I believe the best way, arguably the only sustainable way, to make money in the stock market is to buy and hold great stocks. The mindset of ownership and patience, allowing miracles to happen, is less stressful than trading and locks your performance into the underlying fundamentals of the companies in which you have invested. If the companies are well chosen for their quality and growth potential you should win in the end and win big.

However it is important not to be too static in your approach. A portfolio needs to be as dynamic as the stock market. There are new exciting companies joining the market and emerging all the time. You don’t want to miss out on these opportunities.

Four of the shares featured in this issue of ‘Great Shares’ are relatively new or very new discoveries for me. I like that because I am looking all the time so if a stock is a new discovery for me it is likely that most investors will not be aware of it either. This applies even if the shares have already done well. There are always some people, close to the business, who know what is happening but very often there is little awareness in the wider market. As that awareness grows the shares can rise, often significantly. This phenomenon is sometimes described as crowd theory.

Some shares, like Airbnb or Facebook, start with a high profile but most companies join the stock market with little fanfare.

However, if they are delivering strong growth, as many are in these exciting times, awareness will grow and the crowd following shares will become larger.

A bigger crowd means more buyers for the shares and more new money chasing a fixed supply, which means higher prices. There is almost a one for one link. Bigger crowd equals more buyers equals higher share prices.

If the company is really successful, an Apple, a Google or a Netflix, the buyers can keep coming even when everybody is part of the crowd and by that time the shares may have risen 10, 50, or a 100 times or even more.

Make sure to keep refreshing your portfolio by adding exciting newly discovered shares to your collection. This helps ensure you don’t miss out on important new trends and that you don’t get stuck with a portfolio full of yesterday’s stocks.

Additions to live portfolio

ASML /ASML

Buy @ $500(3)

Broadcom/ AVGO

@ $441(new)

Charles River Laboratories/ CRL

@ $268 (new)

Meituan Dienping/ 3690

@ HK$302 (3)

Lemonade/ LMND

@ $167 (3)

Keyence/ 6861

@ YY58,520 (1)

Natera/ NTRA

@ $108 (new)

Zai Lab Limited

@ $145 (new)

“In short, the global semiconductor market will continue to grow exponentially for the coming years.”

ASML

“”Through a series of strategic acquisitions and a steadfast commitment to R&D, Broadcom has grown to be one of the world’s leading technology companies.”

Broadcom

“The record EPS was driven by exceptionally strong operating performance as we emerged from the second quarter, which we believe will be the worst of the COVID-19 financial impact.”

Charles River Laboratories, 30 October 2020

“As one of the earliest adopters of the online-to-offline (O2O) business model in China, Meituan’s story is full of experimentation, adaptation, and reimagination.”

Analyst, 30 June 2020

“Pets may be our first step beyond homeowners’ insurance, but as you all see here, it won’t be our last.”

Daniel Schreiber, CEO and co- founder, Lemonade, 11 November 2020

“We view these global trends as having great potential for expanding our business, and to realize this potential, we will focus on applying the powers that we have cultivated over the years to achieve sustained growth.”

Keyence Corp, June 2020

“Q3 was another very strong quarter for Natera. The work we’ve been doing for the last 5 years has really started to deliver results.”

Steve Chapman, CEO, Natera, Q3 results, 5 November 2020

“With a broad and differentiated pipeline, we remain confident that Zai Lab can become a leading global biopharma company, leveraging our capabilities and network, to drive the next wave of innovation with transformative impact.”

Samantha Du, CEO & founder, Zai Lab Limited, 13 August 2020

ASML /ASML

US$

MV: $210bn

Employees: 24,749

Next figures: 20 January

Buy @ $500

If you think of integrated circuits as being printed on silicon wafers by photolithographic machines, a Dutch company, ASML supplies those machines and in 2010 had two thirds of the market. It involves continually pushing the envelope on innovative technology and positions ASML as a key player in an accelerating global technology revolution. The company is growing steadily and reinvests much of the cash it generates in share buybacks so the shares just keep climbing.

The company says:– “Based on different market scenarios, we have an opportunity to grow our annual revenue for 2025 to between €15bn and €24bn”.

Broadcom /AVGO

US$

MV: $180bn

Employees: 19,000

Next figures: 18 March

Buy @ $441

String of acquisitions makes shares in semiconductor giant, Broadcom, one of top US performers

Broadcom Inc. is an American designer, developer, manufacturer and global supplier of a wide range of semiconductor and infrastructure software products. Broadcom’s product offerings serve the data centre, networking, software, broadband, wireless and storage and industrial markets. Broadcom is one of the world’s best run semiconductor companies. The company has strong market share and technology positions across most, if not all, of the areas it serves, and that strength has paid off in the form of high revenue, robust gross margin, and a flood of free cash flow that it returns to its shareholders.

Annual Financial Data

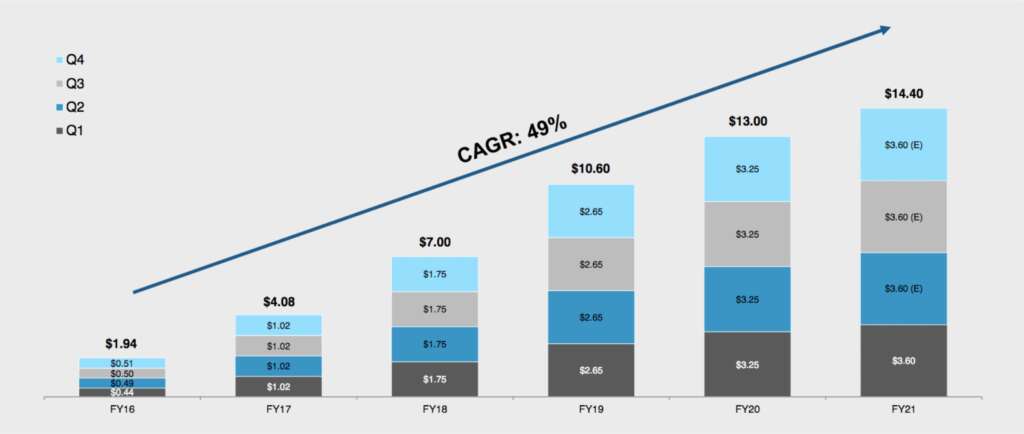

“We capped off fiscal 2020 with record quarterly revenue and profitability despite the ongoing pandemic and macroeconomic uncertainties. We delivered net revenue of $6.5bn, above the midpoint of our guidance and up 11pc sequentially and up 12pc year on year.”

Common Stock Dividend

One way for companies to deliver exceptional growth is to make acquisitions to supplement organic growth and boost profitability by cutting out waste and duplication in the enlarged business. Avago/ Broadcom has been doing this to such effect in the semiconductor industry that its shares have risen 32-fold since 2009.

It is a strategy that works particularly well in a sector which is already growing strongly providing a powerful tailwind for the enlarged business and helping to make the acquisitions look cheap as time passes.

Avago/ Broadcom has been especially active and was only stopped from buying Qualcomm for a mighty $130bn by an executive order from Donald Trump. In 2013, Avago Technologies, which began life as a spin-off from Hewlett- Packard, bought LSI Logic for $6.6bn. Then in 2016 it bought Broadcom for $37bn in cash and shares, changing its name to Broadcom but staying with the old stock market code, AVGO. In the same year the enlarged Broadcom bought Brocade Communications for $5.5bn. In 2018 it bought CA Technologies for $18.9bn and in 2019 it acquired Symantec’s enterprise software business for $10.7bn.

The result of all this activity is a powerful and much enlarged semiconductor business, supplying chips for Apple phones among other activities, which looks well placed for an expected strong period of growth in the semiconductor industry.

One sign of the strong growth of the business is the dramatic rise in dividends paid in recent years though there is an element of catch up and the growth is unlikely to continue at such a rapid rate. The group uses share buybacks as well as dividends to return cash to shareholders.

Despite challenging conditions in a pandemic- affected period the group continues to trade strongly. “We concluded the year with strong fourth quarter results driven by continued demand for networking from cloud and for broadband from service providers as well as the significant ramp in wireless, even as enterprise demand remained soft. Our infrastructure software segment continued to be stable and delivered solid results. Our first quarter revenue outlook, which projects continued overall strength, is expected to show 13pc year over year growth, all organic.”

Last but not least is the prospect of more acquisitions. Broadcom is already big but clearly intends to become much bigger in what is increasingly one of the world’s most important industries.

“Despite the challenges presented by the ongoing pandemic and macroeconomic uncertainties, we achieved record profitability, generating $11.6bn of free cash flow in fiscal 2020. As a result, we are raising our target common stock dividend by 11pc to $3.60 per share per quarter for fiscal year 2021.”

“Our backlog continues to grow. To give you a sense, I mentioned we have over $14bn of backlog today. When we started the quarter, our backlog — and we’re shipping in between since the beginning of the quarter, our backlog was $12bn. So, it’s accelerating. But having said that, please don’t get carried away in the other aspect. As you know, wireless business that we have is seasonal. So, we are seeing our wireless backlog is a significant part of the total backlog. But given the seasonality of it, we obviously have seen a deceleration in the bookings that are coming in from our wireless business. But we are seeing, on the other side, acceleration and continued strength in orders coming in from the other parts of our business. Networking has always remained strong. Broadband continues to be very strong. And now we start to see the smaller part of our business, industrial, coming in very, very strong.”

Charles River Laboratories /CRL

US$

MV: $13.5bn

Next figures: 16 February

Buy @ $268

If you can live with animal testing Charles River Labs plays key role in global pharma industry

Charles River provides essential products and services to help pharmaceutical and biotechnology companies, government agencies and leading academic institutions around the globe accelerate their research and drug development efforts. Employees are focused on providing clients with exactly what they need to improve and expedite the discovery, early-stage development and safe manufacture of new therapies for the patients who need them.

“Cellero has enhanced our access to high-quality, human-derived cellular products, both from healthy donors and patient populations. And expanded our geographic reach with donor sites in both Eastern and Western United States. We firmly believe that our ability to supply cell therapy developers and manufacturers with these critical biomaterials will lead them to remain with us through discovery, early stage development and the manufacturing support processes. We continue to view the cell and gene therapy space as a high-growth market, in which we need to continue to strengthen our capabilities in order to meet clients’ increasing needs and further enhance our growth profile.”

Charles River Laboratories looks like a very exciting company. It plays a key role supplying the tools that help biotechs and biopharmas do their research. In 2018 the group worked on 85pc of all FDA approved drugs. Its work sits at the heart of the drug development process.

The business is also highly acquisitive and has supplemented growth in recent years with a string of earnings enhancing acquisitions.

It has just announced the acquisition of Distributed Bio, a next generation antibody discovery company. The consideration was $83m in cash to bring in revenues of $21m with a further $21m contingent on future performance.

Prior to the Distributed Bio deal the group had spent over $2.0bn on acquisitions over the last five years and achieved a 10pc return on its investments.It is strongly placed in China which is rapidly emerging (see Zai Lab story) as a key player in drug development with every prospect that some major Chinese biopharmas are going to emerge in coming years.

Last but not least the business, like so many others, is being transformed by technology. In December the group “announced that it is the first company to offer clients Good Laboratory Practices (GLP) validated digital peer review using Deciphex Patholytix Preclinical for toxicologic pathology.”

It all looks very promising in a world where the number of biotechs engaged in clinical research has more than doubled from 2,000 in the early years of the new millennium to 4,300 now, with drug approvals annually, doubling and funds raised by the industry increasing from $25bn average a year in the 2000s to $40bn in the first half of 2020.The group is also changing.

Revenues derived from what it coyly calls its Research Models or RSM business is now down to 23pc of revenue and 24pc of profits, while its discovery assessment business is 58pc of revenue and 50pc of profits.

The balance comes from manufacturing support including microbial solutions and biologics, 19pc of revenue and 26pc of profits. However the RSM business is still important. The group has over 35pc of the Chinese RSM market and hopes to grow that to 50pc. So what is RSM? The ‘models’ are animals bred for testing, mostly small animals like mice and rats but I think also dogs and monkeys.

I don’t take a moral or ethical stance in my publications and I suppose somebody has to do it but I can easily imagine many subscribers will struggle with this. I do myself but I can see that the company is doing an important job and playing a key role in a booming industry, which saves many human lives. The shares are likely to continue to climb strongly.

“At Charles River, we have never been so essential to our diverse and growing client base, and we remain fully operational and continue to enable our biopharmaceutical clients to move their programs forward across a wide range of therapeutic areas, including COVID-19. Our resilience through the pandemic has served to enhance our position as the partner of choice for our clients’ early stage research needs as we continue to differentiate ourselves through our broad portfolio, our scientific expertise and our superb client service. In the second quarter, we were encouraged as most of our research model clients were returning to their facilities and recommencing their scientific research more quickly than anticipated. This favourable trend continued in the third quarter with a V-shaped RMS recovery as clients across North America, Europe and Asia, resumed more normalized research activities.” 30 October 2020.

Annual Income Statement Data

Meituan 3690

US$

MV: HK$1861bn ($240bn)

Next figures: 15 March

Buy @ HK$302

Chinese on-line food delivery giant rated one of world’s most innovative businesses

Meituan, formerly Meituan-Dianping, is a Chinese shopping platform for entertainment, dining, delivery, travel and other services. The company is headquartered in Beijing and was founded in 2010 by Wang Xing. By May 2014, the company had 5,000 employees. In 2015, Meituan merged with Dazhong Dianping and changed its name to “Meituan-Dianping”. Dianping.com hosts consumer reviews of restaurants and also offers group buying. Meituan-Dianping is one of the world’s largest online and on-demand delivery platforms. It had over 290m monthly active users and 600m registered users as of April 2018.

“On the consumer front, owing to our early, forceful expansion into lower- tier cities, we currently enjoy a significant first-mover advantage and stand to benefit from the ongoing trend that demand in lower-tier cities continues to grow alongside the rising levels of consumption. Our food delivery business in lower-tier cities made a larger contribution and exhibited higher growth in terms of GTV in full year 2019 as well as the fourth quarter of 2019. Moreover, lower-tier cities continued to be the main driver of our user growth in 2019. Attributable to our improvements to operational teams, delivery network and marketing capabilities as well as positive word-of-mouth, we continued to acquire new users, the majority of which came from third-tier cities and below.”

Annual report 2019

Initially started as the equivalent of ‘Groupon’ in China, Meituan has gone through a long journey to where it stands in the startup ecosystem in China. It is a pioneer, an early-adopter and now a leader in the O2O [online to offline] local life service industry with a Super App model that encompasses almost every aspect of Chinese life, ranging from on-demand food (and non- food) delivery, movie ticketing, ride hailing to hotel and travel booking.

The group was founded by 41 year old Wang Xing, who has built what is now considered as the leading on-demand services platform, with a huge fleet of bikes that will deliver anything anywhere anytime in China. A key decision by the group was to shift from using freelancers to setting up its own bike delivery network to dramatically increase efficiency.

Wang Xing is one of these dynamic individuals, who left university without completing his doctorate and had already built and sold two Internet businesses before launching Meituan, which was originally modelled on Groupon.

A key feature of Meituan is the pace of innovation. The group is continually reinventing itself and the way it does things and has been described as “the world’s most innovative company”.

The management of Meituan view their business as a three-segment entity by the nature of operation and business model, which are (1) on-demand food delivery, (2) in-store dining and purchase, hotel and travel booking, and (3) new initiatives and other, including the bike-sharing service that they recently bought from Mobike. The pandemic boosted demand for delivery but had a severely negative impact on the highly profitable dining, hotel and travel- booking business.

As of Q2 2018, Meituan became the leading food delivery platform and earned much more market share than the old player Eleme. In addition, it also started on-demand delivery for non-food products such as medicine, flowers, fruit, among many other categories.

At the core of Meituan’s evolution, building up a high frequency use case scenario (food delivery) enables Meituan to achieve low user acquisition cost, improves user stickiness, and increases the user lifetime value. Additionally, it creates room for cross selling products. For example, in 2017, over 80pc of hotel-booking service and 74pc of other lifestyle services were converted from food delivery and in-store dining consumer categories.

Equally importantly, data is an integral part of every aspect of Meituan’s business. From on- demand delivery route planning to merchant marketing, data analytics and tailored user experience have made it possible for Meituan to gain a high retention rate, to maximize the value of repeat consumers, extend the user lifecycle, and to become the household brand for local lifestyle services.

The key points about Meituan as an investment are the scale of the achievement in just 10 years, the power of innovation, the journey the group is making and the stupendous spending power of the Chinese consumer market. This is an incredible market in which to have such a strong first mover advantage and such a powerful platform.

“Year by year, piece by piece, step by step, Meituan realized that, with the strong consumer base, a lot more services can benefit from the scale of its network that enables not only low cost of user acquisition but also the multiplier effect – this is particularly true for those even unconnected and infrequent services and use case scenarios. All putting together, the concept and prototype of a Super App for local life services reveals itself so clearly. Meituan is positioning itself as the ‘e-commerce platform for services’ (analogous to Alibaba: e-commerce for goods), and is taking forward the ‘food plus platform ’strategy to really nail the ‘Super App’.game.” Analyst, 30 June 2020.

“As China’s economic recovery accelerated during the third quarter of 2020 as a result of effective COVID-19 containment, our businesses continued to recover steadily and achieved positive growth across all segments. Total revenues for the third quarter of 2020 increased by 28.8pc on a year-over-year basis and by 43.2pc on a quarter-over-quarter basis to RMB35.4bn. Operating profit increased from RMB1.4bn for the third quarter of 2019 to RMB6.7bn for this quarter, including RMB5.8bn in fair value gain on investment in listed entities.”

Annual Income Statement Data

Lemonade /LMND

US$

MV: $9.1bn

Employees: 459

Next figures: 25 February

Buy @ $167

Israeli-founded, US-based Lemonade aims to disrupt a global insurance industry that nobody likes

Lemonade is an insurance company that offers renters, homeowners and pet health policies in the US, contents and liability policies in Germany, the Nertherlands and France. Lemonade delivers insurance policies and handles claims through desktop and mobile apps using chatbots. Its business model includes giving underwriting profits to nonprofits of the customers’ choice. This is done annually in an event Lemonade calls “Giveback”. Lemonade was founded by Daniel Schreiber (former president of Powermat), Shai Wininger (co-founder of Fiverr) and Ty Sagalow. Lemonade underwrites its own policies and is reinsured at Lloyds of London. In 2020, financial analysis firm Demotech rated Lemonade’s financial stability as A-Exceptional.

“This significant upsell and cross-sell phenomena continues to gain steam within our homeowners’ business. About 12pc of our condo policyholders in Q3 started as renters at Lemonade and then graduated to become homeowners with Lemonade. While our overall IFP [in-force premiums] doubled year on year in Q3, our IFP from customers graduating from renting to owning grew by over 300pc. The premiums of these graduates grew sixfold on average, from $150 before their graduation to $900 after with no incremental cost to acquire the incremental premium. We believe these trends both within homeowners and between product lines have a tremendous runway.”

Dan Schreiber, CEO, 11 November 2020

Why is a company that aims to disrupt the global insurance market called Lemonade? I don’t know. Apparently it is something to do with lemons being sour and lemonade being sweet. The idea may be that most people regard insurance as a necessary evil provided by people with whom they have an adversarial relationship. Lemonade aims to change all that and give policyholders a ‘delightful’ experience.

It is getting great reviews, regularly boasts a net promoter score over 70 (anything positive is good, over 70 is sensational) and according to some observers is already the world’s most popular insurer.

If this all sounds a bit too good to be true that may be because you have not listened to the founders, Dan Schreiber and Shai Wininger, both from non-insurance backgrounds, describing how they are using technology to transform the customer experience and disrupt what they say is a huge but very traditional industry. I have listened to them and read the documentation including the prospectus and I have to say I am impressed. think Lemonade could be a very exciting business indeed with a huge growth opportunity. They have recently added pet insurance to their home insurance business and the new addition is off to a rip roaring start.

To give you an idea about Lemonade a third of claims are settled instantly; that’s right, instantly! How can they do this and make money? Various reasons. First they have very low costs because they use chatbots (robots) to sign up customers, settle claims and run their back office. Second, the first time policy holders are mostly small, Gen-Z and millennial renters so initially there is not a great deal at risk. Thirdly, they take a fixed 25 pc of premiums paid as the group’s income. Losses that bite into that, i.e., over 75pc, are mostly covered by reinsurance. If losses are less than 75pc they don’t keep more than 25pc but give the balance to charities chosen by the policyholders.

This means that if people try to cheat and embellish their claims it is not Lemonade who is being defrauded but the charities, which encourages good behaviour. They are also quite strict in who they sign up but best of all is that as those early bird customers grow older on life’s journey and become home owners their policies rocket five or six fold with no additional marketing cost to Lemonade.

No wonder they have plans to go into life insurance, which is a huge market. They plan eventually to go into all forms of insurance and expand all around the world. Last but not least the data they are collecting is unique in the industry and giving them a huge competitive advantage.

Lemonade is positively fizzing with excitement and potential. It is also very highly valued but could still be very cheap on a long-term view.

“The second thing of note this quarter was our launch of pet health insurance. It’s our first foray into an insurance sector beyond homeowners and it’s off to a roaring start. About 40pc of pet policies were sold to first- time Lemonade customers. These newcomers alone delivered about nine times more IFP than we generated from newcomers to Lemonade in the three months following our initial launch four years ago. And we did that at a rate of marketing efficiency that it took us three years to achieve with our renters’ products. Not only has pet insurance provided an additional on- ramp to Lemonade, but about 5pc of these newcomers added a rental or homeowner’s policy within their first quarter with us. And as compelling as the metrics look for newcomers, they are better yet for existing customers, who comprise a majority of our pet insurance buyers. Each of these added an average of $450 to their premium, an almost fourfold jump in the median premiums, without us incurring any costs at all to acquire incremental premiums.” Q3, 11 November 2020

“The fires in Q3 alone made this year California’s most disruptive fire season ever. Hurricane season was equally ferocious. The National Hurricane Centre named storms alphabetically, starting with A, but by mid-September they had literally run out of letters and they had to start over this time with the Greek alphabet. That has never happened so early. These unprecedented disasters hit the most popular states in the union, which are also home to the majority of Lemonade’s customers.Against this devastating backdrop our loss ratio for Q3 remained perfectly healthy. In fact, at 72pc, it was more than 7pc lower than the corresponding quarter last year. Below 75pc loss ratio are reinsurers make money. Our 25pc take is safe even without reliance on reinsurance, and there’s typically enough money left for giveback. If the annual gross loss ratio occasionally topped 75pc, that would also be OK, and our economics would be largely unchanged because our reinsurers would finance most of those excess losses. But the fact that our loss ratio didn’t spike even as catastrophes did is a non-event of note.” Q3, 11 November 2020

Annual Income Statement Data

Keyence Corporation /6861

¥

MV: Yen14,253bn ($137bn)

Employees: 8,419

Next figures: 29 January

Buy @ Yen58,520

Keyence offers opportunity to invest in a world class Japanese technology business

Keyence is a Japanese company, which has steadily grown since 1974 to become an innovative leader in the development and manufacturing of industrial automation and inspection equipment worldwide. Products consist of code readers, laser markers, machine vision systems, measuring systems, microscopes, sensors, and static eliminators.The group serves over 250,000 customers in 110 countries around the world, Keyence is fabless (fabrication-less) – although it is a manufacturer; it specialises solely in product planning and development and does not manufacture the final products.

“Ketence and its affiliated companies have more than 1,500 highly trained sales engineers positioned around the world. Keyence’s philosophy is to meet customers’ needs at every level of their business from the design and research stage to the production line and beyond. Highly trained technical sales engineers are expert problem solvers who can provide real solutions to the customers’ applications with existing products or potential new solutions.”

It is very hard to research Japanese automation business, Keyence Corp. I cannot even find a discussion of their latest results but this is what the Financial Times said about the company in February 2019

“Keyence Corporation, a $68bn manufacturer of factory automation widgets, might just be the greatest business in the world. Over the past two decades, Japan’s sixth largest listed company has sustained operating margins north of 40pc and, post-crisis, revenue growth of 10 pc plus, propelling its shares from ¥4,477.5 to ¥31,250 as of Monday’s market close [and now to over Y58,000 around two years later].

Keyence specialises in creating a range of products for factory automation, such as measurement sensors and laser markers. Just under half of its revenues come from Japan, with the US its next largest region for sales. But the company is also a mystery. Keyence’s financial disclosures are threadbare — its annual report last year ran to only 22 pages — and its chosen to sit, Smaug-like, on its $12.5bn cash pile, rather than redistribute it to shareholders. It also does not talk to the press. Yet, as we noted in November, the most puzzling aspect of Keyence’s business is how it has kept its evident competitive advantage for so long. One theory put to Alphaville is that its unique sales culture, which blends sales and market research, allows it to serve customers far more efficiently than rivals. Another reason, as argued by CLSA Japan’s Head of Research, Morten Paulsen, is that its delicate management of its supplier relationships allow it to keep manufacturing costs extremely low.”

New product highlights in their latest annual report featured a wide area coordinate measuring machine, a data analytics platform, a programmable controller and a handheld mobile computer. The data analytics controller, “The KI Series software from Keyence allows users of any skill level to easily analyse large amounts of data. Even without a data scientist with specialized knowledge, analysing enormous amounts of data is possible using AI and machine learning for automatic uncovering of solutions for various business problems. The KI Series can be utilized in any business situation, regardless of industry or field, for swift and accurate decision-making support.”

It sounds very useful. However it is also suggested that it is not so much what they do but how they do it, like Apple, using contract manufacturers to make everything, which keeps cost low, which, allied to their direct sales relationships with customers across the globe keeps sales growing and profit margins super high.

At the end of the day this business just feels special and I expect it to continue to be a rewarding investment as it has been since the shares took off in 2012.

“The market environment surrounding Keyence Group businesses is expected to see not only growing demand for automation, quality improvement, and R&D investment, but also various technological innovations. We recognize the need to strengthen the group’s planning and development capabilities while also expanding overseas business operations. In addition, furthering human resource development to take advantage of these changes and demands for continued sustainable growth is critical. We view these global trends as having great potential for expanding our business, and to realize this potential, we will focus on applying the powers that we have cultivated over the years to achieve sustained growth.” Annual report, June 2020

“Keyence is an industrial company specializing in factory automation sensors, a developer as well as marketer. Factory automation is where Japan has been a global leader and likely will continue to be. What Keyence produces are customised factory automation sensors for customers to use in their factories.

Japan is a country that has been experiencing an ageing labor population and a rising labor cost since as early as the 1960s. That is why we have this industry that is leading the world in robotics and factory automation.

One of the great things about this company is they have a direct sales channel that caters to factories and corporate industrial customers. This is a hard-to-replicate business model, because factories don’t normally want any outsiders walking around their premises. This direct sales channel strategy is very difficult to replicate and because of this they have extremely high margins with historical operating margins of more than 50pc. They are very, very global and very cash-flow generative with a strong track record and strong balance sheet. In a nutshell, we believe it is a great business.” Japanese fund manager discussing Keyence as an example of stable Japanese companies with long-term growth potential.

Annual Income Statement Data

Natera /NTRA

US$

MV: $9.49bn

Employees: 1,039

Next figures: 9 March

Buy @ $111

Blow-out Q3 for Natera with exciting potential in tests for pre- natal, transplants and oncology

Natera (previously Gene Security Network) is a genetic testing company that operates a CLIA-certified laboratory in San Carlos, California. The company specialises in analysing microscopic quantities of DNA for reproductive health indications to provide preconception and prenatal genetic testing services to physicians and in vitro fertilisation centres. The company has been broadening its reach and now describes itself as a leader in non-invasive genetic testing and the analysis of circulating cell-free DNA’.

“In Q3, we processed 262,000 tests, which represents 31pc growth versus last year and 12pc versus the second quarter of this year. This is a record quarter in several respects. For example, this is the best sequential quarterly growth we’ve seen in Q3 since 2015, when the business was a small fraction of the size we are today. We generated revenues of $98.1m, which is again a record and is up 13pc from Q2 2020 and 26pc from Q3 2019. This revenue growth was largely driven by product revenues, which were up 39pc year-on-year.”

Steve Chapman, CEO, Q3 results, 5 November 2020

Genetic-testing group, Natera, delivered Q3 2020 results showing progress in all divisions of the business.

“Based on the success we have had in Q3, we’re excited today to significantly raise our 2020 revenue guidance. The bulk of this performance comes from the core reproductive health business hitting on all cylinders. Post-ACOG [The American College of Obstetricians and Gynecologists], we are seeing an uptick in accounts ordering average-risk NIPT [non- invasive pre-natal testing] and we have continued to benefit from closing new customers as well. we’ve had in organ health and oncology has now started to contribute to revenues. Also, as you would expect, when the clinic starts ordering Panorama from us, we have an opportunity to educate the practice on our carrier screening offering, which serves to amplify the effect of these trends in our business.

This is the time we’ve really been working for over the past five years, where the success that We’re not breaking out the new businesses for competitive reasons but it’s exciting to see some of the green shoots in these very large markets.

The U.S. market for NIPT consists of about 4m to 5m pregnancies per year and is very under- penetrated in the average-risk setting, which makes up 80pc of those pregnancies. So we still have significant room to run in the NIPT space. The acceleration we’ve seen in 2020 is really incredible, and it’s picked up even more since. This is the same pathway to reimbursement that we started presenting when we first received the draft local coverage decision last year in colorectal cancer. As a reminder, there are roughly 145,000 patients in the U.S. diagnosed every year with colorectal cancer, and about two-thirds of them have Stage 2 or Stage 3 disease. So with the repeat testing described in the Medicare coverage policy, this would imply roughly 1m tests per year as a total addressable market.

We are now moving into the formal commercial launch phase for Signatera in the clinical setting for colorectal cancer, and we plan to build on the momentum we’ve seen in the pre- launch phase. Pharma demand has been growing rapidly for us. We continue to win business from new customers, and our repeat business from our largest pharma clients is continuing to grow, consistent with trends we described in August.

We were very pleased to execute a follow-on equity offering in the quarter, where we took net proceeds of roughly $271m and now have a total cash and investment position of over $800m. This cash position, along with our expectation that the women’s health business crosses over the cash flow breakeven threshold next year, means that we are very well situated to make the investments necessary to support the new products. Overall, we are very pleased with all the momentum in the business.”

As you can see I have really let the company tell the story here because the business is new to me and operating in unfamiliar areas. What stands out is that the company is growing strongly, beating expectations, on the brink of becoming cash flow positive, strongly funded and very likely at the beginning of what could be years of strong growth. The company is already talking about a total addressable market (TAM) of $18bn.

“We have already seen a significant amount of momentum among payers adding average-risk NIPT to their coverage policies, and we could see significant additions to that list in the near term. This development aligns nicely with the timing of the completion of the SMART trial. The SMART trial is a prospective 20,000-patient multisite clinical trial with newborn genetic outcomes that has taken five years to run. We think a study of this magnitude and scale will never be repeated, and therefore, could become the gold standard in NIPT for the foreseeable future. The data has been unblinded to us and to the investigators in the trial. And we believe the results have the potential to further drive market share in NIPT and may unlock guidelines on reimbursement for microdeletions, which is already more than 100,000 units per quarter for Natera. We expect the data to be presented at the SMFM [The Society for Maternal-Fetal Medicine] conference early next year.” Steve Chapman, CEO, Q3 results, 5 November 2020

Annual Income Statement Data

Zai Lab Limited

US$

MV: $12.8bn

Employees: 859

Next figures: 5 March

Buy @ $145

Zai Lab sets three year goal to become leading global biopharma

Zai Lab is a commercial-stage biopharmaceutical company focused on bringing transformative medicines for cancer, infectious and autoimmune diseases to patients in China and around the world. Zai Lab’s experienced team has secured partnerships with leading global biopharma companies, generating a broad pipeline of innovative drug candidates. Zai Lab has also built an in-house team with strong drug discovery and translational research capabilities, aiming to establish a global pipeline of proprietary drug candidates against targets in our focus areas. Zai Lab’s vision is to become a fully integrated biopharmaceutical company, discovering, developing, manufacturing and commercialising its portfolio in order to impact human health worldwide.

“Over the next three years, we plan to have a steady stream of approvals and commercial launches in Greater China, across multiple therapeutic areas. We established transformative partnerships and advanced our internally discovered global pipeline into the pivotal stage. Today, our portfolio consists of four US FDA approved assets with two approvals launched in China, 14 clinical stage assets, with nine in late stage development, two internal programs with global rights in the clinic, and over 25 clinical trials planned or ongoing across oncology, infectious and autoimmune diseases.”

Not the least amazing thing about Zai Labs is that it didn’t exist before 2013. It has been built from scratch with the intention of creating a leading biopharma able to cater for China’s vast and ever more affluent population but also to compete on the world stage.

The shares were floated at $23 in September 2017 to value the group at $1.15bn. At the time it had raised around $320m in funding including the IPO money and had just 155 employees. Seven years later and the business is valued at over $12bn, it has 892 employees and although we are not even halfway through January it has already announced two major new partnerships including one with Argenx SE, a company which is already in the Quentinvest portfolio.

There are a number of reasons why the group has been able to move so fast. China is explicitly opening up the country to new drugs, encouraging innovation and trying to foster the emergence of powerful Chinese biopharma businesses. It is doing this almost from a standing start. Secondly, western countries need to partner with Chinese companies to make use of their expertise, connections and manufacturing capabilities to negotiate the Chinese regulatory environment and engage with Chinese consumers and its medical community.

Thirdly and arguably most important is the capability and experience of Zai Lab’s top team led by founder and CEO, Samantha Du. She played a key role in setting up Hutchison China Meditech, a biopharmaceutical company backed by CK Hutchison, a powerful Hong Kong based company with roots in the old Hongs. She left Hutchison Meditech to set up Zai Lab Limited, which has already outstripped the former business.

The opportunity to act as a gateway between western businesses and the Chinese market looks enormous and the company says western pharmas are queueing up to do deals on their products. This makes sense because Zai can help with market access, with local manufacturing and also with its increasingly powerful r&d capabilities to help, for example, to find new indications for existing drugs and also negotiate the expensive clinical trials process.

I haven’t attempted to go into detail about the drugs in Zai’s partnerships or in its own pipeline. There are so many and the number is growing all the time. What makes this company exciting is the scale of its ambitions, the speed at which it is moving, the talent and experience of the leadership team, its key position as a gateway into China, which is effectively being sponsored by the Chinese government and its demonstrated ability to raise money.

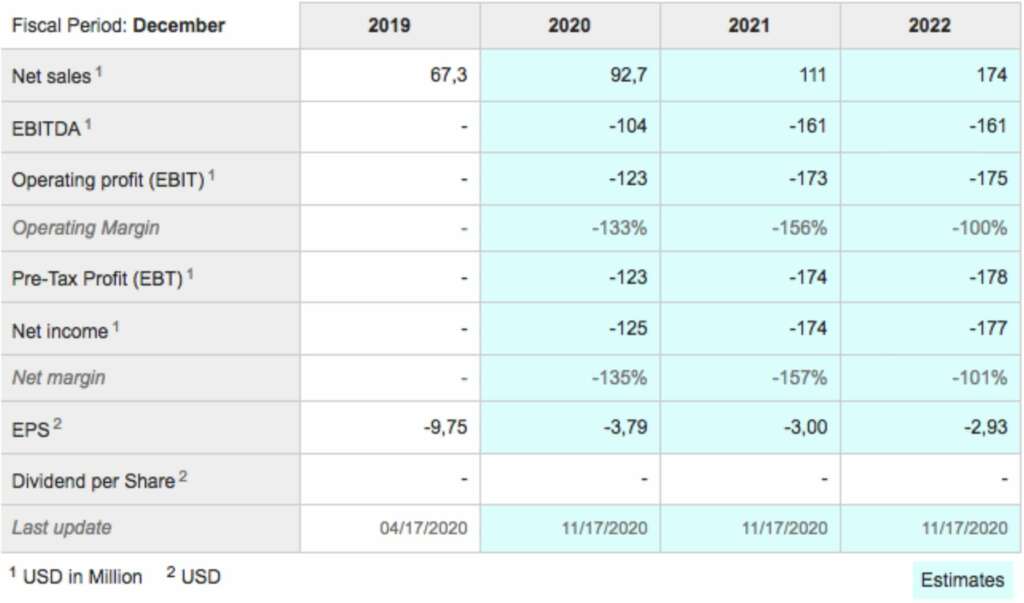

In 2017 the group had no sales and costs of $150m plus so fund raising capability has been critical. Since foundation the group has raised around $1bn.It may not need tor raise too much more because its partnerships are starting to bear fruit, with sales expected to ramp up rapidly to a projected $461m by 2022.

Even more exciting for Zai is the opportunity to develop its own proprietary drugs, which is the main reason why it is building such an impressive r&d capability.

“Zai Lab was built on the vision that, despite having a significant addressable market and sizable growth potential, China has historically lacked access to many innovative therapies available in other parts of the world and its drug development infrastructure has been under- utilized. There remains the need to bring new and transformative therapies to China. In recent years, the Chinese government has focused on promoting local innovation through streamlining regulatory processes, improving drug quality standards and fostering a favorable environment, which we believe creates an attractive opportunity for the growth of China- based, innovation-focused companies.”

“We’re proud of our global reputation as a biotech pioneer and the partner of choice in China, and remain very confident in our team, strategy, and platform, and continue to deliver exceptional execution and growth. This is why I believe that within next three years, Zai can reach our vision of becoming a leading global biopharma Company.”

“I’ll start with Niraparib or ZEJULA, a PARP- inhibitor approved globally for the treatment of ovarian cancer, and in development for several other solid tumor indications. We believe ZEJULA is a potential best-in-class PARP- inhibitor, given it is the only PARP-inhibitor approved in the United States as monotherapy for all-comer patients in the first-line and recurrent maintenance treatment settings. In addition, it has superior pharmacological properties including, once daily dosing, low drug-drug interactions and ability to cross the blood-brain barrier.

As you know, ZEJULA was launched in China in January for second-line maintenance treatment of ovarian cancer patients, with over 800 hospitals covered at the time of launch. This commercial launch was done with incredible speed, with launch events held both onsite and online. Since the launch, ZEJULA has been included for regional reimbursement in one province and six cities. It has also been listed in 16 commercial health insurances and four provincial and municipal level customized commercial insurance, underscoring Zai Lab’s execution capability in bringing important therapies to patients.

Trial results further underscore the promise of ZEJULA as a best-in-class ovarian cancer treatment. Looking ahead, our plan is to continue to develop ZEJULA and to bring this innovative medicine to as many patients who may benefit as possible, including in tumors beyond ovarian cancer.” Tao Fu, president and chief operating officer, 13 August 2020

“Let me first say that at Zai we have really built a strong reputation over the last few years as a partner of choice for Western companies when it comes to this part of the world. And we also have a very robust business development pipeline currently in the backlog. And most of these are actually, by the way inbound interests from good, reputable US companies and a lot of them are the strategic objective for them to do a deal, is relooking for help, not only to access the Chinese market quickly, but also to help and accelerate the global development. I think we have had a very good first half and we have done two great strategic deals, one with Regeneron, one with Turning Point, both late stage assets, both arguably potentially best-in- class products in the categories. And we’re working very hard to expedite those timelines in China and also working with them from a global development perspective. We won’t commit to a number in the second half of this year, but we’re working very hard, and I think I’m sure we’ll bring a lot more good deals in the very near future.” Jonathan Wang, head of business development, 13 August 2020

Annual Income Statement Data