I will have more to say about Carvana and its extremely bullish chart below but first I want to talk about another exciting share.

Table of Contents

I have just found this amazing analysis of Root which was written in June 2023, when the shares traded as low as $4.61 to value the business at $67m. This price reflected investors’ conviction that three years of heavy losses meant that the company was heading rapidly toward an inevitable bankruptcy.

Unsuccessful Bid Marks Turning Point for Root

Against this background a company called Embedded Insurance, headed by James Hall, a Ph.D from Oxford, made a $19.34 cash bid for the company. You might imagine that delighted Root shareholders would have rushed to accept but they were not able to do so because of the voting structure which gave insider shareholders and management voting control and they vehemently rejected the bid.

The bid didn’t succeed and after a brief spike higher the shares fell back again but with hindsight we can see that the bid marked the turning point for the shares.

Below is an expert assessment written at the time of why the shares were right to turn higher and most likely the insiders were right to reject the bid. Given how tiny Root was at this time in market cap terms it is extraordinary that anyone could be bothered to write about the company at all.

Root is a technology company that is trying to disrupt the slow and stodgy insurance industry. The company sells short tail products (automobile insurance, renters insurance, and homeowners insurance). The automobile insurance industry is large, with approximately $273bn of annual premium dollars. The company has aggressively invested in its technology stack, which enables consumers with the ability to shop, get a quote, and ultimately purchase insurance, via their smartphones.

The company operates an embedded insurance model, and Carvana (CVNA) is the company’s first partner. Embedded insurance is arguably the future of insurance and Root is (arguably) way out in front here.

Enclosed below is one technical definition of embedded insurance:

Embedded insurance is a type of bundling and sale of insurance coverage or protection while a consumer is purchasing a product or service, bringing the coverage directly to the consumer at the point of sale.

(Source: Cover Genius)

To picture it, think of buying insurance on your new iPhone or Samsung Galaxy smartphone at the time of purchase, at the Verizon Wireless, AT&T Wireless, or T-Mobile store. Or think of buying insurance at the time of purchase, at Home Depot (HD) on a basket of home appliances. Additionally, if you buy expensive electronics at Best Buy (BBY), you might consider buying insurance. These are all real-world examples of embedded insurance.

Besides the significant investment on the technology side of the business, the company’s underwriting practices are different in that they want to evaluate insurance risk, at the individual level, as opposed to pricing it on an aggregate basis, using the ‘law of large numbers’. In other words, the traditional model was that the large players would figure out expected aggregate losses, on a large pool of customers, and then price their coverage similarly, albeit with some modifications and tweaks based on various/broader risk factors, for each stratum of customers.

Moreover, Root uses technology and machine learning to assess risk and behavioral data, notably using proprietary telematics.

The Past Operating Losses And The Opportunity

At face value, a casual observer might quickly glance at ROOT’s historical losses and declaratively conclude ROOT will go out of business. ROOT’s stock chart is really ugly, and the stock is down 98pc from its all-time highs, accounting for its 1 for 18 reverse split (effective August 12, 2022).

Fidelity

The chart, on a one-year basis, notwithstanding the high volume move made on June 21st and 22nd, lifting ROOT shares from $6 to $14.80 (the stock actually traded as high as $15.70 in pre-market on June 22, 2023), is similarly ugly.

Fidelity

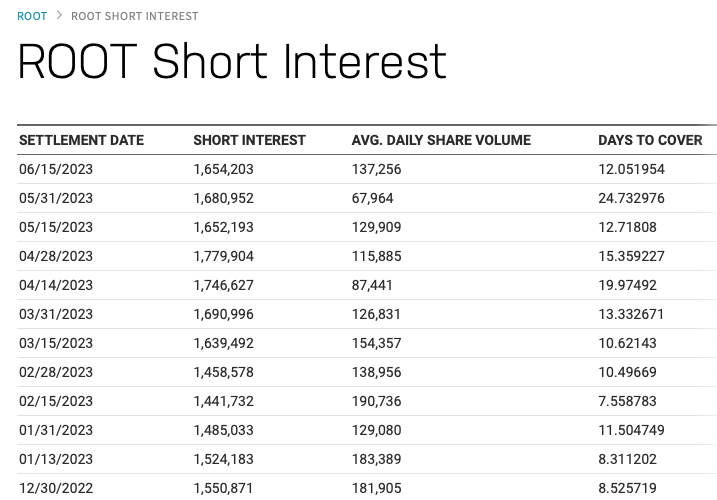

Perhaps, the shorts have been short this stock, for a long time and at a very high price, and certainly seems like they are intent on riding this stock to zero, or so they think.

Nasdaq.com

As I mentioned earlier, I’ve saved readers the trouble of digging through ROOT’s past conference calls and 10-Ks and present its unencumbered capital and hefty operating losses.

Net Cash Used In Operating Activities (Cash Flow Burn Rate)

FY 2022: -$210.6 million

FY 2021: -$403.4 million

FY 2020: -$287.2 million

As you see, the unencumbered capital base is relatively sizable and the speed of losses is slowing.

Trajectory Of Unencumbered Capital (Period Ending)

3/31/2023: $524 million

12/31/2022: $559 million

9/30/2022: $629 million

6/30/2022: $696 million

3/31/2022: $736 million (signed a $300 million term loan with BlackRock)

12/31/2021: $450 million

That said, investing even the higher risk variety, and make no mistake here, if you’re long ROOT, you’re swimming in the higher risk end of the pool, is about the future.

If you actually do some real work, a clever and forward thing observer might try and work out why James Hall wants to buy this business, for $19.34 per share, in cash, a seemingly astounding 220pc premium to its June 20, 2023 closing price.

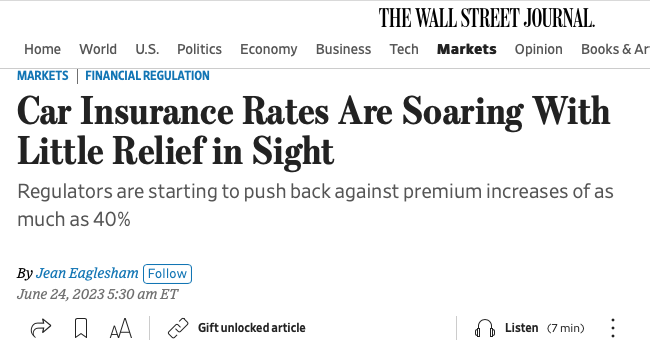

Big Rates Increases, Lower Loss Ratios, And Big SG&A/Marketing Cuts

1) Big Rate Increases on Tap

If you actually dig in, you learn that 2022 was the worst year, from a profitability standpoint, for the auto insurance industry, in thirty years!

WSJ

Check out these two poignant excerpts, from the June 24, 2023 WSJ article, referenced above.

Exhibit A:

Auto insurers say their rate requests are driven by necessity, not greed. The cost of claims has soared since the pandemic, due to more accidents, higher repair costs, bigger medical bills and increased litigation. Car insurers last year lost on average 12 cents for every dollar of premium written, according to S&P Global. State Farm, the country’s biggest car insurer by premium volume, lost 28 cents for every dollar written last year, posting a $13bn underwriting loss for its auto arm.

Exhibit B:

It’s probably the worst period for auto insurers it’s been in 30 years at least,” said Neil Alldredge, chief executive of industry body National Association of Mutual Insurance Companies.

As we already established, the auto insurance business is very large, with approximately $273bn in annual premium dollar written, as of 2022. Like or hate it, this industry plays an important role in the functioning of society. Therefore, in order for the industry to exist, it has to remain profitable over the full business life cycle. Because of the record losses, State Insurance Regulators have little choice and have to agree to rate increases, such that we, as in the society, have a functioning automobile insurance industry.

Specifically, if we take the work a step further, and you read ROOT’s February 23, 2023 Q4 FY 2022 earnings call transcript, we learn that ROOT already has, in motion, average rate increase of 37pc because of the broader industry’s big operating losses last year.

In 2022, we implemented 53 rate filings with an average increase of 37pc across our total book. We filed revised policyholder contracts in 33 markets to tighten underwriting and refine our fee schedules. We plan to increase rates again in 2023 where needed to offset loss trends from persistently higher than historical severity. The combination of rate increases strengthened underwriting and meaningful segmentation improvements continue to drive decreases in our loss ratios quarter-over-quarter, moving us closer to our long-term target of 65pc.

So if you think about it, albeit with a lag, as the rate increases have to take effect, this is a big tailwind for future profitability.

2) Gross Accident Loss Ratios Rapidly Improving

During that same Q4 FY 2023 conference call, and referenced directly above, we also learn ROOT’s longer-term targeted loss ratio is 65pc.

Lo and behold, during Q4 FY 2022 and Q1 FY 2023, we are seeing tangible evidence that loss ratio is materially declining.

Q4 FY 2022:

The gross accident period loss ratio was 77pc for the fourth quarter, a 17 point improvement versus the fourth quarter of 2021. We have recognized and responded to loss trends early, which has driven this year-over-year improvement.

Q1 FY 2023:

The gross accident period loss ratio was 69pc for the first quarter, a 13-point improvement versus the first quarter of 2022 as we recognized and responded to loss trends early. We remain committed to lowering the loss ratio and expenses to improve our financial performance and the fiscal foundation of the company.

3) Management has Taken a Lot of Costs Out of the Business Via SG&A Cuts and Marketing Cuts

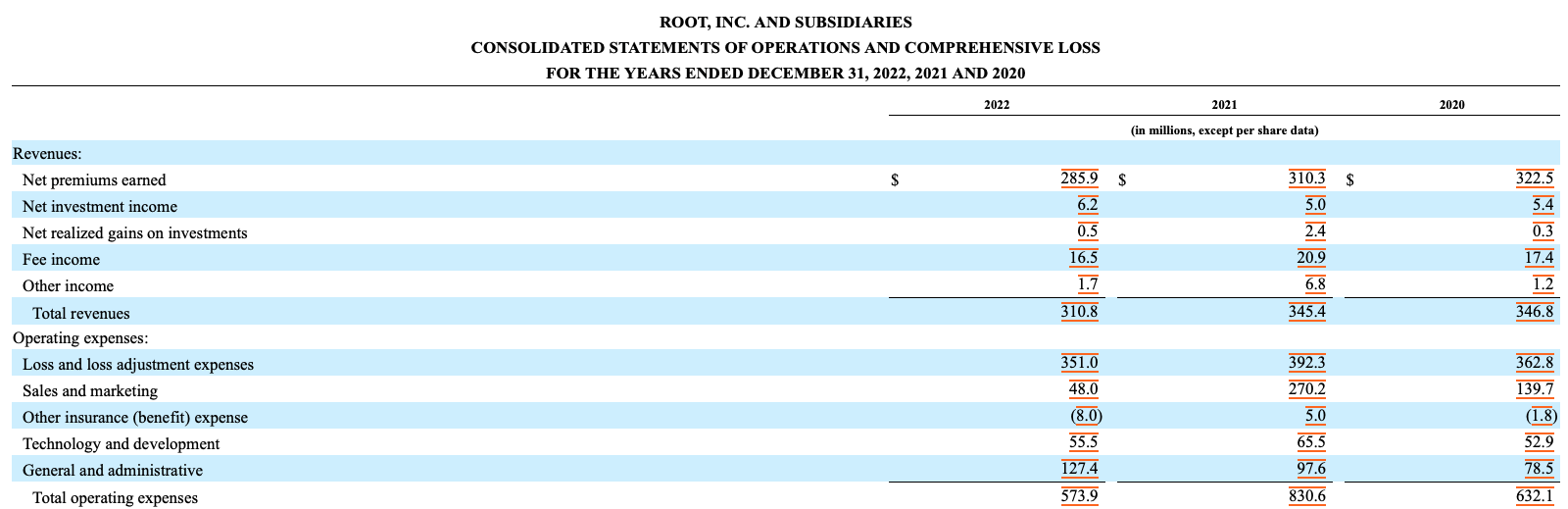

The easiest way to see this is to look at ROOT’s FY 2022 10-K and simply review trajectory and declining cost of SG&A and marketing.

ROOT’s FY 2022 10-K

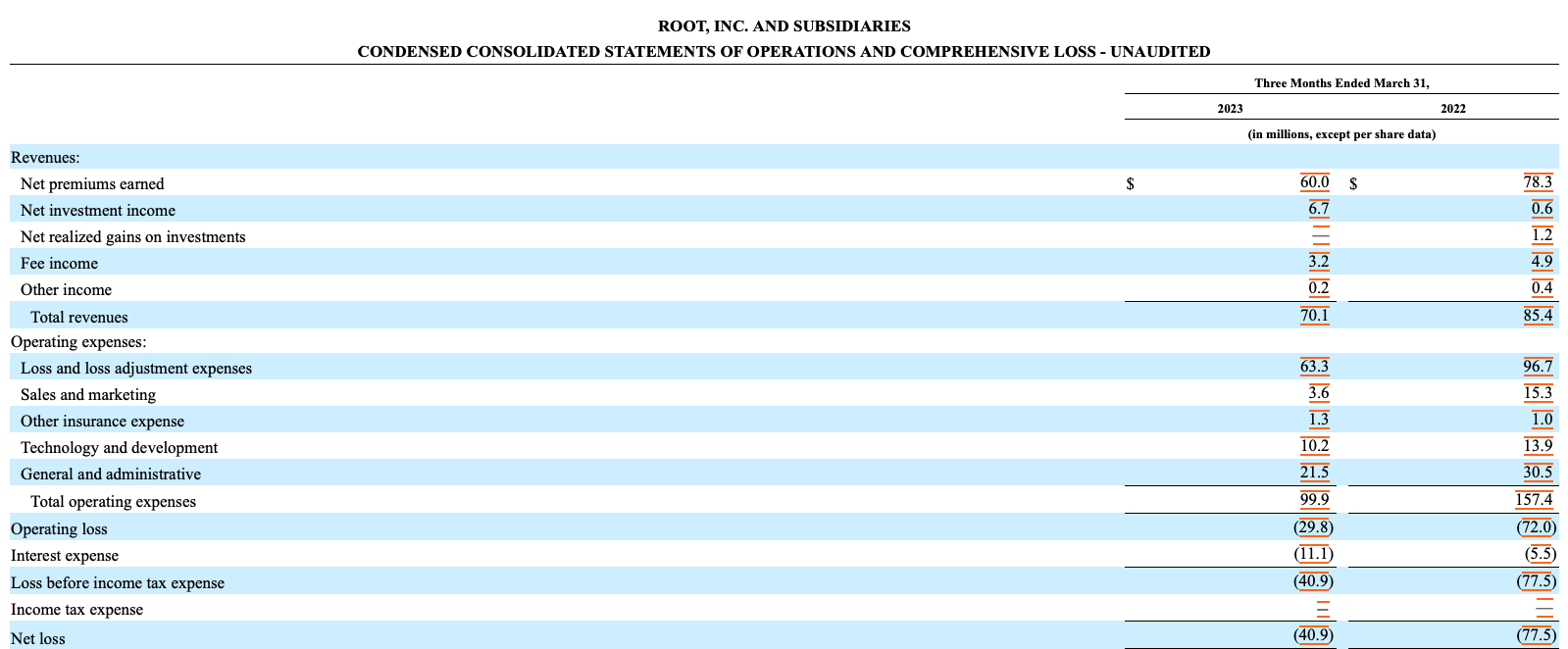

Q1 FY 2023 SG&A is down materially, as is its marketing spend.

SG&A has gone from $30.5m (Q1 FY 2022) to $21.5m (Q1 FY 2023) and Sales and Marketing has gone from $96.7m (Q1 FY 2022) to $63.3m (Q1 FY 2023)!

ROOT’s Q1 FY 2023 10-Q

More Green Shoots

If you take the time to understand ROOT’s business model, they are marching towards an embedded model.

See here:

Furthermore, we continue to prove our differentiation in the embedded channel and are excited to announce we finalised a third partnership.

I’d like to take this opportunity to discuss the key elements of our differentiation. Having built our company on a flexible technology stack, allowing customers to get a quote without ever touching a keyboard, we are able to create seamless, real-time, quote-to-bind experiences in the moments that are most relevant to consumers. This drives adoption rates, as shown by an over 3x increase in our attach rates since launching our fully-embedded product.

Second, our platform continues to advance through our API [application programming interface] developments, allowing us to rapidly scale and add new partnerships while materially reducing the cost and time to deployment for those partners. Putting these three things together, increasing adoption while decreasing costs and increasing speed to market, that’s the differentiated value we provide to our partners.

(Source: ROOT’s Q1 FY 2023 Conference Call)

And in terms of upcoming big catalysts, for both the business and the stock, ROOT already has two new embedded partners, and behind the scenes, they are working on near-term product launches.

Two New Embedded Partners:

We’re also equally, if not more excited, by the two new embedded partners that we have that we think will provide substantial new writings. Now we want to launch those in the coming months. It will take time to get those products into market, but we have all the faith in the world that those are two excellent partners that will provide significant scale for the business.

(Source: Root’s Q1 FY 2023 C.C. (May 4, 2023))

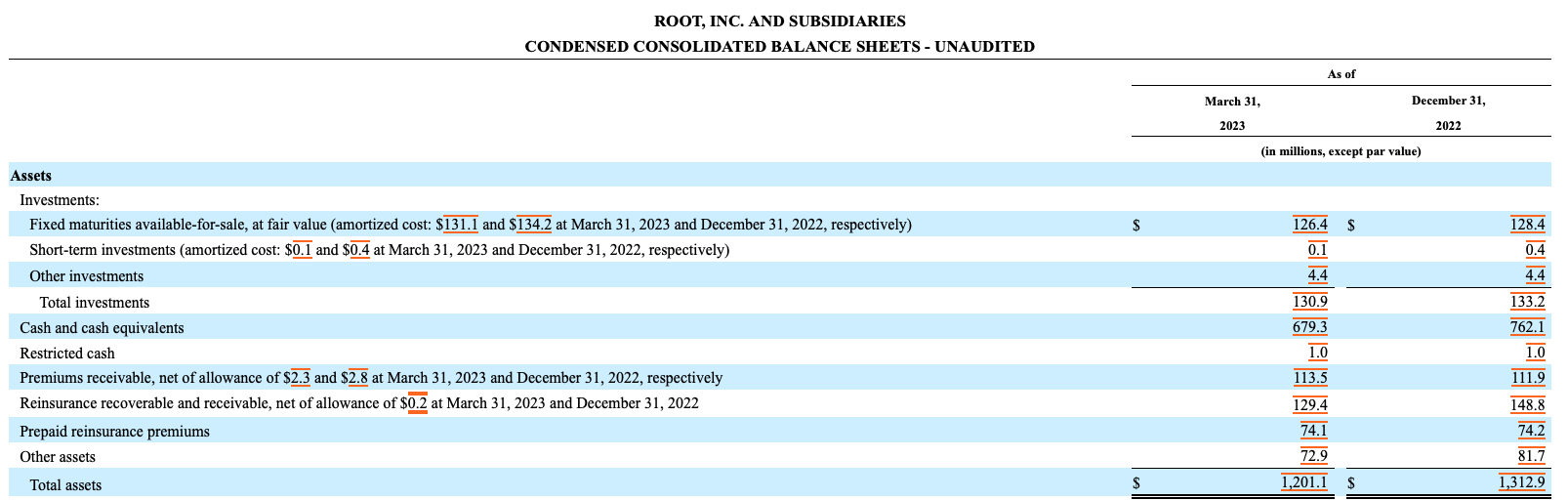

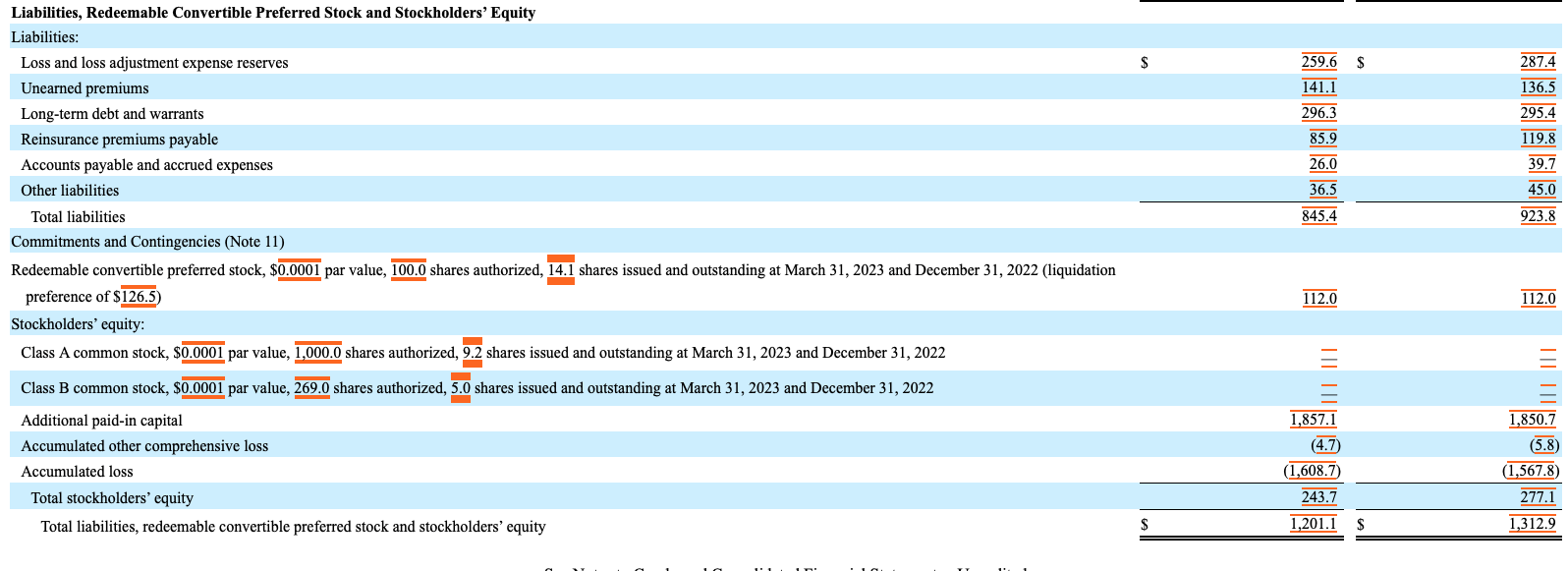

As of March 31, 2023, Root’s book value is still $17.04 per share.

ROOT has 9.3m Series A shares and 5 million Series B shares outstanding. $243.7m, ROOT’s March 31, 2023 total stockholders’ equity divided by 14.3 million shares gets you to $17.04 per share of book value.

ROOT’s Q1 FY 2023 10-QROOT’s Q1 FY 2023 10-Q

Other Nuances

It doesn’t take a rocket scientist to hypothesize that James thinks the future of insurance is finding and attracting customers in the embedded channels.

Secondly, I find it extraordinarily unlikely that James Hall’s bid wasn’t real and that he was spoofing the WSJ. I’m not saying the guy is a good person or not, I don’t know him, so I can’t make that judgment. What I do know, though, on balance, PhDs from places like Oxford tend to be credible and care about their reputations and, therefore, it is unlikely that the bid was some charade.

Perhaps, the reason he hasn’t yet taken a 5pc stake and arguably why we haven’t seen one activist SC 13D filers (or multiple 5pc holders) is because of ROOT’s dual voting class share structure, which consists of A and B shares.

Per ROOT’s FY 2022 10-K:

Our Class B common stock has ten votes per share and our Class A common stock has one vote per share. As of February 16, 2023, holders of our Class B common stock collectively beneficially own shares representing approximately 83.5pc of the voting power of our outstanding capital stock. Our directors and executive officers and their affiliates collectively beneficially own, in the aggregate, shares representing approximately 19.0pc of the voting power of our outstanding capital stock. As a result, the holders of our Class B common stock are able to exercise considerable influence over matters requiring stockholder approval, including the election of directors and approval of significant corporate transactions, such as a merger or other sale of our company or our assets, even if their stock holdings represent less than 50pc of the outstanding shares of our capital stock. This concentration of ownership limits the ability of other stockholders to influence corporate matters and may cause us to make strategic decisions that could involve risks to you or that may not be aligned with your interests. This control may adversely affect the market price of our Class A common stock.

One other nuance here that is worth mentioning, ROOT has an expensive $300m five-year term loan. In FY 2022, ROOT’s interest expense was $34.6m.

On January 26, 2022, we closed on a $300m five-year term loan, or Term Loan. The maturity of this Term Loan is January 27, 2027. Interest is payable quarterly and is determined on a floating interest rate calculated on the Secured Overnight Financing Rate, or SOFR, with a 1.0pc floor, plus 9pc, plus 0.26161pc per annum. Concurrently with the Term Loan, we also issued to the lender warrants to purchase approximately 0.3m shares of Class A common stock. Under certain contingent scenarios, the lender may also receive additional warrants to purchase shares of Class A common stock equal to 1.0pc of the aggregate number of issued and outstanding shares of our Class A common stock on a fully-diluted basis as of the triggering date.

(Source: ROOT’s FY 2022 10-K)

Putting It All Together

A first-level think might argue ROOT’s stock is destined for zero given the historical operating losses. Moreover, a pessimist might read the statement issued by Root’s Board of Directors and think James Hall didn’t actually bid. As I’ve argued, it is unlikely James Hall isn’t 100pc serious about wanting to buy this business.

Moreover, a second-level think might actually work out that Root, Inc.’s business is inflecting. Ongoing and upcoming 37pc average rate increases, much lower loss ratios, and lots of SG&A and marketing expense cuts mean the burning platform has been (greatly) extended. In addition, per Root’s conference calls, they already signed two new and national embedded partners. They have near-term plans of rolling out new products, with these new embedded partners, in the coming months.

This is a major catalyst.

Lastly, the tricky part and arguably why we don’t have 5pc holders (and activists waiting outside the gates) is due to the dual-class voting structure.

On balance, I really like the risk/reward and setup here, as there as multiple ways to win. That said, though, to be crystal clear, this is definitely a high-risk stock/high-reward stock. The biggest risks are the operating losses and ROOT’s ability to stem those operating losses and prove the business can scale and profitability inflect.

Courage & Conviction Investing, 6 July 2023

I think the above was a terrific and timely analysis of the risks and rewards of buying Root shares in mid-2023. I also think there are striking similarities between the chart of Root, a disruptive supplier of insurance to the auto industry, and Carvana, a company which is attempting to disrupt the way used cars are sold and which became Root’s first embedded partner.

I picked up quickly on Carvana’s potential at around $10 because I was already familiar with the company and knew that they had an exceptional management team. Root I came later to the story at $44 but I think both shares still have a long way to go, possibly a very long way.

I have seen this before with a UK company called Ashtead, which is mainly a US business through its Sunbelt Rentals subsidiary.

Ashtead is a plant rental business. At the start of the new millennium, Ashtead was loaded with debt to finance the plant and equipment in its depots and the acquisition of Sunbelt Rentals. It looked doomed as business confidence plummeted globally but it wasn’t and as so often happens with an ordeal by fire what doesn’t kill you makes you stronger.

Fast forward and we entered an era where there was a massive secular shift from owning to renting in the US and Ashtead, a superbly managed business did incredibly well, so well that the shares have risen from 1.8p to 5644p and have been higher.

There is a possibility that both Root and Carvana are on similar paths which is why I am so excited about both these shares. They are disruptors, they appear to have excellent management, they had their ordeal by fire in 2022 and both management teams, like that at Ashtead, have quickly pivoted towards managing their businesses much more tightly with many lessons learned.

Scope to Move Into Virtuous Circles of Growth

Trading performance for both Carvana and Root is on a dramatically improving trend.

2023 was an exceptional year for Carvana. It was our best year from a financial perspective by a long way. Full-year, GPU [gross profit per unit] was nearly $1,000 better than our previous best in 2021. Our full-year adjusted EBITDA per unit was over $900 higher than our previous best, and we have clear visibility to further improvements, as you can see in our outlook. The last two years have been initially characterised as negative for Carvana. In early 2022, we took a quick trip from a company that was perceived to be able to do little wrong to one that was perceived to be able to do little right. That wasn’t a fun transition for anyone. In each of our letters since we went public in 2017, we have signed off with the march continues.

Ernie Garcia, CEO and co-founder, Carvana, Q4 2023, 22 February 2024

Ernie Garcia is the man. Listen to this.

It’s very hard for a group to go through a period like the last two years and not to disintegrate under the pressure. We didn’t disintegrate. We thought, we came together and we got better. The fact that we got better creates room for the last two years to be recharacterised in the future. Time will ultimately pass judgment on the impact of the last two years on the Carvana story. But my personal take is that it’s been our proudest period and that when the story is written, this period and our team’s response will be viewed very favorably. To the Carvana team, there is nothing we can say in words that will convey the gratitude we have for the fight you’ve always put up, but I hope you know it’s real. Thank you. While the success of 2023 deserves a moment of reflection, the truth is we still have a lot of marching to do.

Our goals are big. From here, the key questions are this. Where are we? Where are we going? And how are we going to get there? First, where are we? Today, Carvana sits in the strongest position we have ever been in for five reasons. I would ask that you come back to this and evaluate each element for yourself. Number one, our customers love the experiences we deliver. And as we execute these experiences are getting even better. Number two, the financial power of our business model is becoming clearer every quarter and is highly differentiated across every line item of our income statement. There remain many significant opportunities for additional improvement. We plan to get them. Number three, our infrastructure is simply unmatched. We have built a vertically-integrated machine with 6,500 acres of land and over 500,000 parking spots that scalably and cost effectively gets cars from one customer to another more efficiently than any other machine that serves the same purpose.

Number four, competitively, we have never had more separation. As we continue to execute, that gap is getting bigger. And number five, we compete in a $1 trillion market, and we currently have approximately 1pc market share. The potential is obvious. So where are we going? From the early days of Carvana, we have never flinched in our goals. They have been and remain to become the largest and most profitable automotive retailer and to buy and sell millions of cars per year. And finally, how are we going to get there? We are going to continue to march. We are still an ambitious group with big dreams and hustle. We will keep sprinting in our goals to drive as much positive changes as we can as quickly as possible as we always have. We are also a group that is constantly learning.

Every stage in Carvana’s journey teaches us new lessons and adds to our toolkit. As long as that is true, and as long as we always get back up, our best day is always today. The march continues.

Ernie Garcia, CEO and co-founder, Carvana, Q4 2023, 22 February 2024

As Garcia says Carvana still has a long way to go, just as Ashtead’s management would have said in the early stages of their recovery, but they are on their way.

First, our FY2023 results and Q1 2024 outlook resoundingly demonstrate the ability of our online sales model to generate significant adjusted EBITDA.

Based on our Q1 outlook, we expect to generate significantly above $100m of adjusted EBITDA, equating to significantly above $1,200 per retail unit sold. Despite declining used vehicle prices, industry volumes that remain below pre-pandemic levels and sizable costs of carrying capacity for future growth. Second, we are now beginning to demonstrate record adjusted EBITDA profitability while also showing early signs of growth. Based on industry data sources, we gained market share on a sequential basis in Q4 and our outlook calls for retail unit growth not only on a sequential basis, but also on a year-over-year basis in Q1 and in full-year 2024. Third, we have a unique and powerful infrastructure for significantly and efficiently scaling retail unit volume with excess capacity in our existing footprint to support multiples of profitable growth.

We expect this growth to be paired with significant operating leverage as we leverage our underutilised overhead costs.

Mark Jenkins, CFO, Carvana, Q4 2023, 22 February 2024

Root is on a Similar Journey

I have used these quotes before for Root but they are worth repeating.

Just over 2 years ago, we underwent a crisis as we saw used car prices soar and observed the worst inflationary environment in recorded history. It was clear that we needed to pivot our business. This entailed making a number of decisions that, while difficult in the near term, were ultimately the necessary and correct decisions to ensure we evolved our company and positioned ourselves to be able to fully disrupt the auto insurance industry. To do this, we crafted a 3-step plan. One, drive toward healthy margins on our business by hitting our target loss ratios; two, materially lower our fixed expenses; and three, efficiently grow to scale in order to drive profitability.

Fast forward 2 years and we believe the transformation is remarkable. For the full year 2023, we restarted our growth engines, increasing gross written premiums by 31pc and policies enforced by 55pc. We generated a Direct contribution of $151m. That’s nearly a 20x expansion from just 2 years ago. We recorded a gross accident period loss ratio of 66pc and a gross combined ratio of approximately 116pc, both major improvements while also validating our efforts to enhance our tech and data capabilities.

Alex Timm, CEO and founder, Root Inc., Q4 2023, 21 February 2024

I have just noticed that Root and Carvana report on successive days, at least they did in February. In investment terms, they have so much in common.

Like Ashtead in 2004, Carvana and Root have turned the corner, hence the explosive rise in their share prices as investors begin the pivot from discounting imminent bankruptcy to discounting growth.

2023 was a transformative year for Root, as we returned to growth, recorded sustained improvements in our loss ratio, appropriately aligned our fixed expense structure and pivoted our reinsurance strategy going forward. As a result, we are entering 2024 in a position of strength and we will continue to be mindful of our underwriting and expense management in order to remain on the path to profitability.

Megan Binkley, CFO, Root Inc., Q4 2023, 21 February 2024

Like Carvana, Root is a company with ambitious plans addressing a huge industry.

We could not be more excited for the long-term potential of Root.

Alex Timm, CEO and founder, Root Inc., Q4 2023, 21 February 2024

Strategy – Buy Root and Carvana

The CEOs of Root and Carvana are both young men, 32 and 41 respectively, so time left for world conquest.

My best guess, wildly ambitious, is that both companies will see their shares recover the previous peaks, $538 for Root and $380 for Carvana. If Ashtead is the model even that could still be early days in their progress.

Miracles happen in the stock market and these two companies could be working on theirs.