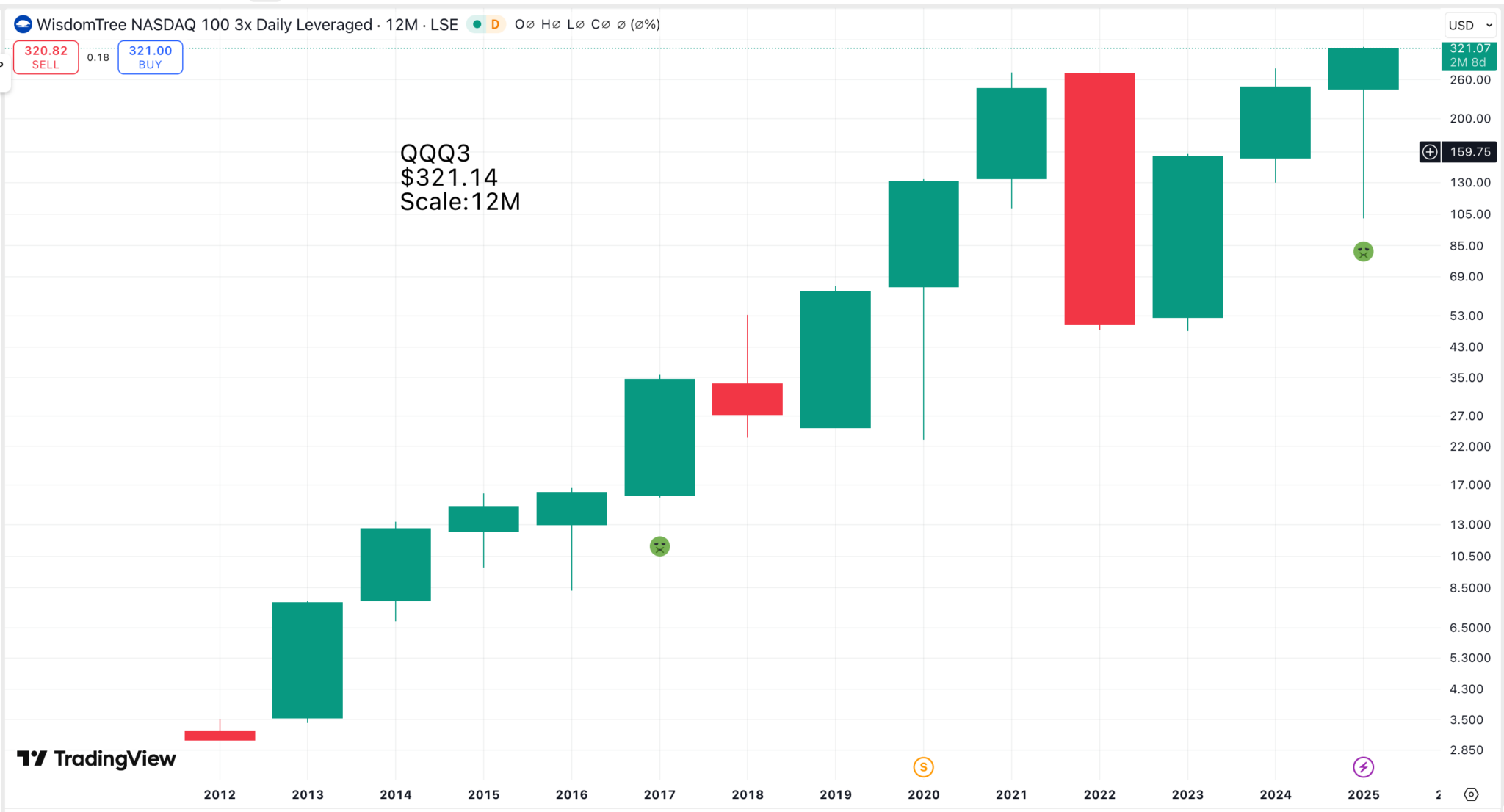

I have never seen anyone else use such long-term charts, but they can be most informative because of the power of the breakouts. Time and again, when share prices fall enough to create a red candlestick (down year) on the chart, this is the precursor to a powerful new buy signal.

There are two breakouts marked by the little green smileys on the chart above of QQQ3. The latest breakout is happening right now and should be a powerful one. Many charts illustrate the power of these breakouts in the past.

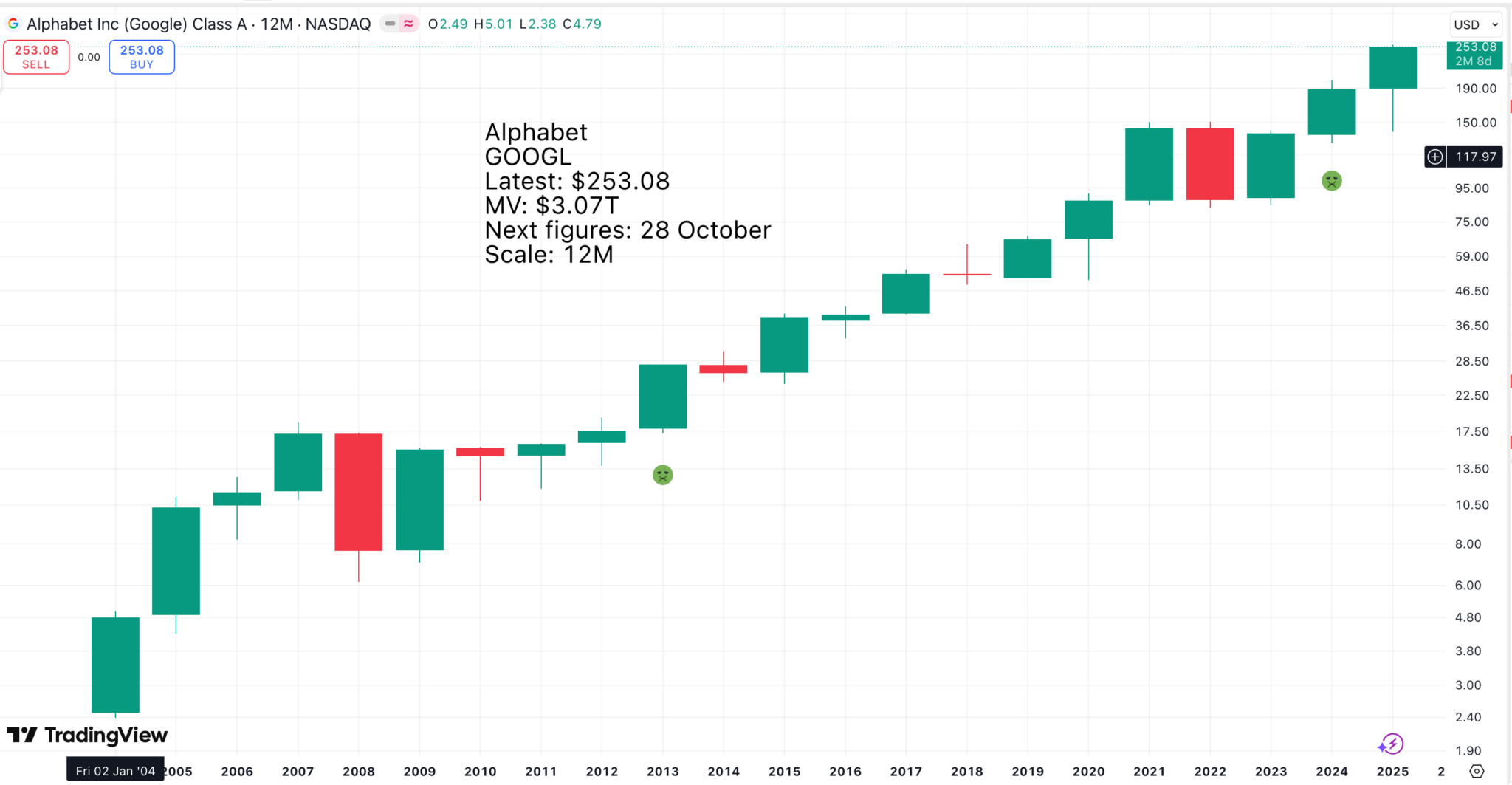

Two such breakouts are illustrated on the Alphabet chart above. Their problem is not their power but their rarity; just two for Alphabet in over 20 years. Most investors don’t operate on those time horizons. However, they give a great perspective for a long-term investor because if the fundamentals are solid, as they are with Alphabet, with many exciting irons in the fire to drive long-term growth, there is always the prospect of another big buy signal ahead. As it happens, the last buy was recent enough to still be driving the share price.

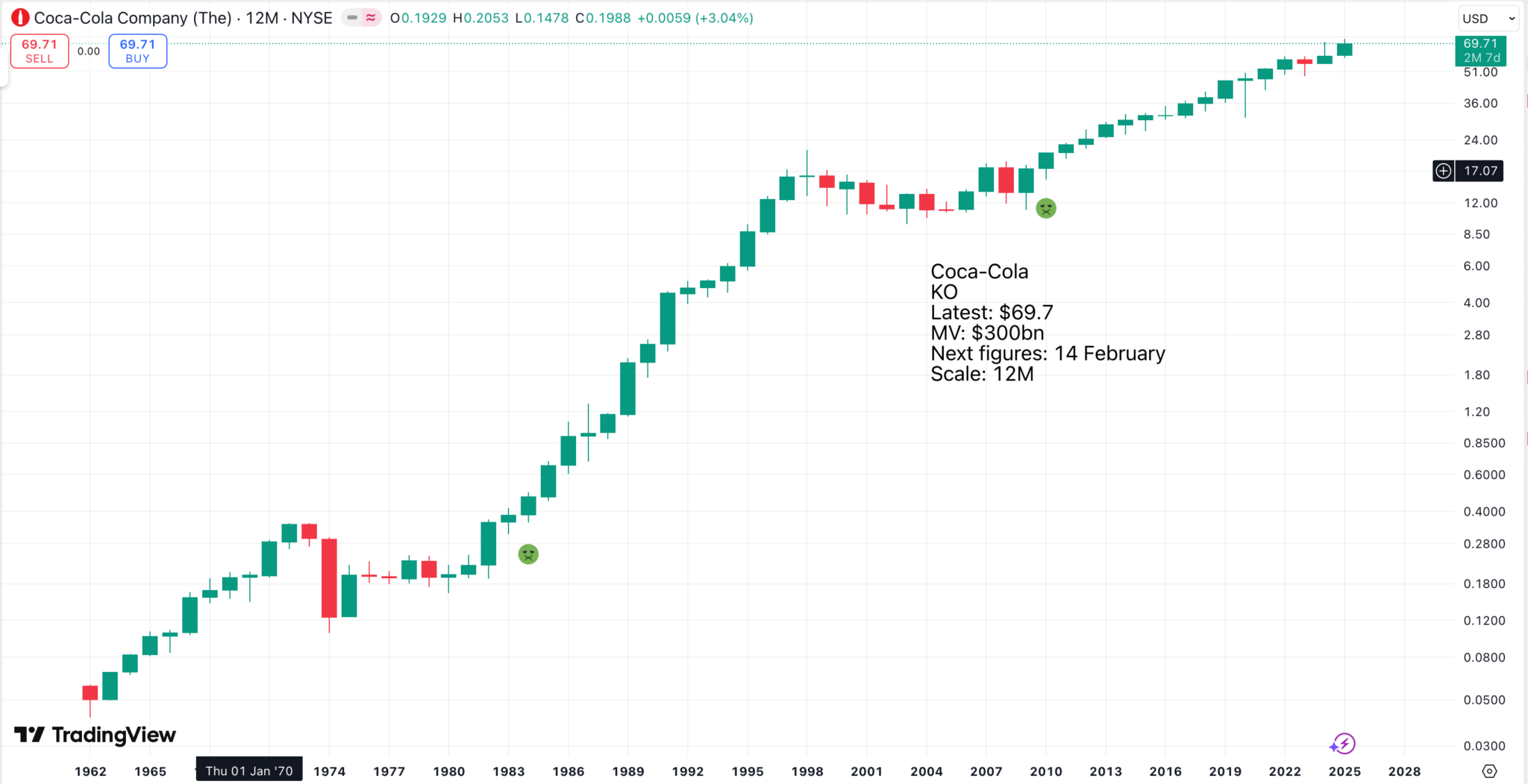

It is amazing how well these super-long-term buy signals work. It is the patience of waiting for signals like these, which are often accompanied by something new in the fundamentals, that has helped make Warren Buffett such a successful investor. He always looked for shares in companies which displayed strong growth, often ones which embodied the American way of life (think Coca-Cola, Gillette, American Express and Apple) and generated plenty of cash.

What a great chart for Coca-Cola. Subscribers may not realise that Coke doesn’t make anything but owns the all-powerful secret formula from which it earns royalties. It is also a brilliant marketing and innovation machine. Other companies do the bottling. In this way, most of the value accrues to Coca-Cola, which generates substantial cash and keeps its shares steadily climbing.

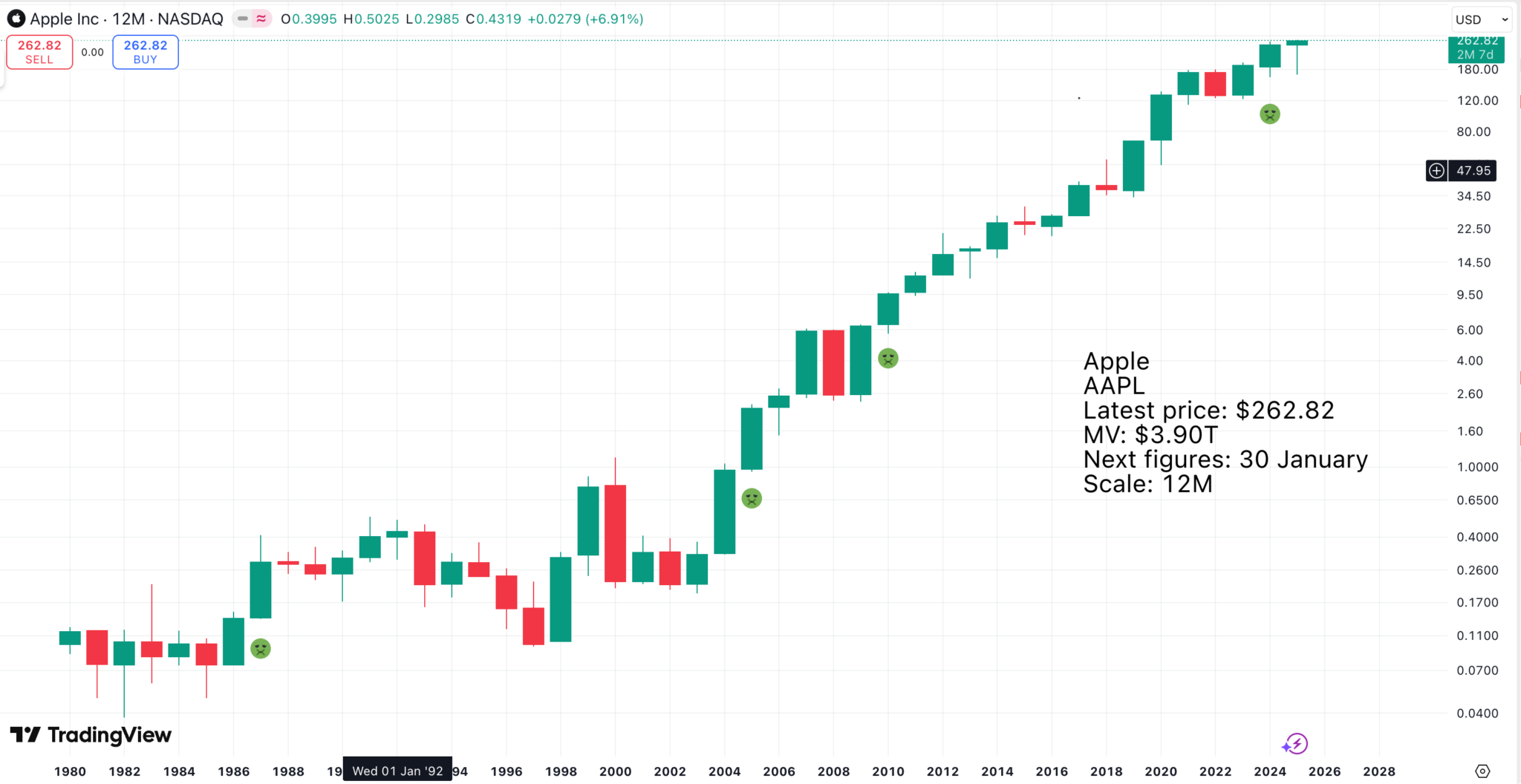

Apple is a similar sort of business in the tech arena. Investors worry that it has fallen behind in the AI race, but with its substantial cash flow and a huge footprint of satisfied users, that is surely temporary. The chart looks great with a recent breakout.

I am adding both Coca-Cola and Apple to the Top 40 List. They may not deliver the explosive performance of some of the smaller, more blue-sky selections, but we need a mix of different types of shares. Apple is famous for using much of its cash to reward shareholders with dividends and share buybacks.

Coca-Cola is an amazing company.

We benefit from operating in a vibrant and resilient industry with ample headroom for growth. For the 18th consecutive quarter, we gained overall value share. We also held or gained value share across each of our geographic segments. By offering consumers choice across our total beverage portfolio by leveraging our systems capabilities, we continue to build momentum to develop our industry and expand our lead over the long term.

To deliver in today’s environment, we’re capitalizing on the strength of our portfolio and focusing on improving execution across all aspects of our strategic growth flywheel. We have unparalleled portfolio power as demonstrated by our 30 billion-dollar brands, which we estimate represents approximately 1/4 of the billion-dollar brands in the industry is approximately double our nearest competitor.

As we continue to develop love brands, we expect our number of billion-dollar brands to grow. Our marketing transformation is centered on connecting deeply with consumers through digital engagement, personalized experiences, and cultural relevance. For example, we recently partnered with Universal Pictures and Blumhouse on a Halloween campaign for Fanta that was activated in approximately 50 markets. Building on last year’s success, the campaign featured iconic power characters on our packaging, limited-time flavors and immersive retail and digital experiences. While we’re building capabilities in marketing, we’re also prioritizing bigger and bolder innovation like Sprite + Tea in North America, BACARDÍ Mixed with Coca-Cola in Mexico and Europe and Powerade Springboks addition in South Africa.

James Quincy, chairman and CEO, Coca-Cola, Q3 2025, 21 October 2025

The bottling strategy is more complicated than I thought.

Over the past decade, we’ve been on a journey to re-franchise company-owned bottlers to fortify our system and unlock further growth. Recently, we reached 2 significant steps in completing this journey.

In July, we sold a 40% ownership stake in our company-owned Indian bottler to the Jubilant Bhartia Group. Additionally, this morning, Coca-Cola Hellenic announced its intention to acquire a controlling interest in Coca-Cola Beverages Africa, which is expected to close next year, subject to regulatory approvals. We believe these moves will unlock growth opportunities in India and Africa. Jubilant Bhartia has built and grown consumer businesses in India and Coca-Cola Hellenic has demonstrated a strong track record in Nigeria and Egypt.

Our global franchise model is a strategic differentiator and is very difficult to replicate. With these milestones, we have a clear line of sight to complete our re-franchising strategy allowing us to further focus on brand building and innovation complemented by integrated execution with our bottling partners.

James Quincy, chairman and CEO, Coca-Cola, Q3 2025, 21 October 2025

Coke is like the conductors of an orchestra.

Like all American companies, there is no woolly b******t about looking after numerous stakeholders; shareholders own the business, they come first, and they are well looked after.

Free cash flow, excluding the fairlife contingent consideration payment was $8.5 billion, which was an increase versus the prior year. Growth was driven by underlying business performance and lower tax payments, partially offset by cycling working capital benefits in the prior year. Our balance sheet remains strong with our net debt leverage of 1.8x EBITDA, which is below our targeted range of 2x to 2.5x. We’re confident in our long-term free cash flow generation and have ample balance sheet capacity to pursue our capital allocation agenda, which prioritizes reinvesting in our business and returning capital to our share owners.

John Murphy, CFO, Coca-Cola, Q3 2025, 21 October 2025

Coca-Cola is solid and a reliable, great American growth stock, but subscribers may feel Amphenol is something else, a little more exciting but still full of all-American get-up-and-go. You guessed it. I love America and Americans; eat your heart out, Jeremy Corbyn, with your sad obsession with Venezuela and North Korea as role models for a perfect world.

Amphenol has been a fabulous slow-burning investment. In 1994, the shares were seven cents. Some 30 years later, they have risen 1,911 times! Talk about a classic buy-and-hold.

The electronics revolution continues to create exciting, long-term growth opportunities for Amphenol. We remain global leaders in developing new applications to drive demand for our broad range of high-technology products across all of our diversified end markets. Our ongoing actions to strengthen our competitive advantages and build sustained financial strength while expanding our high-technology product offering both organically and through our successful acquisition program have created an excellent base for future performance.

Amphenol website

Acquisition programmes often play a key role in long-term growth stories. Quoted companies can use their valuable paper (shares) to buy cheaply while offering exciting value to shareholders in the acquired business. They can take overhead out of the acquired business, offer more exciting career opportunities to employees, step up investment and, if relevant, back its products with a powerful marketing machine.

The latest results were stunning.

“We are pleased to have closed the third quarter of 2025 with record sales and Adjusted Diluted EPS, both significantly exceeding the high end of our guidance,” said Amphenol President and Chief Executive Officer, R. Adam Norwitt. “Sales increased from prior year by 53%, driven by strong organic growth in virtually all of our end markets, including exceptional organic growth in the IT datacom market, as well as contributions from the Company’s acquisition program. In the third quarter, we once again realized excellent profitability with Operating Margin reaching a record 27.5%. We are extremely proud of the Company’s outstanding performance.”

The Company continues to deploy its financial strength in a variety of ways to increase shareholder value. During the third quarter, the Company purchased 1.4 million shares of its common stock for $153 million and paid dividends of $201 million, resulting in total capital returned to shareholders of approximately $354 million.

Amphenol remains focused on expanding its growth opportunities through a deep commitment to developing enabling technologies for customers across its served end markets, an ongoing strategy of market and geographic diversification as well as an active and successful acquisition program. To that end, the Company is excited to have completed the acquisition of Rochester Sensors in August 2025. Based in Dallas, Texas and with annual sales of approximately $100 million, Rochester Sensors is a leading manufacturer of highly engineered, application-specific liquid level sensors primarily for industrial applications. The Rochester Sensors business is included in the Company’s Interconnect and Sensor Systems segment.

The Company also remains excited about the previously announced acquisitions of the CCS business from CommScope as well as Trexon. Amphenol continues to expect the Trexon acquisition to close by the end of the fourth quarter of 2025. The Company now expects the CCS acquisition to close by the end of the first quarter of 2026.

Q3 2025 results, 22 October 2025

I have been reading the company’s comments on the latest Q3 results. The company’s end markets are broadly based, and everything gets a mention, from mobile devices to defence, to industrial and automotive. This widespread range of activities makes it easier to find acquisitions to slot into its wide-ranging operations.

You can also see how acquisitions help drive performance. Trexon was bought at around four times sales, but Amphenol is valued at between seven and eight times sales. This is before Amphenol has worked its magic to improve Trexon’s performance.

Amphenol has much in common with another successful Top 40 share, Broadcom (AVGO), which is a serial acquirer in the semiconductor and networking spaces.

Share Recommendations

QQQ3

Alphabet GOOGL

Microsoft. MSFT

Coca-Cola KO

Apple AAPL

Amphenol APH

Comfort Systems. FIX

Strategy – Keep Taking The Pills

The simplest explanation of what is happening in America is that an epic, technology-driven bull market is in full flight. The odds favour buy-and-hold investors. I am adding KO, AAPL and APH to the Top 40 portfolio, which is up to 45 shares (Top 50 here we come).

The constant additions bring the performance figures down. The average gain on all 45 shares at entry prices is 12pc.

Slow investing is a great way to invest. Climb aboard shares at any stage and be prepared to add more on great buy signals.

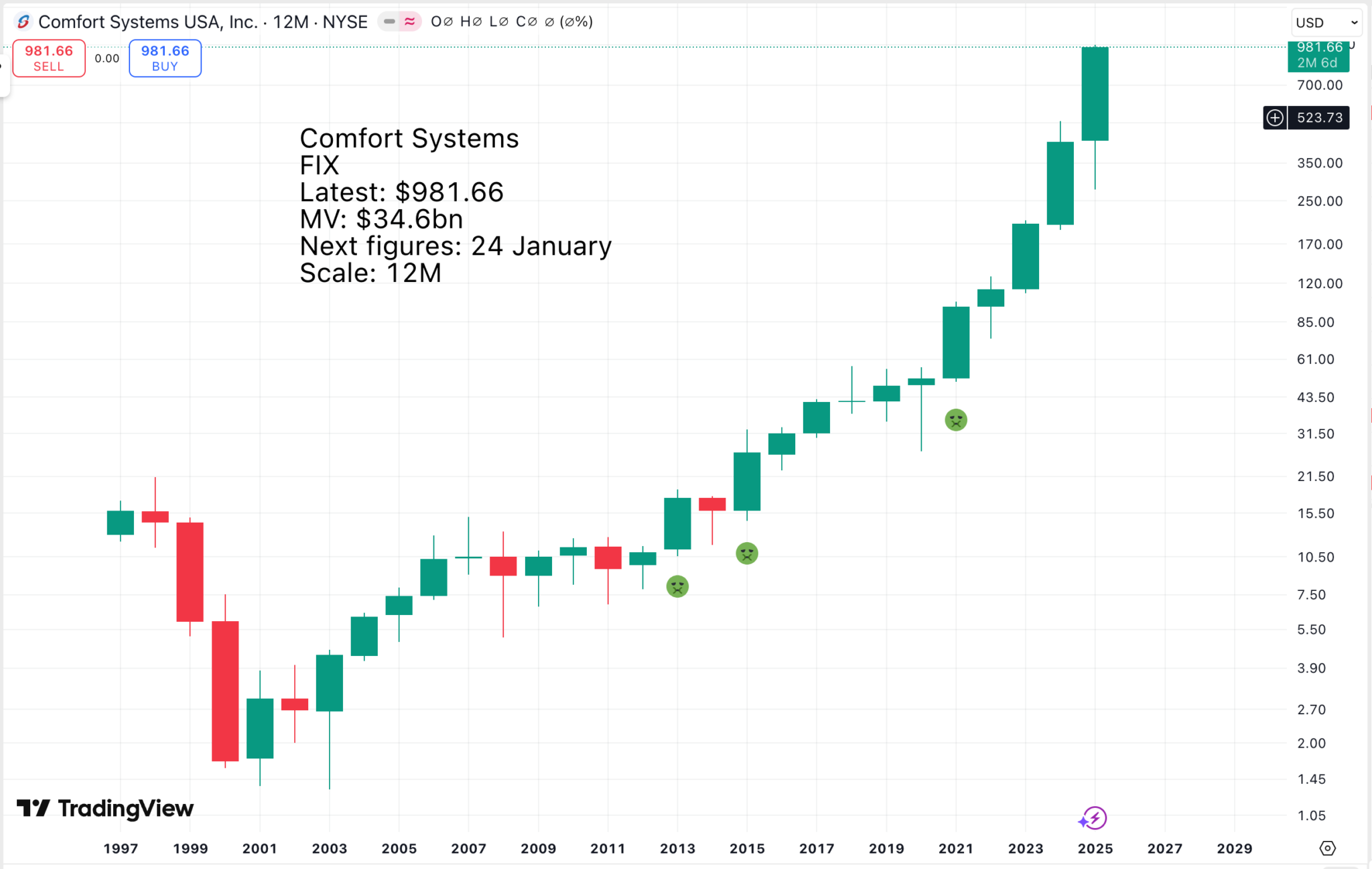

Another Top 40 stock, Comfort Systems, has just announced stunning figures.

Our amazing teams across the country continue to deliver excellent results for our customers, and they have delivered financial results that far exceed even our recent outcomes. We earned $8.25 per share this quarter, which is double what we earned in the same quarter last year. Our mechanical business had a sharp increase in profitability, and our electrical segment was higher as well. We also had favorable developments in some late-stage projects that contributed to our great results.

Construction is driving most of our results, but service revenue and profit also grew by double-digit percentages. Our bookings were strong, and our backlog at the end of the quarter grew to a new high of $9.4 billion. As a result of exceptional demand for our services, we achieved a second consecutive same-store backlog increase of more than $1 billion despite significant third quarter burn. We continue to book work with good margins and good working conditions for our valuable people. We entered the fourth quarter of 2025 with $3.7 billion more in backlog than last year at this time.

Brian Lane, CEO, Comfort Systems, Q3 2025, 24 October 2025

Comfort Systems is another serial acquirer, and prospects look good for more strong growth.

I’m happy to announce the acquisition of 2 companies on October 1. FZ Electrical, a contractor with strong industrial capabilities located in Grand Rapids, Michigan; and Meisner Electric, a contractor based in Boca Raton, Florida, with strong capabilities in health care and other attractive markets. We are thrilled to have these 2 companies join the Comfort Systems USA family of companies, and we welcome them.

Today, we increased our quarterly dividend by 20% to $0.60 per share, and we have actively purchased shares during 2025. With solid bookings and great demand, we expect continuing growth and strong results in 2025 and 2026.

Brian Lane, CEO, Comfort Systems, Q3 2025, 24 October 2025

The data centre boom is a big factor in what is happening at Comfort Systems.

The opportunities, the pipeline is still robust, matching quarter 3. There’s still more opportunities that then probably can be handled out there in the market at the moment. So we’ve seen no let up at all in the opportunities.

Brian Lane, CEO, Comfort Systems, Q3 2025, 24 October 2025

It is amazing what is happening.

We haven’t changed our capital allocation thinking since 2007. We will — to the extent we can find opportunities that we have conviction around, we will deploy most of our cash doing acquisitions. We will continually buy back our shares using a portion of our free cash flow, and we get aggressive on that when we feel like the stock has dipped to — relative to our prospects. So for example, when it dipped earlier this year, we spent $100 million in a couple of weeks buying shares.

And then we — one point you might be making is there’s so much cash now. Is it realistic for us to deploy it into acquisitions? And I think the answer is we’ve faced that problem on a couple of stair steps in our cash over the last few years. So far, our reputation as an acquirer and our commitment to great outcomes for the people we buy have allowed us to find good opportunities to deploy our cash.

One thing people might not think about is we are growing, but the companies we’re buying are growing as well. There’s a certain amount of scaling going on. So I meet with companies regularly that are having — that have results that are twice as big as they were 2 or 3 years ago. And so in a sense, the reality is the opportunity set that’s facing a company with a great, deep, well-established workforce of pipe fitters or electricians is amazing. These companies are worth more today than they were 5 years ago just because of actually what’s going on because of the investments they’ve been making in the meanwhile.

It’s just a fantastic market, and we have just unbelievably good companies.

Brian Lane, CEO, Comfort Systems, Q3 2025, 24 October 2025

The robots are coming.

In terms of the history of construction, the amount of innovation and technology that’s being developed and applied today leaps and bounds over what it’s ever been. And it’s going to be a huge help into helping us build stuff as we go forward safer, more productively and the quality is getting better every day.

Brian Lane, CEO, Comfort Systems, Q3 2025, 24 October 2025

Technology is driving the boom.

Our biggest single booking, I think, in the last couple of quarters was in pharma, but the majority of our bookings today are in technology. It’s not because there aren’t pharma opportunities. It’s because technology is competing for our resources and they’re making a compelling case for our resources.

Brian Lane, CEO, Comfort Systems, Q3 2025, 24 October 2025