosystem.”

Last but not least is the explosive growth of SeaMoney, the online payments business.

“Moving on to SeaMoney. We saw the same strong growth momentum across Garena and Shopee during the quarter. Our mobile wallet total payment volume for the quarter exceeded $2.1bn with quarterly paying users surpassing 17.8m. SeaMoney continues to deepen its integration with Shopee, leveraging Shopee’s rapid growth and extensive reach to scale efficiently and effectively. In October, more than 30pc of Shopee’s total gross orders across our market combined were paid using our mobile wallet. We also continued to expand our suite of online and off-line third-party use cases and partnerships in the third quarter. This has further increased the usage and the brand awareness of SeaMoney across our community. We see a significant opportunity ahead of SeaMoney and believe that we can capture it in a highly efficient manner by building on our core use cases. Our focus remains on building the business to enable more consumers and the merchants to benefit from the ease and convenience of our digital solutions. In closing, the strong momentum from the first half of the year has carried on into the third quarter and beyond. Our third-quarter performance is a testament to our ability to quickly adapt to the rapidly evolving needs and the preferences of our community.”

No surprise that management says – “Our conviction in the scale of the opportunities ahead for Sea over the long term is growing even stronger.“

Sea Limited looks to me like a giant company in the making and still at an early stage of its corporate journey.

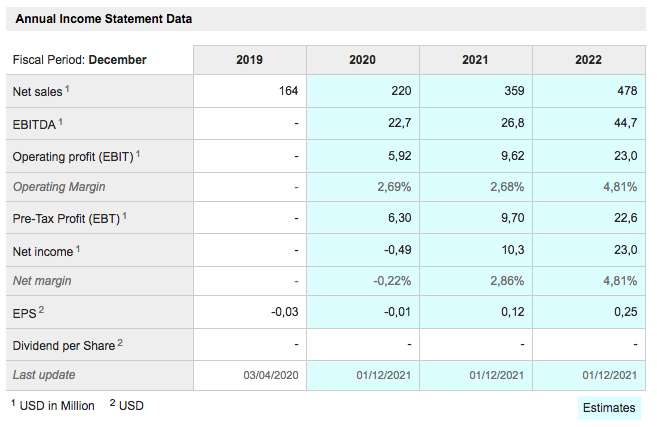

Upstart Holdings UPST Buy @ $62.50 MV: $4.6bn Employees: Next figures: 3 March New entry

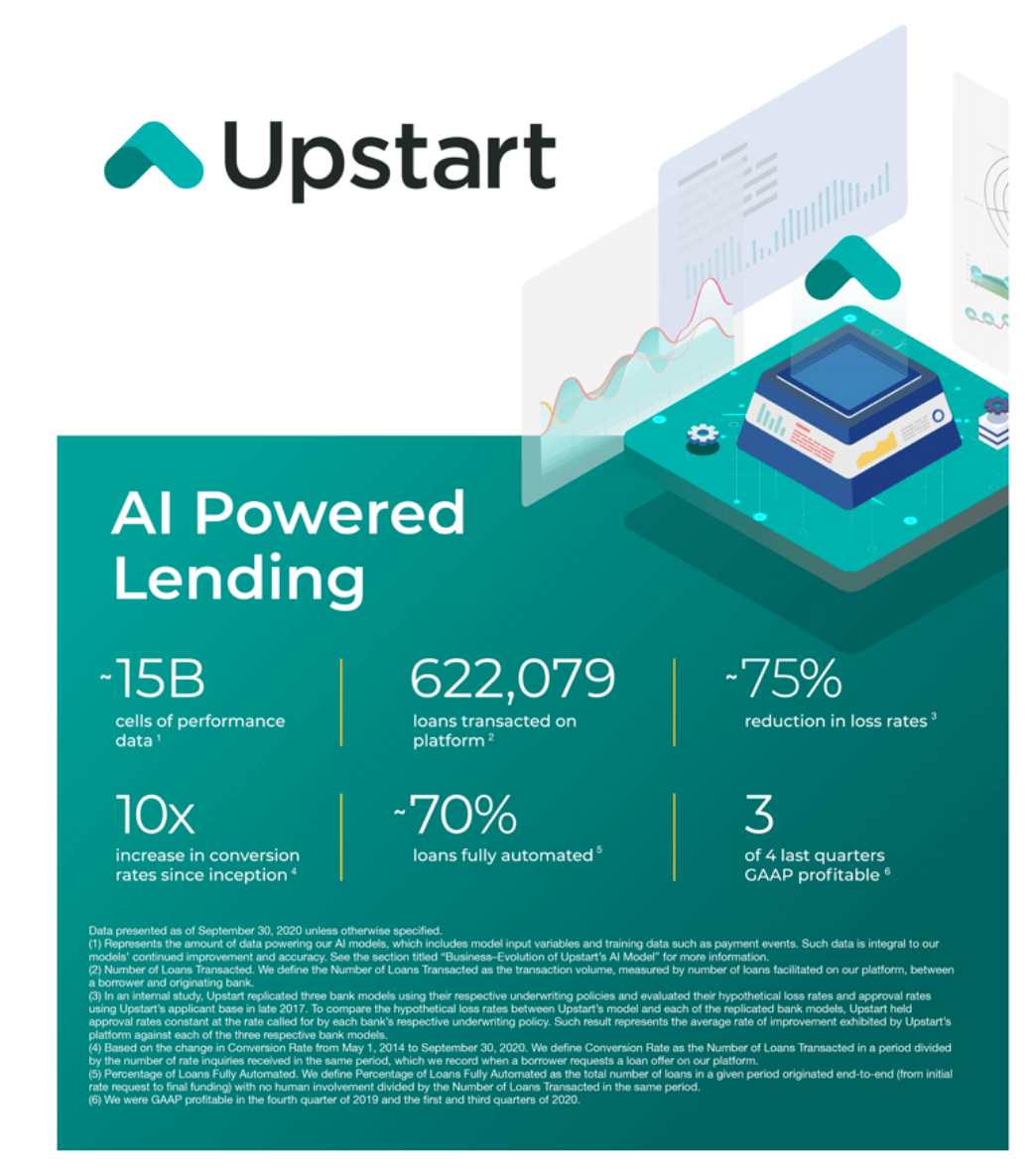

Upstart Holdings is a very recent IPO and the shares have already more than trebled from the IPO price. The trigger for the latest move was the announcement of a new banking client. “Upstart, a leading artificial intelligence (AI) lending platform, today announced that Oriental Bank, a subsidiary of OFG Bancorp and one of the largest banks in Puerto Rico, has selected Upstart’s Credit Decision API (application programming interface) to deliver faster credit decisions and more accurately price auto loans for applicants on its online banking site.” The shares rose over 15pc on the day.

“Incorporating more than 1,600 variables, Credit Decision API leverages machine learning algorithms trained on more than 620,000 loans and more than 9 million repayment events across Upstart’s network of bank partners. Compared to traditional bank models, AI-enabled decisioning can provide banks with up to 75pc fewer defaults at the same approval rate.*

The graphic below, taken from the prospectus, shows the results being achieved by Upstart and the reason why a bank would be interested in using their software.

Upstart was founded in 2012 by three ex-Googlers, Dave Girouard, former president of enterprise at Google, Paul Gu, a Thiel fellow [founded by technology entrepreneur and investor, Peter Thiel, in 2011, the Thiel Fellowship is a two-year program for young people, sometimes called 20 under 20, who want to build new things. Thiel Fellows skip or stop out of college to receive a $100,000 grant and support from the Thiel Foundation’s network of founders, investors, and scientists) and Anna Counselman, former manager of global enterprise customer programs and Gmail consumer operations at Google.

The company quickly gravitated to helping banks make three and five year loans. Upstart developed an income and default prediction model to determine creditworthiness of a potential borrower. This means that in addition to traditional underwriting criteria—FICO score, credit report and income—the Upstart underwriting considers academic variables—colleges attended, area of study, GPA, and standardized test scores—and work history to develop a statistical model of the borrower’s financial capacity and personal propensity to repay.

Investors in the company include such illustrious names as Eric Schmidt (former Google CEO) and Marc Benioff (founder and CEO of Salesforce.com).

As you can see from the table above analysts are expecting the company to grow rapidly and, unusually for 21st century enterprise software companies, the business is expected to be almost immediately profitable. More than two-thirds of Upstart loans are approved instantly and are fully automated.

The founders claim that the current system for awarding loans is badly broken, that although four in five Americans have never defaulted on a loan half of them fail to qualify for the lowest rates available. They say many people who are given loans end up defaulting, many people, who would not dream of defaulting cannot get loans and many of those who do get loans pay higher interest rates than they should.

I can vouch for this. I am a high earner, have significant assets beyond the home in which I live and have never defaulted on a loan but have not been able to borrow money from anybody, least of all Barclays, the bank I have used for decades, for many years because I do not fit their lending criteria.

Upstart’s simple plan is to use the latest technology, in particular the cloud and artificial intelligence, to automate and dramatically improve the system by which credit is appraised and loans are awarded. It sounds like a great plan, it appears to already be delivering impressive results and has the potential to disrupt a massive industry.

The founders believe the solution is all about using AI [artifical intelligence].

“AI has the potential to add $13 trillion to the global economy by 2030 and is broadly considered one of the most important developments in the history of technology. Last year Amazon’s Jeff Bezos said ‘we’re at the beginning of a golden age of AI. Recent advances have already led to inventions that previously lived in the realm of science fiction’.

Credit is a compelling and obvious case study for AI. First, lending involves sophisticated decision making for events that occur millions of times each day. Second, there is an almost unlimited supply of data that has the potential to improve the accuracy of credit decisions. Third, given the cost and risks associated with lending as well as the scale of the industry, the potential economic wins from AI are dramatic.”

They also note that “as good as our AI platform is today, we are only scratching the surface of what is possible“.

The opportunity for AI powered lending and hence for Upstart looks enormous. Their current focus is on the US market and personal loans. In December 2019 there were $4.2 trillion of loans outstanding across mortgages, auto loans, credit cards, personal loans and student loans and that virtally all could have been improved by AI.

In September 2020 the first Upstart-powered auto loan was originated. The auto loan market is both large – at least five times the size of the personal loan market – and inefficient with millions of borrowers paying interest rates that don’t reflect their true risk.

With their eight year head start the founders of Upstart believe their AI lending platform is well positioned to help power one of the largest transformations facing the financial services industry.

I think Upstart looks an exciting investment but subscribers should remember that recent IPOs can be incredibly volatile both up and down. I don’t think that matters too much for a long-term investor but it can be disturbing while it is happening.

Upstart’s strategy is not to compete with banks but to partner with them. They have been working for four years with one bank, Cross River Bank, to develop their systems and this bank still accounts for 72pc of their revenue in the first three quarters of 2020. However they now have 10 banks on their platform and there are 1000s of banks out there.

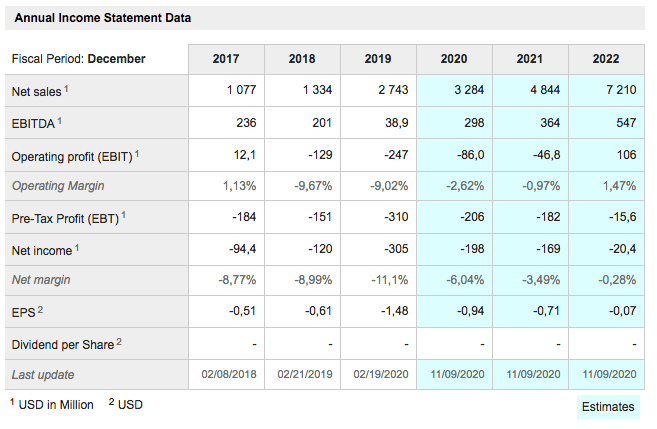

Zillow Z Buy @ $145 MV: $34bn Employees: 5,409 Next figures: 11 February New entry

I first became interested in Zillow years ago because I saw it as similar to the UK’s Rightmove but operating in the US with a much bigger market. The group was originally founded by four ex-Expedia employees, led by Rich Barton, who founded Expedia but he soon stepped up to become executive chairman of Zillow, leaving it to be run by another founder, Spencer Rascoff, who grew the business dramatically but failed to make it very profitable.

In late 2018 Rich Barton bought 700,000 more shares at low prices to add to his 15.8m share stake (now worth $2.3bn) and in early 2019 he returned as CEO and began to take the business in a new direction.

Zillow still offers free valuations through its Zestimates operation and generates revenue from real estate agents advertising properties on its platform but it is also becoming more directly involved in the transaction process.

It has launched a business called Flex, where it takes a fee from the transaction, only when a house is successfully sold over its platform. It has also launched a business called Zillow Offers where it uses Zestimates and other algorithms to value and buy your house from you and then sell it on, flipping the house as they call this process in the US.

The attraction for sellers is an immediate sale at close to the estate agent’s figure but without showings and settlement in days.

Zillow boldly predicts that in three to five years it will be buying 5,000 homes a month—1pc of all real estate transactions—and booking home sale revenue of $20bn a year, compared with $2bn or so from selling real estate ads on line. But most of the profit from the new business, as Zillow execs tell it, won’t come from marking up houses. “It is more important to price right when you buy the home than at the back end,” explains chief financial officer Allen Parker, who joined Zillow in 2018 after 13 years at Amazon. Instead, Zillow’s plan is to make more profits on auxiliary services, including title insurance and, most important, mortgages. If it’s selling 5,000 houses a month, it expects to finance loans on 1,650 of them.

The group says two tailwinds are driving the business – one in residential real estate and one in the adoption of technology. An increased desire and growing ability to move, as people rethink their relationship with home and work, is causing a Great Reshuffling across the U.S. All of this is happening as people are increasingly turning to new technology to safely navigate many aspects of their lives, including shopping for and buying their next home.

“Our team is executing in the rapidly evolving and still uncertain environment while keeping a firm focus on our long term opportunity, which is vast and nascent. We have built and cultivated a tremendous audience, with an average of 236m unique users coming to our platforms on a monthly basis, but we have much to do more before we transform the way residential real estate is transacted. Our Premier Agents, who are responsible for our biggest business today, handle only a small fraction of all real estate transactions. There is potential for meaningfully more growth as we continue to improve the customer experience and make more connections between our high-intent customers and our best-in-class, high-performing agents.Similarly, Zillow Offers makes up only a tiny fraction of all residential real estate transactions – just two-tenths of a percent. Most sellers are also buyers, so as more people consider selling to us, we are able to create a flywheel effect when they go to buy their next home. We are building adjacent services in both mortgages and title and escrow that drive market share and ecosystem economics as we spread our low customer acquisition cost across all of these services. This is our Zillow 2.0 vision for the future of real estate – seamless customer experiences across our products and services, which will deliver additional economic benefits to Zillow, capitalising on the customer trust we’ve spent so many years cultivating.We know home buyers, sellers and renters want a better way, and we are working to transform the industry.”

Ironically so far in 2020 the core Premier Agents business has been booming and mortage business is up 114pc but the house flipping business hit pause because of lockdown. Most striking has been the dramatic increase in users and visits detailed above. However business is picking up.

“Throughout Q3, we accelerated our activity, purchasing 808 homes and selling 583 homes. This reopening strategy was coupled with expansion to Jacksonville, FL in August, which is our 25th Zillow Offers market.We ended the quarter with 665 homes in inventory, up from 440 homes at the end of Q2. Our refined resale strategies, combined with the ongoing tailwind of a strong housing market, resulted in Homes segment revenue of $187m, exceeding the high end of our Q3 outlook.”

One would have to say that the jury is still out on Zillow Offers, the home flipping strategy but meanwhile the core Premier Agents business is trading brilliantly with Q4 2020 revenues expect to increase by 31pc to between $300m and $310m.

The group is optimistic on prospects. “The third quarter saw continued momentum in the housing sector, a trend we expect to continue for the foreseeable future as more and more people are seeking new places to live and are more readily adopting technology solutions to get them there. In addition to these tailwinds, we are executing well and delivering great results.”

I am inclined to give them the benefit of the doubt and assume that under Rich Barton their plans to transform the US housing market are going to be successful. If they are these shares are going much higher.

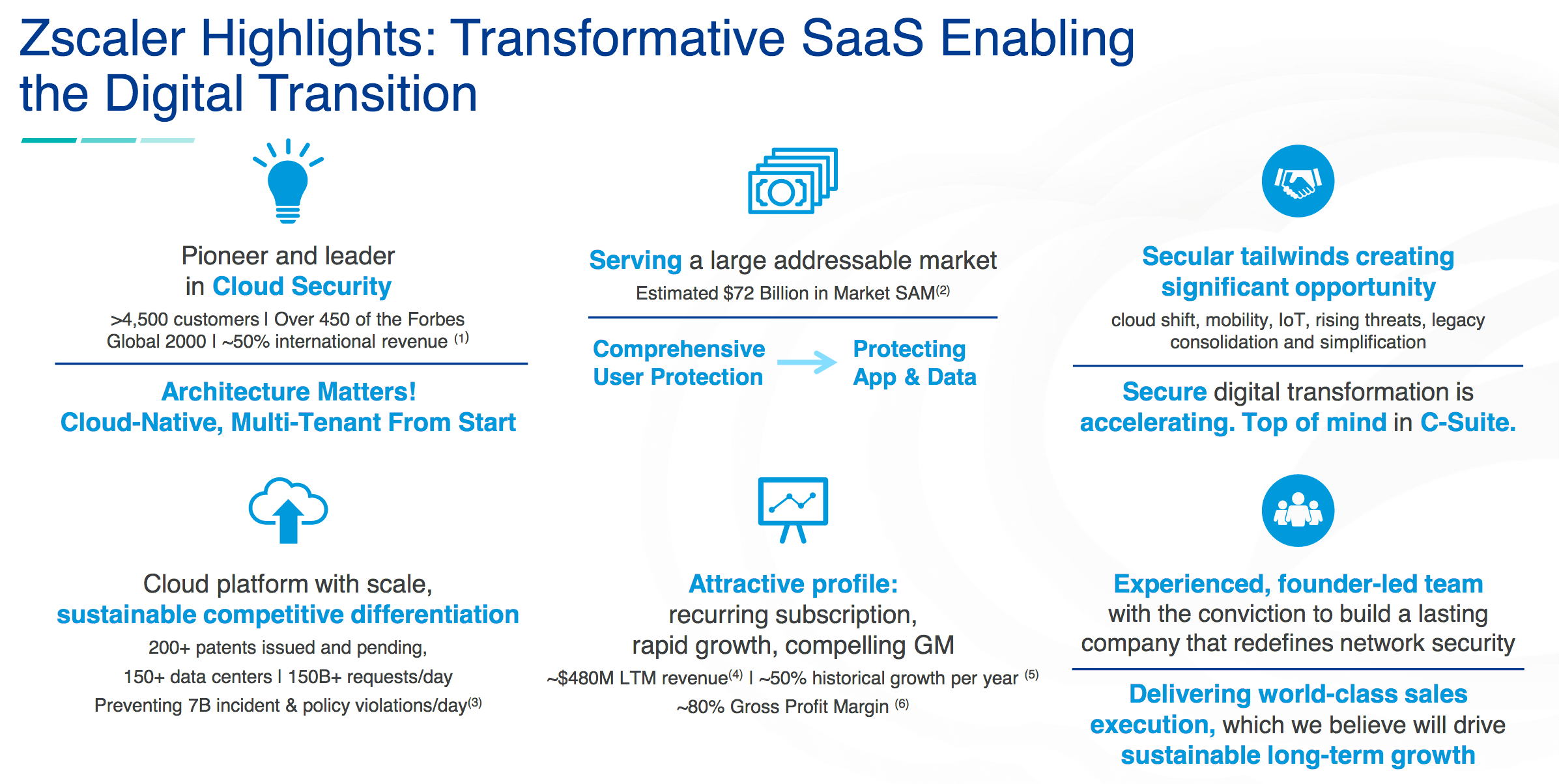

Zscaler ZS Buy @ $214 MV: $28.6bn Employees: 2,020 Next figures: 4 March Times recommended: 10 First recommended: $60 Last recommended: $180

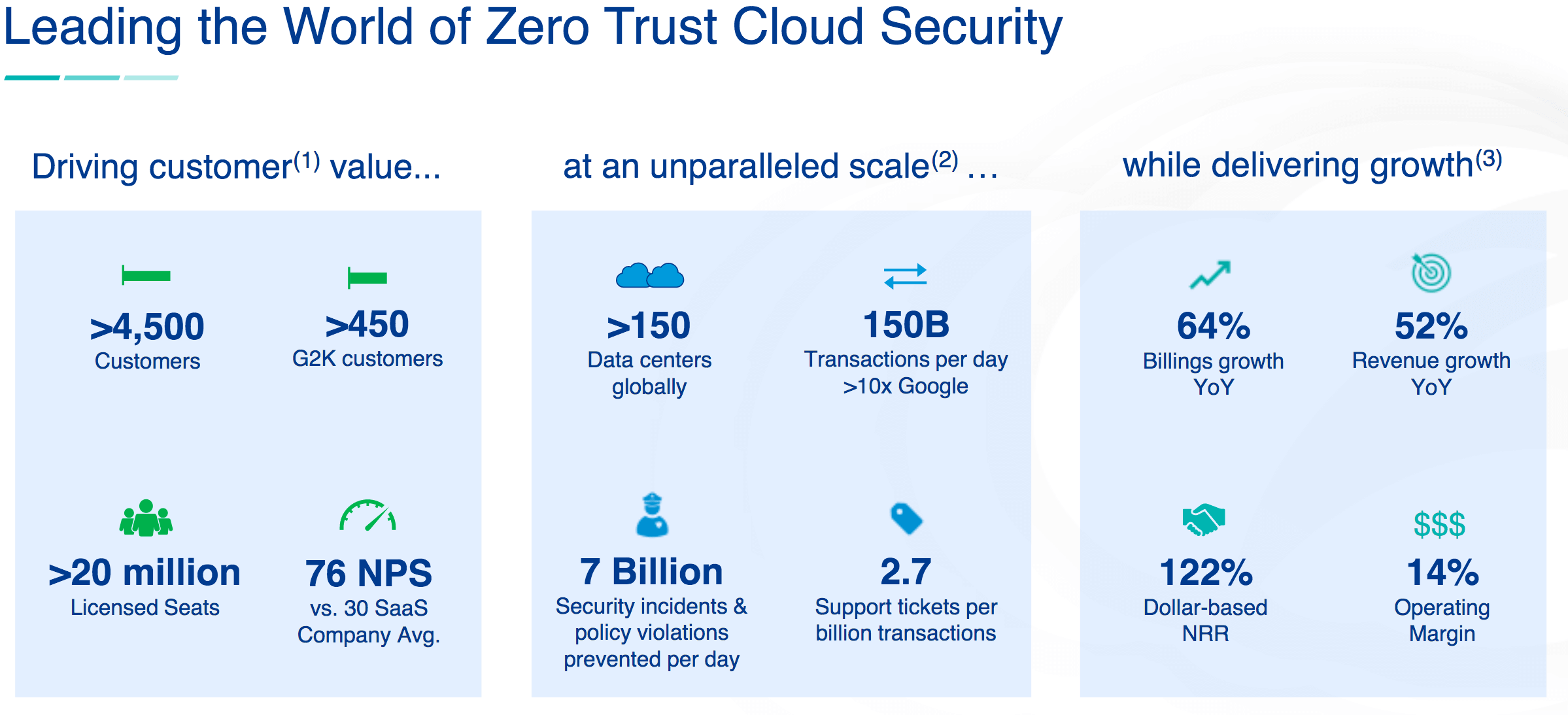

The graphic above is from Zscaler’s January 2021 analysts’ day. It alone makes a strong case for buying the shares. Recurring revenue, 50pc historical growth, 80pc gross margins and a $72bn and climbing addressable market. What’s not to like.

Part of the point about Zscaler is that it is a cybersecurity business built from and for the cloud. They say this makes it very hard for legacy cyber security companies to compete with them and their growth certainly tells a story. Founded in 2007 the group is on course to deliver sales over $1bn in the year to 31 July 2023.

Some of the standouts from the graphic above, also taken from the analysts’ day, are the scale of the business, handling 10 times as many transactions a day as Google and the low amount of support required, just 2.7 tickets per billion transactions. An NPS, net promotor score (would your customers promote you to another potential customer) above zero is good, above 70 is sensational. A 122pc dollar based NRR [net retention rate] of 122pc means that your customers at the beginning of the year increase their spend by 22pc over the year with new customer wins generating growth on top.

The big picture of why Zscaler is doing so well is the growing need for cyber security in an increasingly connected world. This is why the market is huge and why enterprises, public bodies and even smaller concerns have to take cyber security seriously.

Part of the reason why Zscaler has such an opportunity is not just that its technology was created for a cloud-centric world but also because after successfully targeting larger corporations it is now turning its attention to smaller as well as very large organisations.

CEO and founder, Jay Choudhery, refers to “four key pillars with each enabling a critical element of the transformation. ZIA to secure direct access to the internet and SaaS, ZPA for zero trust access to private applications, Zscaler Digital Experience, or ZDX to deliver user experience for work from anywhere and cloud workload segmentation to protect applications. An increasing share of our sales is coming from initial platform purchases by new customers and also growing upsell to existing customers, which is driving a record 122pc net retention rate. I believe in the current challenging environment and in the post-COVID economy, Zscaler will be the go-to platform, our vendor consolidation, cost savings, increased user productivity, and better cyber protection. We are excited about our mission to make the cloud a safer business and enjoyable for users.”

Covid-19 and work from home has given a powerful boost to already strong demand.

“Many CxOs (a chief experience officer is an executive responsible for the overall experience of an organization’s products and services) shared with me that their current work from home environment while temporary has helped them realize that zero trust architecture is the future and it can be implemented easily and rapidly. COVID was a catalyst in changing the mindset and shaking off inertia, resulting in a reduced need for educating customers about the value of the Zscaler architecture over legacy approaches. Inbound customer requests have greatly increased, and we are becoming an integral part of a growing number of larger transformation projects. We continue to see more customers buying ZIA and ZPA together, which enables a true transformation with direct and seamless access to SaaS applications or applications in your data centre, or the public cloud.”

The issue for many investors is the valuation they have to accept when buying shares in companies like Zscaler. No dividend, no earnings and a market capitalisation that values the business at nearly 30 times projected sales for 2022-23. It is valuations like these that make the shares volatile but there is a reason why over time they keep climbing so strongly. Zscaler is in a virtuous circle of growth. The bigger it becomes the more powerful the business, the more outstanding the talent it can attract and the more it can do for its customers, putting it on a track to becoming a very large business indeed.

One way to think of the Quentinvest strategy is that each of the shares I pick is a bet on the underlying business one day becoming very large, or, if it is already large like Google or Amazon, on it becoming gigantic.

It is this approach which helps me be so relaxed about the current valuation. Almost any valuation will become reasonable if the company grows dramatically in size.

In the 1980s, I bought Body Shop shares on a price earnings ratio of 100, which was a stunning valuation at the time. In retrospect, it turned out that the shares were incredibly cheap as sales and profits rocketed higher. It happens so often in the stock market that the shares, which look most expensive, are actually the best value, while the shares that look cheap are fool’s gold.