In this issue I am recommending another 39 shares, 37 from the existing portfolio and two new ones. This means I will have recommended buying most of the shares in the portfolio.

My core theory remains the same that the key drivers of rising share prices are US technology shares and they should be the bedrock of any 21st century portfolio. But I am supplementing that with another theory, elaborated below.

The chart above is of the US S&P 500 index. It is the best chart to encapsulate the performance of corporate America. If the business of America is business this is the chart that takes the temperature of what is happening. Since 2009 the S&P 500 has risen roughly 4.4 times.

I have another chart of the S&P 500, which goes back practically to the American civil war. In July 1932 the index fell to 4.77, the low point of the 1929 collapse. Since then it has been in what looks almost like an unbroken bull market, rising 616 times as American has grown to be the world’s preeminent economy.

It is less dominant than it was as other centres have risen including Europe, China and emerging economies. Observers sometimes paint the US as a loser in this process as their share of global trade and GNP falls but I see them as a gainer because of the huge increase in size of the markets that US business can address in 2020. The world really is their oyster and some colossal businesses are being built as a result.

July 1932 was a great time to buy US shares at very low levels. Global business reset and a long period of growth took shape, albeit it began slowly and there was a serious interruption from WW2, which made 1940 another great buying opportunity.

I am beginning to see the sharp 1929-style fall in output/ rise in unemployment triggered by Covid-19 and the global lockdown as providing a similar reset and arguably a somewhat similar buying opportunity. Some analysts have been arguing for a while that a bear market began in January 2018 and it is this bear market that hit bottom in mid-March 2020.

This may be more apparent from a chart below of the Russell 2000, which tracks the performance of the 2000 US-quoted shares suitable for institutional investment excluding shares in the 1000 largest quoted companies. There are three indices, the Russell 1000 of the largest 1000 shares, the Russell 2000, a bit like the FTSE 250, which includes the next biggest 2,000 shares and the Russell 3000, which includes all of them.

The Russell 2000 topped out in August 2018 and has only recently recovered to a level first reached in October 2016. It is well below the average levels of 2018 and 2019 so, you could say, still very much in bear market territory. At the low point in mid-March it fell to 961.85. which is down around 45pc on the peak. It has done worse than other indices like the Nasdaq 100 because it doesn’t contain all the outperforming big tech stocks like Apple, Microsoft, Amazon, Alphabet, Facebook, Netflix, Adobe, Nvidia and others. It may take a while to reach new highs but has surely passed the bear market low point.

I expect big tech and the Nasdaq 100 to continue to outperform but I also think that the global economy may be resetting in a way with parallels to 1932 and setting up for another long running bull market. The world was different after 1932 and especially after the war. I think it is going to be different after the pandemic but increasingly I am thinking it is going to be different in a good way and that this is going to be good for shares.

We have a combination of a globally connected economy, an accelerating technology boom, an extraordinary spirit of co-operation in many countries, a taste of a less polluted world, interest rates close to zero in developed countries and governments and central banks on a mission to drive a far-reaching economic recovery. You could see this as a very bullish backdrop for shares and increasingly I do though many businesses are going to have to change and they will.

I have accordingly gone through the Quentinvest portfolio again and I am recommending shares in another swathe of companies that didn’t quite make the cut the first time around. They are not a second division group. If I didn’t think they were good world-beating businesses I would not be recommending their shares. They are 3G, they have the magic and I expect these shares to also perform well and reach new highs in the future. What has changed is that I think a new bull market has begun and new highs for global shares lie in the future and not the distant future – this year or next year.

AB Dynamics/ ABDP Buy @ 1735p

Alibaba/ BABA Buy @ $204.3

Alteryx/ AYX Buy @ $113.35

Anaplan/ PLAN Buy @ $41.57

Ashtead/ AHT Buy @ 2207p

Autodesk/ ADSK Buy @ $187.80 (new entry)

Blue Prism/ PRSM Buy @ 1279p

Brunello Cucinelli/ BC Buy @ €28.66

Croda International/ CRDA Buy @ 4868p

CyberArk Software/ CYBR Buy @ $98.96

Dexcom/ DXCM Buy @ $341.5 (new entry)

Disney (Walt)/ DIS Buy @ $109.20

Domo Inc./ DOMO Buy @ $19.34

Ecolab/ ECL Buy @ $193.50

Estee Lauder/ EL Buy @ $176.25

Experian/ EXPN Buy @ 2425p

Facebook/ FB Buy @ $206.20

Fair Isaac/ FICO Buy @ $352.00

Fiserv/ FISV Buy @ $102.5

Hubspot/ HUBS Buy @ $169.66

Intertek/ ITRK Buy @ 4790p

Kering/ KER Buy @ €459.25

Keywords Studios/ KWS Buy @ 1569p

Learning Technologies/ LTG Buy @ 127.25p

Liontrust Asset Man./ LIO Buy @ 1060p

Magellan Financial/ MFG Buy @ A$51.02

Renishaw/ RSW Buy @ 3500p

Rotork/ ROR Buy @ 250.2p

Salesforce.com/ CRM Buy @ $164.2

Sanne Group/ SNN Buy @ 662p

Shake Shack/ SHK Buy @ $55.7

Shotspotter/ SSTI Buy @ $35.20

Spotify Technology / SPOT Buy @ $148.95

Stamps.com/ STMP Buy @ $161.3

Twlio/ TWLO Buy @ $116

Visa/V Buy @ $179.5

Wandisco/ WAND Buy @ 566p

Workday/ WDAY Buy @ $157.4

Zendesk/ ZEN Buy @ $79

New entries

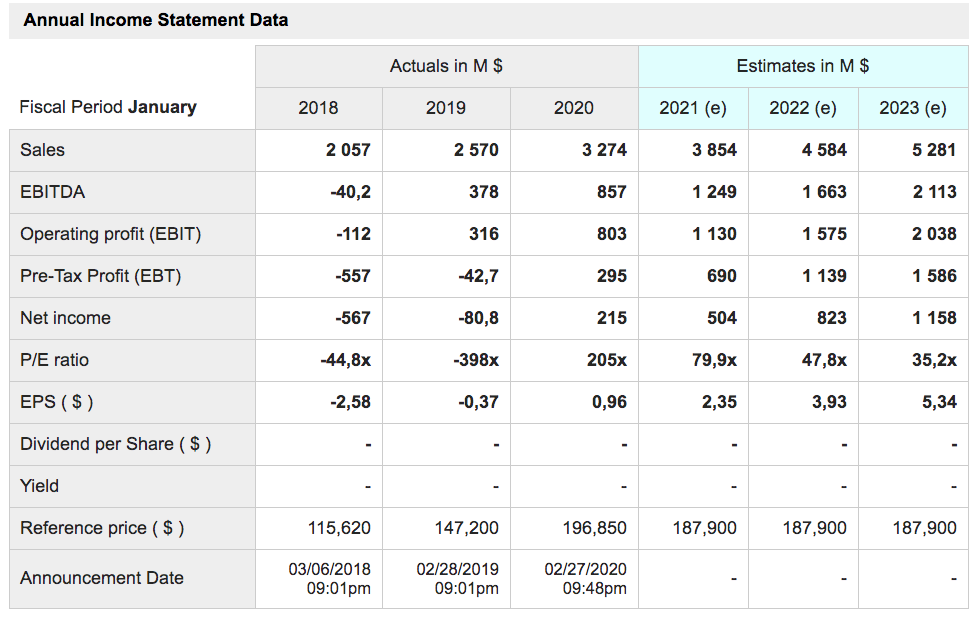

(1) Autodesk is a very sexy business. It makes software for people who make things. If you’ve ever driven a high-performance car, admired a towering skyscraper, used a smartphone, or watched a great film, chances are you’ve experienced what millions of Autodesk customers are doing with their software. The company is growing fast. The first table below gives you an idea of the growth people were expecting for the business. It may be different now, given the pandemic. Many companies have been withdrawing their full year guidance but this is clearly a high-performance business. Here is what CEO, Andrew Anagnost, said about the Q4 2019 results, reported on 27 February: “We closed fiscal year ’20 with outstanding Q4 results with revenue, earnings, and free cash flow coming in above expectations. Recurring revenue grew 29pc and we delivered $1.36bn in free cash flow for the year. Our results were driven by strong growth in all geographies. This was a landmark year for us in construction as we absorbed our acquisitions and integrated our offerings under one platform, the Autodesk Construction Cloud. Subscriptions now represent around 85pc of our revenue and we exited the year with maintenance contributing less than 10pc. Fiscal year ’20 marked the end of the business model transition for us and we are entering fiscal ’21 firmly positioned to deliver strong, sustainable growth through fiscal ’23 and beyond.” He added: “Beyond that, the dramatically reduced upfront costs created by the subscription model have enabled a whole new class of customers to purchase our most powerful tools; opening up not only new opportunities for our business, but for the businesses of our customers as well.” And finally noted that, at least at that stage, the virus was not having much effect on Autodesk:- “The events are not currently impacting our service levels for our customers or global R&D efforts. We will continue to monitor the situation and take precautionary steps.” Autodesk is classic 3G and has plenty of magic.

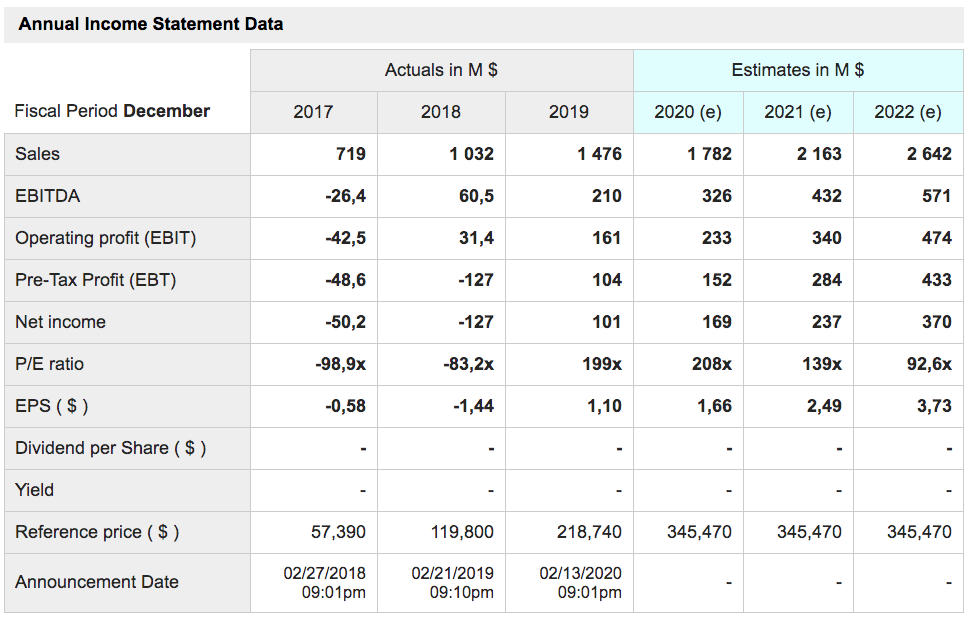

(2) Dexcom is a healthcare business that is disrupting the diabetes market. Diabetes is another pandemic that is having a dramatic effect on the world but it is genetic and lifestyle related rather than infectious so does not affect the global economy in the same way. This is what they say they do: “Dexcom, Inc. empowers people to take control of diabetes through innovative continuous glucose monitoring (CGM) systems. Headquartered in San Diego, California, Dexcom has emerged as a leader of diabetes care technology. By listening to the needs of users, caregivers, and providers, Dexcom simplifies and improves diabetes management around the world.” The business is growing dramatically including explosive growth in international markets. The second table below shows you what is happening.

Finance director, Quentin Blackford, had this to say about how the company was doing at the Q1 2020 results, released on 28 April: “The growth performance reflects the strength of our new patient additions throughout 2019 and the first quarter of 2020 as we continue to see growing awareness of the value of DexCom CGM for both type 1 and type 2 patients. The U.S. business grew 39pc in the first quarter of 2020 over the first quarter of 2019 with strong growth from each channel, durable medical equipment, pharmacy and Medicare. Pharmacy continues to be the fastest-growing channel for us, and realised the strongest sequential uptick in utilisation to date as a result of the significant access improvements that our team has driven over the past year.

Our international business also put up a great first quarter, growing 63pc on a constant currency basis relative to the same quarter in 2019. The $112.8m in revenues for our international business represents an increase of more than $25m from our previous quarterly high watermark. Strength was across the board, including both direct and distributor markets. Our first-quarter gross profit was $258.7m or 63.9pc of revenue compared to 60.2pc in the first quarter of 2019.”

He admitted that Covid-19 was affecting new patient recruitment but had this to say: “The thing is coming out of the quarter or over the course of the first quarter, the strength in the core business, the underlying business was incredibly strong. And I think from our perspective, we’re as bullish as we’ve ever been on where we’re at in this opportunity, the runway that exists in front of us. And probably even more so now when you think about the long term, just with the hospital opportunity opening probably sooner than what we anticipated. The whole play in telehealth, telemedicine, we know we have a device that works better there than anything else in the marketplace. And folks seem to be understanding that. So I think long term, we feel incredibly bullish about where we’re at. In April, yes, the new patient starts were down a bit. We noted that coming out of Q1. We have seen it start to rebound a bit in April. I think it continues to build over time. But we need to see that play out and have some certainty there before we can get back to where we feel comfortable providing guidance. There’s just too many things that are uncertain at this point in time that we need that greater clarity on. But I would just reiterate, the underlying strength, the fact that folks are recognising the value of this product and what it means in the marketplace. From a long-term perspective, we’re as bullish as we’ve ever been.”

Plenty of magic there, then and obviously classic 3G

The big picture view for me is that global stock markets hit a massive speed bump with the lockdown triggered by the coronavirus pandemic.There is still much uncertainty about how things are going to develop and plenty of economic bad news in the pipeline but I think in sentiment terms the worst is behind us, that a new bull market is taking shape and that we should treat the setback as a buying opportunity. I have now recommended buying virtually all the shares in the QV for Shares portfolio that I believe have an exciting future plus added some new names. There are one or two I am still watching but generally speaking if I have not included them in the lists of recommended shares since mid-March that is because they are no longer 3G.