Remember cogito ergo sum. We want our investment decisions to be determined by hard facts, not opinions.

Fact 1 – How strong is growth?

Revenue in the fourth quarter was $1,660,000,000, up 66% year over year, driven by continued technology advancements to our core mobile gaming business, seasonal strength, and the expanding impact of our e-commerce initiative. Adjusted EBITDA was $1,400,000,000, up 82% year over year, representing an 84% margin.

Fact 2 – Adam Foroughi had this to say on prospects.

From where we sit, we are still in the early innings of what this platform can be.

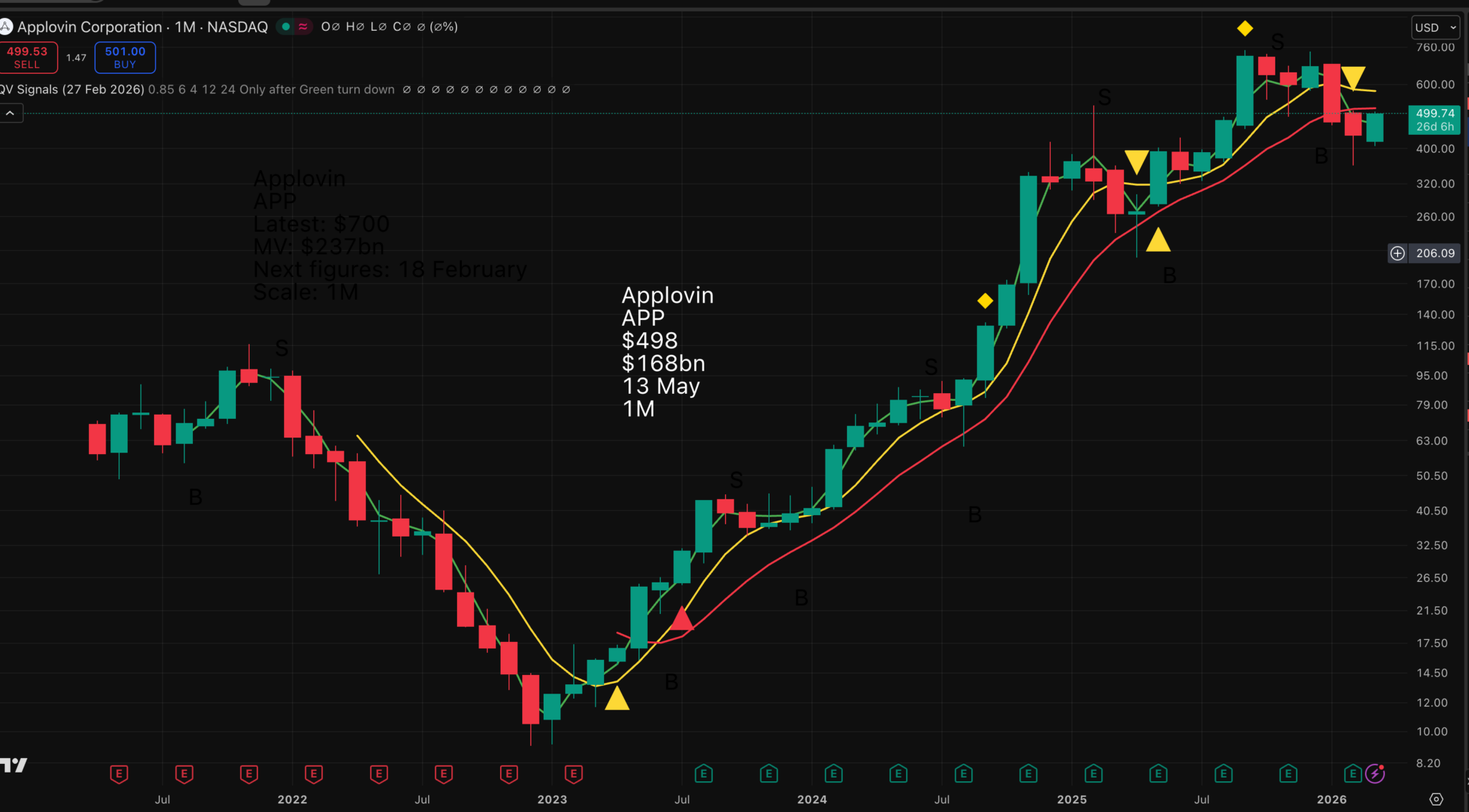

Fact 3 – The fundamentals are spectacular, so what about the chart? My idea is that we buy when the chart and fundamentals are pointing in the same direction. This is not happening yet, but it is close. It is super-tempting to buy now, and maybe why not, but support from a yellow line buy signal would be the final brick in the wall.

Fact 1 is strong growth.

And thank you everyone for joining us today. In our fiscal Q1 2026, total revenue reached $19.3 billion, up 29% year on year, and exceeding our guidance on the back of better than expected growth in AI semiconductors. This top line strength translated into exceptional profitability with Q1 consolidated adjusted EBITDA hitting a record $13.1 billion, which is 68% of revenue. These figures demonstrate that our scale continues to drive significant operating leverage. Now we expect this momentum to accelerate as our custom AI XPUs hit their next phase of deployment among our five customers. Looking ahead to next quarter, Q2 2026, we are guiding for consolidated revenue of approximately $22 billion, which represents 47% year on year growth.

Fact 2 is the story, which is awesome.

Let me now give you more color on our semiconductor business. In Q1, revenue was a record $12.5 billion as year on year growth accelerated to 52%. This robust growth was driven by AI semiconductor revenue, which grew 106% year on year to $8.4 billion, way above our outlook. In Q2, this momentum accelerates and we expect semiconductor revenue to be $14.8 billion, up 76% year on year. Driving this is AI revenue growth, which will accelerate very sharply to 140% year on year to $10.7 billion. Now our customer accelerator business grew 140% year on year in Q1. This momentum continues in Q2. The realm of custom AI accelerators across all our five customers is progressing very well.

Today, in fact, we have line of sight to achieve AI revenue from chips, just chips, in excess of $100 billion in 2027.

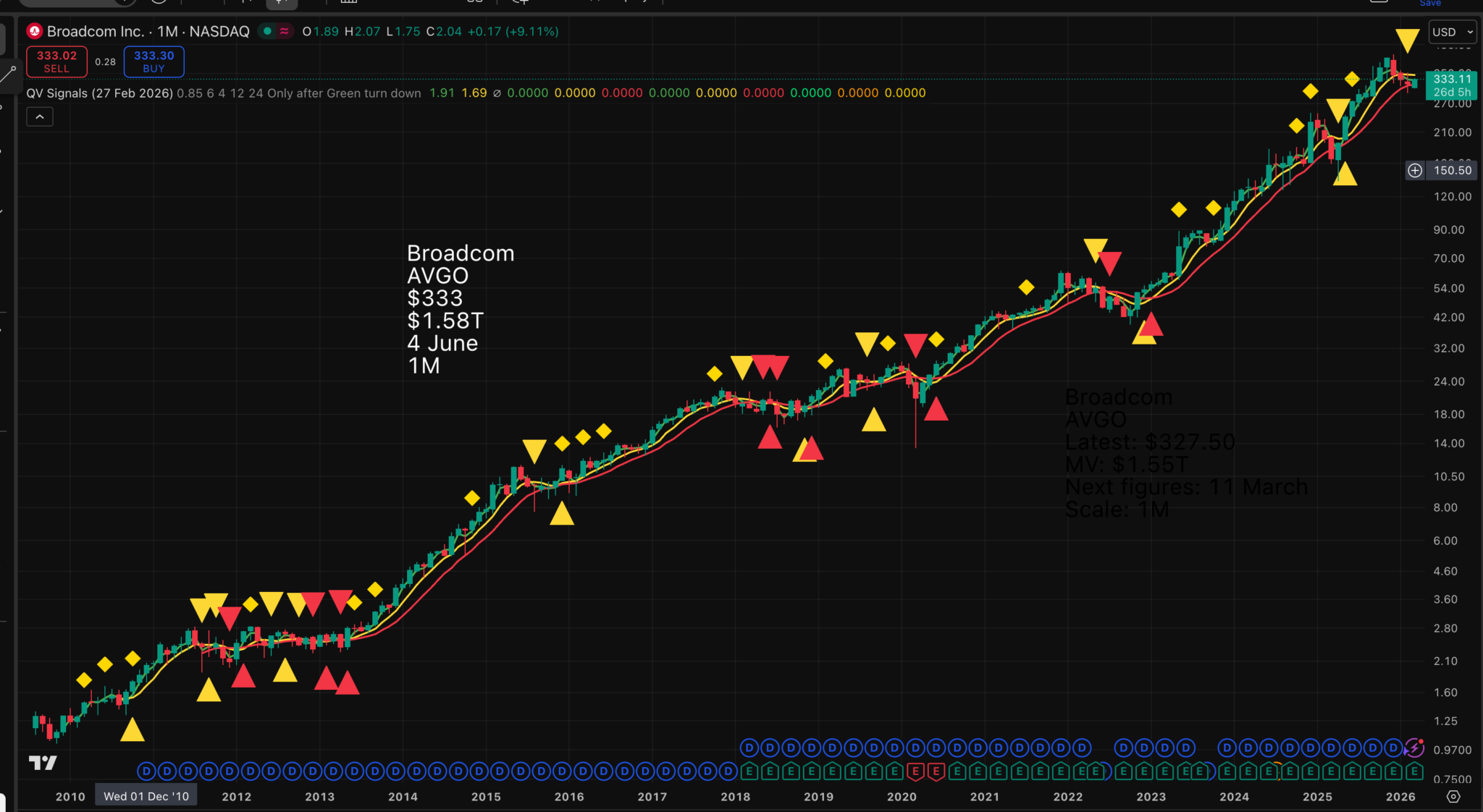

Fact 3 – So, what about the chart? The yellow line is falling after a recent sell signal, but it is more a question of flatlining. Broadcom shares would look like a strong buy on a yellow line buy signal. I will be alerted to this as soon as it happens.

Fact 1 is the blistering growth of Credo’s business.

In the third quarter, we delivered record revenue of $407,000,000, a sequential increase of 52% and more than 200% from Q3 last year. We delivered non-GAAP gross margin of 68.6% and generated approximately $209,000,000 of non-GAAP net income.

Fact 2 is the exciting story.

Over the past 18 to 24 months, maximizing network reliability and energy efficiency have been our core mandates as we have built our roadmap and brought new products to market. In AI infrastructure, performance without reliability stalls clusters, and scale without efficiency strains both economics and power envelopes. The strategy is clear: accelerate cluster bring-up, maximize XPU utilization, and reduce total cost of ownership, all while providing our customers the highest reliability in the industry. Our recent performance reflects the most accelerated growth phase in Credo Technology Group Holding Ltd history. From fiscal 2024 to fiscal 2025, we more than doubled revenue. And from fiscal 2025 to current year, fiscal 2026, we expect to triple revenue on top of that.

That represents greater than six times growth in just two years. Few companies, particularly in semiconductors, have scaled at that pace while maintaining consistent execution, healthy margins, and product leadership. Our purpose-built SerDes NICs, vertically integrated system model, and deep hyperscaler partnerships win at scale. We established leadership in high-reliability copper connectivity and built strong position in optical DSPs and retimers. Now our strategy is to lead in reliability, power and signal integrity across the full spectrum of AI and data center connectivity, from die-to-die links to chip-to-chip and board-level links, to rack- and row-scale copper, to mid-reach optical, and to resilient facility-wide optical solutions.

Fact 3 – So again, we look at the chart. The moving averages are bunching, which is a classic precursor to a significant move. In light of the glowing fundamentals, it seems unlikely this will go down, but that is what charts are for: to make us think the unthinkable if that happens. We need a yellow triangle buy signal. This may not guarantee success, but it bases our investment decisions firmly in logic and comes with a built-in exit strategy.

Strategy – Wait To See The Whites Of Their Eyes

This combination of spectacular, corporate optimism on the outlook near and far and charts which lack upside conviction is extraordinary. Investors are cagy, which means we must be cagy too. Get those buy signals in place, and we can start to act.

Keeping A Close Eye On Palantir

Reading The Tea Leaves In A Turbulent World

Red Line Investing And The Russell 1000 Index