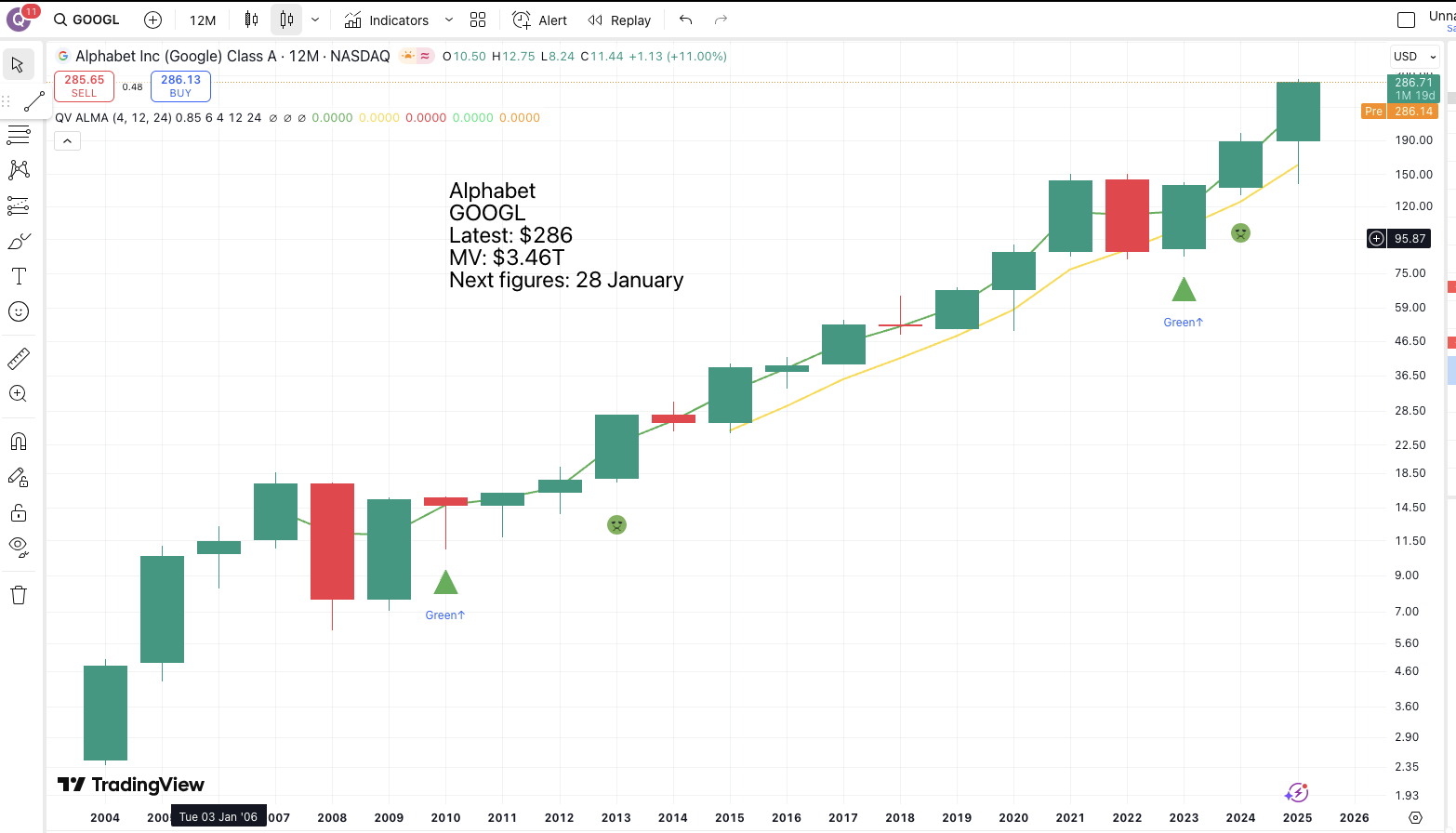

Alphabet floated on a valuation of around $80bn. It is presently worth $3.6 trillion, and both the chart and fundamentals look positive. It hasn’t always been plain sailing. In the early days, relatively modest sales made the business look severely overvalued to the value guys, the quarterly results sometimes disappointed, and there were periods like the financial crisis in 2008-09 when the background fundamentals became extremely negative.

Google/ Alphabet soldiered on as good companies do, and patient investors reaped massive rewards. Remember my last alert, where I noted that the most successful investors either forget they hold the stock or die. Google is a great example.

It has grown and grown, and the compounding effect of that is incredible. In 2003, let alone 2002, Google was a tiny business.

Google’s revenue for fiscal year 2003 was approximately $1.47 billion, with a profit of $105.6 million. This represented significant growth from the previous year, with revenue increasing by over 233%.

AI overview

Look at the company now.

In its most recently reported quarter, Google’s parent company, Alphabet, saw record revenue of approximately $102.3 billion, driven by strong performance in both its advertising and cloud businesses. The company’s net income was about $$35 billion, a 33% increase year-over-year. This surge in revenue is largely attributed to increasing demand for AI-powered infrastructure and data analytics services, as well as continued strength in its core advertising services.

AI Overview

Every statistic is amazing. Annualised sales are running at over $409bn, net income is running at $140bn, and the company is growing profits at 33pc year-over-year.

This is what drives the share price over time: a massive increase in the scale and power of the business. There have also been exciting developments. Search is unrecognisable from the early days; YouTube has proved to be one of the greatest acquisitions in corporate history, the cloud has been a massive driver of sales and profits, and now the company is using its scale and financial power to play a major part in the AI boom. Further down the road, initiatives like Quantum Computing and Waymo self-driving car technology may become new growth stars.

Remember, the 20 punch cards that were also mentioned in a recent alert. The trick to becoming a legendary investor is to make a significant investment in some great companies and hold forever.

The main reason why Google shares have climbed so massively, and that original investors hold 40 shares for every share they bought (thanks to subsequent splits), is that the business has been phenomenally successful.

This always looked like a strong possibility given the great starting fundamentals, so it didn’t take a rocket scientist to decide to use one of his punch card holes for Google. On the contrary, if in 2004, an investor had been looking for such a stock, Google would have been an obvious choice and commanded a high valuation accordingly.

The best investments are in companies which look most likely to become much bigger over time. You must expect their shares to be expensive. Cheapness is a massive red flag in the stock market. This is why I am not dismayed by the high valuations accorded to companies like Palantir. If it were a private company, like OpenAI, I would already be describing it as one of the world’s great businesses, likely to increase massively in size and value over time.

Buy the shares, perhaps buy more into weakness or over time, but otherwise pretend you have forgotten you own them or are dead. Less drastically, you could have a 20-punch card portfolio, and when you buy any share which punches a hole in the card, you can never sell.

Look for shares in companies where you believe in the man, the business, the performance and the tail winds driving the company’s growth. These are your one decision investments. They won’t all be successful, but even one winner can transform your life.

There is another important point about great growth shares. A company growing at five per cent a year is going to take forever to become a giant, but Google, in 2003, was growing sales by 233 per cent a year. Dramatic growth is a key characteristic of a major winner.

There is also something intangible, some special magic about the business. Nvidia has it, Palantir has it, Tesla has it, Broadcom has it, I am beginning to believe that ArgenxSE has it, and there are other companies like Credo Technology and RobinHood that are delivering the explosive growth, have the tailwinds and the visionary leadership that can take a business from small to gigantic.

There are others, not yet quoted, that may or arguably do fit the bill, companies like OpenAI, Anthropic, and Anduril. You guessed it. I am starting to think about not just my Top 50 but a portfolio where it is even harder to gain entry, a PunchCard Portfolio.

Value investors criticise Nvidia by saying that its shares are more valuable than all the bank stocks in the world. So sell Nvidia and buy all the bank stocks. Then sell that incredible Van Gogh on your walls and buy 10,000 lovely landscape paintings to decorate every inch of the walls of your houses. That would be madness. Exactly!

The best is priceless, which is why investors find it so hard to value Palantir. Analysts and professional investors are trained in share valuation, and Palantir smashes all their rules. Retail investors are ignorant of the rules but love the story, the romance, the magic and the passion of company founder and CEO, Alex Karp. And those are the characteristics of the biggest winners.

Share Recommendations

Alphabet. GOOGL

Nvidia. NVDA

Palantir. PLTR

Broadcom. AVGO

Tesla (TSLA)

ArgenxSE. ARGX

Credo Technology. CRDO

RobinHood. HOOD

OpenAI (private)

Anthropic. (private)

Anduril. (private)

Strategy – Play Dead

As I write, stock markets are in full-scale panic mode. One worry is a rather technical one about the rate at which companies depreciate the data centres in which they are investing so heavily. I guess that the assumptions companies are making about the useful life of data centres and GPU chips (namely that they will last quite a long time) will prove reasonable, and investors will calm down.

If it were easy to keep the faith with exciting investments, everybody would do it. It’s a challenge, and investors need to have faith. There are large profits to be taken, and investors become ultra twitchy when they see paper profits melting away.

I have no idea how much profit taking will happen or how badly stocks will correct, but I am sure that once the correction is done, prices will rebound. In 1974, there was a UK share called Electrocomponents, which had a successful business distributing electronic components. It is no longer quoted in its old form, so the precise records are gone, but this is what AI said.

In 1974, Electrocomponents shares were significantly affected by the severe 1973–1974 stock market crash, which was one of the worst global market downturns since the Great Depression. The United Kingdom market was particularly hard hit during this period.

Key factors contributing to the market environment in 1974 included:

The collapse of the Bretton Woods system.

The effects of the 1973 oil crisis, which caused high inflation.

A major recession in the 1970s.

All main stock indices of the G7 countries, including the UK, bottomed out between September and December 1974, losing at least 34% of their value in nominal terms and 43% in real (inflation-adjusted) terms from their peak. The UK market did not return to its previous level until May 1987, over a decade later.

While specific performance data for Electrocomponents shares in that exact year is not available in the provided snippets, its stock would have been subject to these pervasive, negative market forces that affected nearly all listed companies in the UK at that time.

AI overview, 12 November 2025

I remember they took a fearful hit, but when I looked at the underlying fundamentals, the business carried on as strongly as ever, just like Amazon in 2001 when its shares collapsed while business was booming.

Investors who stuck with their Electrocomponents and Amazon shares did brilliantly. Businesses do go wrong, but if you chicken out just because the shares are falling, you may miss great opportunities.