More on Upstart Holdings, the interloper aiming to transform global banking

Upstart Holdings. UPST. Buy @ $297. Times recommended: 14 First recommended: $62.50 Last recommended: $318

I have recommended Upstart very recently at a higher price but nevertheless I am returning to the subject partly because it has so many mysterious and exciting features.

One which stands out is the incredible rise in the shares in a short time since the IPO. The shares were placed in December 2020 at $20 and less than a year later hit a peak $346. The natural assumption of most observers is that this is a ridiculous rise in such a short period of time and the shares must be grotesquely over-valued.

I have approached it from a different perspective by asking myself if maybe the December 2020 placing price was far too low. At $20 the company was valued at $1.45bn against over $20bn now. The people who set the price were banks, Goldman Sachs, Barclays and others, the very people whose lending business Upstart is planning to massively disrupt.

It is also noticeable that although Upstart offers to partner with banks none of these banks is a partner. Whatever Upstart is doing it seems they don’t want to get involved which surely disqualifies them as suitable people to put a value on the business. Indeed the contrast between their obvious lack of enthusiasm and what co-founder and CEO, Dave Girouard, had to say in his founder’s letter in the prospectus could hardly be more striking.

Girouard describes banking as a vast but inefficient industry – yes, Barclays, he is talking about you. He says the ways in which banks decide whether or not a loan will be repaid are closer to a roll of the dice than the workings of an omniscient deity.

He then goes on to provide proof that Upstart’s AI-based algorithms work better. Studies the group has carried out with three US banks demonstrated they could approve up to three times the number of borrowers at similar default rates. Furthermore the effectiveness of the model has improved 10-fold since Upstart launched eight years earlier. And on top of that he says that good as the model is today it still only scratches the surface of the gains that are possible.

I may have been a little unfair to Goldman Sachs. Many of the loans that originate on the Upstart platform are sold to a consortium of institutions. Goldman Sachs is one of those institutions.

How big is this market that Upstart is addressing with its amazing, proprietary technology? It’s worth $4.2 trillion just in America. So what did these banks, in their wisdom, think that Upstart was worth – a measly $1.45bn. They don’t get it or they don’t believe him; that is what the pricing of these shares tells us.

As soon as the company was floated and investors who wanted to make money as opposed to bankers with poles stuck up their backsides were able to have a go at the shares the price rocketed to $165 in four months! Which raises another amazing thought. In the flotation most of the shares sold were raising new money for the company but some idiots sold $56m of their own shares. I bet they feel sick now – so much for the omniscient investing skills of the venture capital community. Those $56m of shares would be worth $823m less than a year later.

It turns out 1m of those shares came from Girouard. He kept the vast bulk of his holdings but it still seems an extraordinary decision. The venture capitalists also kept most of their shares.

I identify two stages in the amazing run up in the Upstart share price with the initial fuel being supplied by the ludicrous undervaluation of the IPO by the banks. The first stage of the rise came when investors read the prospectus and asked themselves if Girouard knew what he was talking about because if the did this was an incredibly exciting share. They probably also though maybe he did know what he was talking about since this guy has a string of degrees and spent eight years as president of enterprise computing at Google with a staff of 1,000 people working for him.

How many of the bankers who set the price had anything like his knowledge and experience?

The second stage came when the company started reporting its trading results and these made the bankers look even bigger fools while proving out Girouard’s thesis that Upstart is facing one of the great opportunities in investing history. One analyst described Upstart’s Q2 2021 results, their latest, as the most amazing set of results he had ever seen.

“I want to do a quick quibble with some of my colleagues here on the sell side [with comments like] pretty impressive results, and another strong quarter. Seems a bit understated when you’re talking about quadruple digit growth, which might be a first in my career. What’s more impressive is as you mentioned early on, this was on the back of an — even if you take that out, that Q2 of last year was you turned off revenue. So — but if you compare it to Q2 of ’19, you’re still looking at fivefold growth on that year. And if you look at the TransUnion data and other data on the personal loan market, obviously, the personal loan market is still down as credit card balances have fallen.”

Hats off to Nat Schindler of Bank of America Merrill Lynch who made the comments above, I know he does get Upstart because I watched a fascinating interview between him and Girouard.

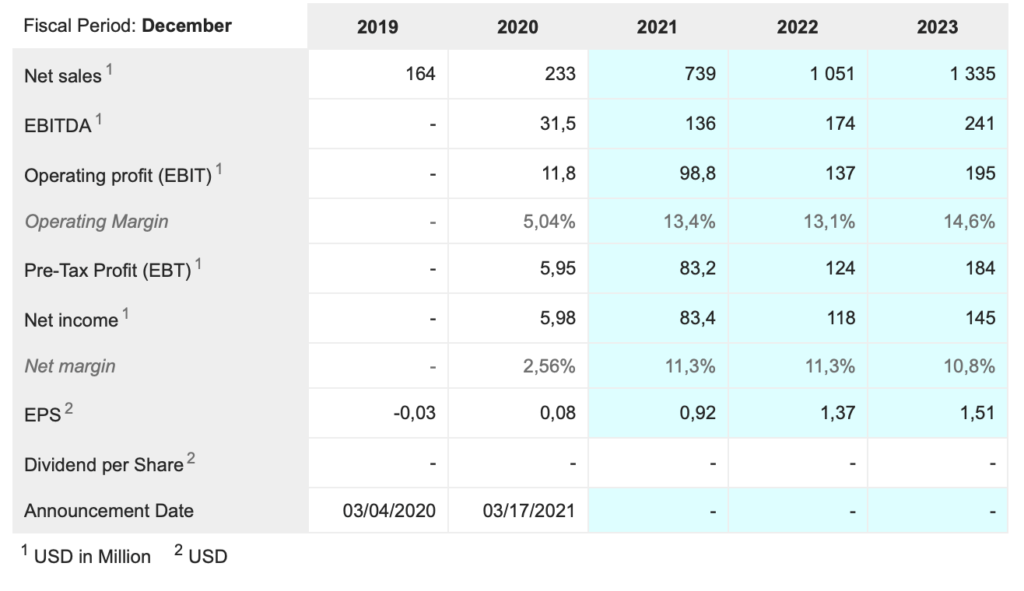

The course of events on those latest quarterly results has been extraordinary. Investors love it when companies deliver what they call a ‘beat and raise’. The company beats with its actual results and raises the guidance. Now let us look at what has been happening at Upstart. Since the IPO they have reported three sets of quarterly figures, Q4, 2020, Q1 2021 and Q2 2021. At the time of Q4 they were guiding for FY2021 sales of $500m, by Q1 2021 this had gone up to $600m and they then raised it again to $750m with the Q2 2021 figures. Could it go up again with the Q3 2021 figures and be higher still when they actually report Q4? We shall see. It certainly suggests that the projections for 2022 and 2023 in the table below are very cautious.

Meanwhile you can also wonder what they might have forecast at the time of the IPO. As it happens they are not allowed to give guidance with the IPO to prevent any attempts to massage the price. However I am sure the guidance would have been less than $500m, maybe closer to $400m so the projections have most likely almost doubled since then. The performance of the business is improving so fast nobody can keep pace.

But what is really important is what that improvement says about Dave Girouard and his belief that Upstart can become one of the world’s largest and most important financial technology businesses. Maybe he is right in which case (a) that IPO valuation of $1.45bn is one of the great investment steals of history and (b) even a $22bn valuation could be a drop in the bucket compared to where this business could be going.

This brings me to another mystery about the Upstart story which is the attitude of the banks, except that I don’t think it is a mystery as we shall see below. Upstart has come along with what is clearly a better mousetrap. Their technology leads to improvements in the performance of loans which Upstart co-founder and technology leader, Paul Gu, describes as ‘stunning’. So why are the banks not rushing to get on board. No doubt Upstart charges more for its AI-powered algorithms than Fair Isaac charges for its vastly simpler and less effective FICO scores but surely the banks would be ready to absorb that for something so massively beneficial for their customers.

After all these are the people who bombard us with advertising telling us that even Mother Teresa never had our interests at heart the way our friendly bank managers do. Or do they? Are they in fact lying through their teeth? Well, I know what I think.

The truth is that the current situation works very well for banks even if if leaves millions of potential customers out in the cold without a loan and millions more paying far more than they should be. Banks take in vast sums in deposits, some of which sits in current accounts so they don’t even have to pay for it. Then they lend it out at multiples of the rates of interest which they pay for funds.

It’s true than when they lend they have no idea if they are going to be repaid but they don’t care because like Shylock in a famous play if they don’t get repaid they will seize their pound of flesh. This is because the vast bulk of bank lending is secured against assets – cars, houses, businesses, jewels, shares, paintings, land. They make sure that their loans are always well covered.

The FICO score is just another filter to help them weed out people who are obviously high risk. People, who have defaulted on earlier loans for example. It’s a great system for banks and if it leads to them lending to many people who still do default that is not a problem because (a) any losses are covered by the high rates they charge to people who do repay their loans and (b) they have those assets which they can seize.

Their only real problem is if there is a deep recession and suddenly huge numbers of people cannot repay their loans and assets start falling in price and becoming hard to sell. So banks expend enormous energies on trying to predict the unpredictable – when is the next recession coming.

Upstart even has the answer to this because its algorithms are so good at predicting who will and who won’t repay their loans that who you lend to becomes far more important than whether or not a recession is coming. This would have the further advantage that banks using Upstart’s technology could carry on lending even if the face of recession which is just when many people could really use the help.

The fact is that most people don’t have pots of capital sitting around for many of life’s events, weddings, moving house, buying cars or going on holiday and loans have a huge role to play in helping people organise their lives. They desperately need a system for allocating loans to people who need them and would repay them and doing this at the most favourable possible rate of interest and that is exactly what Upstart is offering.

All credit to the banks who have jumped on board, especially Cross River Bank, which was the only bank working with Upstart for the first four years. People think the concentration with Cross River is a negative but if it wasn’t for them this wouldn’t be happening. Cross River’s share of loan volume has gone from 89pc in 2019 to 72pc in the first three quarters of 2020 and is surely less now as the number of banks using the platform has grown from 10 in 2020 to 25 or more currently.

Cross River remains a big supporter. In September 2021 Upstart launched a Spanish language version of Upstart’s loan application process for the 50m plus Americans who speak Spanish at home as their first language. Which bank is offering these Spanish language loans, Cross River. It is easy to imagine a lot of Spanish people turning to Upstart for their loans – not only do they get a better deal but they get to apply for it in their preferred language.

Another concentration risk is that a company called Credit Karma, refers almost half the loans going through the Upstart platform. Credit Karma was recently acquired by accounting software giant, Intuit, which introduces an element of uncertainty but it may well be that both sides are very happy with an arrangement showing such strong growth.

It is also not unusual to have this degree of concentration risk in the early days of a company’s growth. PayPal was hugely dependent on Ebay for years but not any more. Twilio was very dependent on Uber and then lost them as a customer but has still done brilliantly since. Early stage companies have to make do and mend; that is par for the course.

My guess is that banks don’t really want use Upstart. Nevertheless Girouard says he will be shocked if there are not hundreds of banks using the platform in a couple of years and eventually all credit will be allocated using AI. I guess it is the customers who will make this happen. Upstart is developing algorithms to predict who will and who won’t repay their loans. As more and more loans are made using the platform the computer learns to do this job of prediction better and better. Imagine if it was perfect. It would open the door to loans for millions of Americans who can’t get loans, often because they are younger, poorer, less asset rich or the wrong demographic. It would also help more affluent Americans pay less for their loans because they did not have to subsidise all the defaults. It would even improve the performance of the banks who could price their loans more accurately and make more of them. It’s a win win all around which makes it likely that it is going to happen. It is just the time scale that is hard to predict but judging by Upstart’s recent progress events are picking up speed.

Upstart shares have quickly become a byword for volatility. This is not a surprise if I am right about the massive initial undervaluation meeting a combination of a huge opportunity and rapidly accelerating growth. It is the perfect cocktail for some dramatic share price moves and so much profit in such a short period is bound to lead to bouts of profit-taking..

The real question for investors is where is Upstart on its investment journey. Like so many ebullient US CEOs, Girouard thinks the business is just getting going and he believes Upstart is on a course to become one of the world’s largest and most impactful fintech businesses. All you have to do is suppose he is right to justify buying the shares and he has been proved very right so far.

Upstart in 2021 looks to me more than a little like Microsoft in its early years. The latter had a vast opportunity. There was a permanent threat of competition and always great uncertainty about whether it would seize the opportunity. As we know with 20:20 hindsight it did and Microsoft had a phenomenal run between 1986 and 2000 with the price rising over 600-fold. It has had another phenomenal run since but that is another story.

I see traditional banks as like the Austro-Hungarian empire in the early years of the 20th century surrounded by hungry predators ready and waiting to eat them for breakfast. Upstart may be one of their best hopes for continuing to play a role.

I am still reading Upstart’s prospectus and have found another extraordinary statistic. In the eight years between the company being founded and the December 2020 prospectus 620,000 loans were made using Upstart’s platform. In June 2021 100,000 loans were made on the platform in one month alone. Is it any surprise that the shares have been racing higher.There is an opportunity for Upstart to really change peoples’ lives. According to the prospectus 10pc of Americans’ disposable income is spent servicing debt and 16pc of Americans spend 50-100pc or their disposable income servicing debt. Think what a difference it would make to these people to have a system which prices loans more accurately (i.e. more cheaply) and makes loans available to many people who are rejected under the existing approach.

Last but not least there is the exciting possibility of a tipping point in the acceptance of Upstart’s technology. Girouard has referred to this possibility in interviews and there is a reference to it in the prospectus where the McKinsey Global Institute is quoted as saying “AI will be slowly adopted in its early stages followed by steep acceleration as the technology matures and companies learn how best to deploy it” . Girouard then says: “We believe the lending industry will follow this path.”

Shares don’t climb in a straight line. Upstart shares rose strongly between December 2020 and March 2021. They then entered a period of extreme volatility and consolidated for the next four months before rising sharply again in two hectic months from $120 to over $300. It would not be surprising if they entered a new period of volatility/ consolidation but if I am right long term these shares are headed higher and news flow is likely to be positive or even extremely positive. You could even say it will have to be if the company is to go from where it is now to where Girouard thinks it is heading.

Just remember that miracles can happen in investment. Alphabet/ Google, floated at $40 in 2004 adjusted for a subsequent share split, has recently traded at a peak $2,925 and the business looks as full of energy and innovation as ever.

Here is another fun statistic to reference Upstart’s incredible growth. From April 2019 to March 2020 there were $118bn of personal loans made in the US. Over the same period $3.5bn of personal loans were originated on the Upstart platform or less than three per cent of the total. In June 2021, so in just one month, $1bn of personal loans were originated on the Upstart platform. If we assume no growth in the total market, which admittedly may be too cautious an assumption because personal loans are growing fast in the US, then Upstart originated loans are running at $12bn a year which is around 10pc of the market. They have tripled their market share in little more than a year.

Everything points to the fact that Upstart is doing something which really resonates with consumers and if that is right the banking industry is going to be forced to sit up and take notice.

One of the most important factors that can create shareholder value is the flywheel effect where companies get into a virtuous circle of improvement that creates an ever higher barrier to entry by would-be rivals. Upstart believes it has just such a barrier, sometimes referred to by US investors as a moat.

First is the machine learning effect. More loans means more data to process which makes the algorithms smarter which means they can make more loans at lower interest rates.This increases the number of borrowers using the platform. This, provides yet more data, which leads to better borrower selection, which lowers losses and leads to lower interest rates for borrowers which leads to more borrowers, more data, better borrower selection and on and on.

You could say this process is just beginning with the Spanish speaking demographic although in many respects they will be like any other Americans but if there is anything special the AI will pick it up. The algorithms are also just beginning to see the loans being made which will feed the whole flywheel effect for auto finance, which is a market six times the size of personal loans.

There is another factor at work with auto finance which is Upstart’s 2020 acquisition of Prodigy, a Shopify-style platform which is being rolled out to car dealers across America. A key part of the package will be to enable dealers to offer Upstart powered loans to car buyers, a market where the company says there are huge inefficiencies.

Upstart has said they plan to invest massively in Prodigy to expand its coverage and its r&d efforts. I have not been able to. confirm the figures but anecdotal reports suggest that Upstart already has over 1,000 employees. This compares with 554 when the number was last officially reported so would be an astonishing rate of growth and further proof of the company’s ambitious goals.

If they are hiring on such a scale they certainly have the money. Not only is the business profitable but they recently raised $661m in a convertible loan issue. This comes hard on the heels of a follow on offering at $120 to raise $276m in April and the $167.4m raised for the company in the December 2020 IPO.

What has not been mentioned above is that over 70pc of loans are approved automatically with no human intervention. You literally go on the platform, enter some details and receive a firm offer of a loan. It is that simple which also helps explain why repeat business from existing customers doubled in the latest quarter. Upstart is not just assembling an amazing data bank but also a hugely valuable roster of customers, who know and appreciate what they do.

There are so many mind-blowing statistics pointing to the growing scale of the business. In the whole of 2017 the group spent $33.8m on sales and marketing and $5.3m on engineering and product development. in the latest quarter to 30 June 2021 those numbers have increased to $75.9m for sales and marketing and $31.4m for engineering and product development.

Not only is the company growing fast but it is gearing up for massive investment to keep growing fast going forward. Things can often go wrong and we all know about Murphy’s law. Even so Upstart looks to me a phenomenally exciting investment. One of the most exciting I have encountered in many decades of hunting down exciting fast-growing companies.