Five coronavirus winners (two from the portfolio and three newcomers)

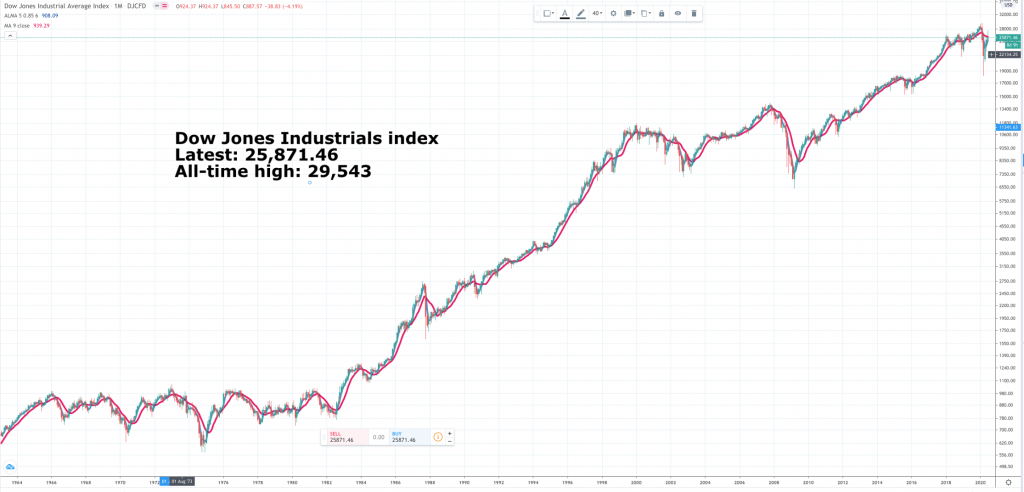

The Dow Jones is consolidating. Fears of a bubble are misplaced. It has rallied from the panic lows of mid-March but is still well off the highs, which seems like a reasonable response to the current set of circumstances. Virus cases are rising in some states and in some countries so the pandemic is still happening but countries in Europe and key cities like New York and London are well past the worst. My guess is that we are winning but it is a long haul process, which is another reason for liking shares in companies that help us deal with a stay-home economy.

The chart highlights key periods for equities. There was the long sideways between the late 1960s and 1982 as central banks fought inflation with high interest rates. Victory in that battle, falling interest rates and the dawn of the Internet era then fuelled a long bull market culminating in the dot com bubble in the late 1990s/ 2000. This was followed by another long consolidation punctuated with two ferocious bear markets in 2000-2003 and 2007-2009.

Since then there has been another long bull market which has seen the emergence of a group of technology-based collossi, stocks like the FAANGs, Facebook, Apple, Amazon, Netflix and Google (Alphabet). Not in the list because it doesn’t work alphabetically but part of the group is another tech behemoth, Microsoft and I am starting to add other names like Nvidia, Adobe, Paypal and Tesla with further names like Shopify and maybe one day even Zoom Video Communications knocking on the door.

Behind them is another group of exciting software as a service businesses, many of them in the QV portfolio, which are providing enterprise software from the cloud and driving a planet-wide digital transformation of the way businesses and corporations manage their activities. These are exciting times for investors as reflected in a tech-weighted Nasdaq 100 index, which has, justifiably in my view, reached a new peak even while the pandemic is still raging.

My expectation is that as the world gradually emerges from lock down, which is clearly a longer drawn out process than some initial hopes, that the Dow Jones and other less tech-weighted US indices will all reach new highs and enter a new bull market. Eventually even the UK and Europe may join the party although there is little sign of that happening to date.

1. Chegg/ CHGG Buy @ $67.81 MV: $8.4bn Employees: 1,401 Next figures due: 3 August

Business: “Chegg is the leading student-first interconnected learning platform, which is on-demand, adaptive, personalised, and backed up by a network of human help. It is the Smarter Way to Student and it is transforming the way millions of students learn by reconnecting the link between learning and earning through tools and services that support students throughout their educational journey. Our mission is simply to help students save time, save money, and get smarter in order to improve the overall return on educational investment.”

Key quote: “While many traditional companies are unfortunately being heard as a result, we believe the direct-to-consumer companies like Chegg that have digital and serve an essential need are experiencing increased levels of growth since the outbreak of the COVID-19 virus. Since mid-March, we have seen a mix shift in our business, as advertising revenue has decreased from an industry wide slowdown. While at the same time, we have also seen a substantial increase in our subscription services driven by new U.S. and international subscribers to our platform as well as increased success with our account sharing efforts, and we see these trends continuing into Q2. The first two months of the quarter started strong with subscriber growth at 33pc. And the acceleration of growth since mid-March added an additional two points in the quarter, increasing growth to 35pc. This continued acceleration is having a profound impact on Q2. As we now expect Q2 subscriber growth to be greater than 45pc.”

Comment: I was convinced that Chegg was already in the QV portfolio but not so. I put it in my hard copy publication, Quantum Leap, at $61 but not so far in QV. The worry investors have about Chegg, like other companies featured in this issue, is that once we do triumph over the virus and lock down ends that growth will slow at these businesses and their share prices will suffer. There is something in that view but I agree with Chegg that the virus has turbocharged a trend, which was already happening and will continue. I am very hopeful that Chegg will prove a long term winner. In the course of a discussion of education in an era of technology, Nathan Schultz, president of learning services at the company, noted “Chegg is now one of the premier online learning platforms with over 30m visitors coming to our site a year. We not only support these students in their academic journey but also, increasingly, into their professional endeavours.” I would say this business is riding a strong secular trend and is very much here to stay.

2. Fastly FSLY Buy @ $63.50 MV: $6.50bn Employees: 630 Next figures due: 6 August

Business: “As the consumption of online content continues to grow globally, organisations must keep up with complex and ever-evolving end-user requirements. We help them surpass their end-users’ expectations by powering fast, secure, and scalable digital experiences. With Fastly’s edge cloud platform, our customers are disrupting existing industries and creating new ones. Today, our platform handles hundreds of billions of internet requests a day.”

Key quote: “We delivered strong first quarter results with continued top line growth generating $63m in revenue, up 38pc year-over-year. We continue to see strong customer adoption of our edge cloud platform and security products by both new and existing customers across multiple verticals. Our enterprise customer count grew to 297, up from 288 last quarter, with average enterprise customer spend also increasing to $642,000, up from $607,000 in the previous quarter. This resulted in enterprise customers generating 88pc of our trailing 12-month total revenue, up from 87pc last quarter. Our existing customers are continuing to rely on us more as reflected in a consistently strong dollar based net expansion rate of 133pc. We also continued to demonstrate the stickiness of our platform as reflected in our new metric, net retention rate, which was a 130pc. Additionally, we are seeing the results from the investments that we made in 2019 in our demand generation, sales and marketing teams, which is also reflected in the increased total customer count of 1,837, up from 1,743 last quarter.”

Comment: I am not even going to pretend that I know what Fastly does, let alone how they do it. This is serious cutting edge technology, to coin a phrase. Importantly since February the company has a new CEO in Joshua Bixby, who was already a key player in the business. His promotion has allowed Fastly’s super-geek founder, Artur Bergman, to take on a role more suited to his skills as chief architect and executive chairperson, which sounds to me like he does what he likes and does best, focusing on the technology and leaves running the business to Bixby. The company has an important role to play in an increasingly online world and is doing well. “As social distancing measures increased over the March period, we continued to see increased traffic across the Internet and our platform.” It is also confident on prospects. “Fastly is the platform of choice for innovators. We are partnering with the most technologically advanced and creative companies, who we believe will not only weather the storm, but will continue to thrive in this environment. Companies are increasingly recognising the importance of digital transformation not only to survive during these uncertain times, but also for long-term success. As we are seeing this trend accelerate and evolve, we believe we are best positioned to partner and grow with these companies as they look for a trustworthy and modern platform.”

3. Pelaton PTON Buy @ $50.50 MV: $14.4bn Employees: 1,954 Next figures due: 27 August

Business: “Peloton Interactive makes money primarily by selling fitness equipment and via interactive sports content. The company was founded in 2012 by John Foley (CEO), Graham Stanton, Hisao Kushi, Tom Cortese, and Yony Feng. As of August 2019, it counts over 1.4m members on its platform with annual revenues of $915m. In its S1 filing, the firm calls itself “a technology, fitness, media, design, software, retail, product, apparel, experience, logistics company”. But above all, they are a “an innovation company transforming the lives of people around the world through our ever-evolving fitness platform”.

Key quote: “As you might imagine however, the shelter-in-place and work from home realities have created a meaningful tailwind for Peloton and a broader ongoing consumer shift toward that home fitness experiences. Specifically, we ended the quarter with over 886,000 Connected Fitness Subscribers, representing 94pc year-over-year growth. Member count is now over 2.6m inclusive of 176,000 Peloton Digital subscribers. Over the past year, we’ve seen steady gains in member engagement as we’ve expanded content verticals and launched new member experiences. With so many members now under stay at home orders, this quarter saw an even larger gain than expected. Our Connected Fitness Subscribers logged 44.2m workouts with us in the quarter up from 18.0m workouts in the same period last year, representing 145pc year-over-year growth. On a subscriber basis that is 17.7 average monthly workouts per Connected Fitness Subscriber compared to 13.9 workouts in the same period last year. With this growth the value proposition of our platform has never been stronger. This incredible engagement with our Connected Fitness products led to our lowest level of churn in four years. For the quarter, our average net monthly Connected Fitness churn was 0.46pc. In addition, we now have over 176,000 digital subscribers with growth attributed to improvements we have made to our fitness content and software features available on our digital app. Our price changed to $12.99 in December and the extension to new platforms like Amazon Fire TV. Early in the COVID crisis, we extended the digital subscription free trial period from 30 days to 90 days resulting in over 1.1m downloads of Peloton Digital in the past six weeks.”

Comment: Unlike Chegg, Peloton Interactive is in the QV portfolio at $45.11 and raises similar questions for investors. The stay-home economy has given a dramatic boost to growth but is this a flash in the pan that will fade as soon as lockdown ends. It now seems that lock down is going to be around to some degree for longer than we thought but I also feel that the virus boosted a trend that was already strongly in force as can be seen by the growth being delivered by Peloton before the crisis. The company is bursting with optimism. “Over the past several weeks, we believe we are accelerating our market share gains of the $600bn global fitness industry and increasing our lead as the largest and most scale connected fitness platform in the world. We believe the current environment of social distancing and working from home is permanently influencing consumer behaviour, driving more people to discover Peloton as the most engaging, entertaining, immersive, and motivating home platform for fitness and well-being.”

4. Teladoc Health TDOC Buy @ $201.50 MV: $15bn Employees: 2,400 Next figures due: 29 July

Business: “Teladoc Health, Inc., is a multinational telemedicine and virtual healthcare company based in the United States. Primary services include telehealth, medical opinions, AI and analytics, and licensable platform services. In particular, Teladoc Health uses telephone and videoconferencing software as well as mobile apps to provide on demand remote medical care. Billed as the first and largest telemedicine company in the United States, Teladoc Health was launched in 2002 and has acquired companies such as BetterHelp in 2015, BestDoctors in 2017, and Advance Medical in 2018.In 2019 it was active in 130 countries and served around 27m members.”

Key quote: “Teladoc Health reported strong revenue outperformance in the first quarter of 2020, driven by broad-based momentum across the business and a sharp acceleration in visit volume growth. Total revenue in the quarter grew 41pc over the prior year to approximately $181m. As a result of the increased demand for our services from clients and consumers, we are significantly raising forward guidance, including full-year revenue guidance of $800m to $825m, representing an increase of over $100m relative to our prior range. We are playing a critical role during the global outbreak of COVID-19 and has seen a significant increase in inquiries from both existing and new potential clients. Our clients are turning to us to expand our service offering to new populations and add new products during this time of need. Requests from new potential clients are increasing as the outbreak of COVID-19 has highlighted the value of access to a comprehensive virtual healthcare solution. During the first quarter alone, we onboarded over 6m new paid members in the US across government and commercial populations. And we anticipate onboarding an additional 6m to 7m new members during the second quarter, culminating in the strongest first half membership growth in company history.”

Comment: Teladoc looks to me very much like an idea whose time has come. “The remarkable growth across our platform has been enabled by the tremendous response on the part of our team members and physicians. We responded to the surgeon demand by rapidly expanding the capacity of our physician network, including the onboarding of thousands of new providers, more than doubling the number of licensed physicians in our network. The investments in capacity made during the month of March have positioned us to meet the increased demand from existing members, as well as the new members we are in the process of onboarding. Turning to visits, we crossed a new milestone as total visits exceeded 2m in the first quarter, representing growth of nearly 90pc as compared to the first quarter of 2019. This is particularly noteworthy as it comes just 12 months after crossing the 1m visit per quarter mark in the first quarter of last year. While the first two months of the year were strong, visit volume accelerated significantly throughout March and into April as shelter-in-place orders began, $0 copays were implemented and brick and mortar facilities closed. We were experiencing broad-based growth in visits across the portfolio as our diverse product offering has enabled us to step up and meet the varied healthcare needs of patients during the outbreak of COVID-19. While general medical visit growth has increased significantly, demand for specialist care, including behavioural health and dermatology has accelerated even faster, reflecting the diverse nature of the need for care during this challenging time.” It is important that ever more medical care can be delivered without in-person meetings and that will make a huge contribution to making medical care affordable in the future.

Wingstop Wing Buy @ $131.77 MV: $3.9bn Employees: 784 Next figures due: 30 July

Business: “Wingstop operates and franchises a global network of restaurants with the mission of serving the world FLAVOUR. With a menu of 11 bold, distinctive flavours of classic and boneless chicken wings, Wingstop is the destination for made-to-crave wings and sides. The group operates from 1400 plus restaurants worldwide.”

Key quote: “Our focus on simplicity, scratch recipes and a takeout orientation have served us well in this difficult time. We made the decision to close our domestic dining rooms and offer carryout and delivery only on 16 March, 2020 which represented approximately 80pc of our domestic sales prior to that time. As we shared in our business update on 7 April , we saw a slight acceleration in our domestic same-store sales during the last two weeks of the first quarter. The first four weeks of the second quarter were even stronger. Prior to the outbreak of COVID-19, digital sales consisted of just over 40pc of our sales. Since closing our dining rooms, digital and delivery orders now account for more than 65pc of our sales.We believe that the strategic investments that followed our strategy to build a world-class digital platform plus the rollout of national delivery in 2019 provided a strong foundation for us and have led to the success we have seen during this time. To quantify the impact, our domestic same-store sales growth exceeded 30pc for the first four weeks of the second quarter which is well beyond even our own expectations. Our brand partners, supplier partners led by our friends at Performance Food Group and our delivery partner, DoorDash, have not missed a beat with the substantial change in volume. We remain confident in the solid positioning of our brand and life during and after the COVID-19 pandemic.”

Comment: Wingstop went into the QV portfolio at $126.50 in May, initially fell as often happens but has subsequenty recovered strongly and with its overwhelming emphasis on takeaway, delivery and digital is ideally placed to prosper in a stay home environment. The company’s vision of becoming a top 10 global restaurant brand looks eminently achievable.

| When the first world war began popular belief was that it would all be over in weeks. Something similar happened with Covid-19 and like the war victory is taking much longer to achieve than first expected. This provides a strong tailwind to companies like those above which have seen their growth accelerate as a result of lockdown. However these are good companies that were doing well before the virus arrived and it seems likely that many of the effects of the virus will continue in a post-virus world. The shares are sensitive to virus related newsflow. Falling cases trigger profit-taking and vice versa but my guess is that longer-term all these shares will do well. We are clearly moving to a more online world and new technologies like 5G will only add to that process. |