It’s finally happening – my new web site, Quentinvest.com; take a look

I have two print publications, Quantum Leap and Chart Breakout. I have been publishing them for 36 years now and I have no plans to stop. If you subscribe to one of those or both you don’t have to do anything. They will keep coming through the post every month. However, like everybody else, I am slowly but surely going digital and I now have a new web site, Quentinvest.com, which is increasingly going to be at the heart of what I do.

There are two elements to Quentinvest.com – Quentinvest for Shares, which alerts on shares and is closely tied in with my personal investing (although so are QL and CB). I put my best ideas everwhere.

The advantage of QV for Shares is that it is not limited by a print format. It is better and I plan to make it better still. If you subscribe you will pretty much get everything, QV for Shares+QL+CB, albeit in a different format.

Also on the Quentinvest.com web site is another new venture of mine, Quentinvest for ETFs. I used to write about collective investments for The Investors Chronicle, way back in the day but writing about ETFs has been a revelation. They make sensational investments with an element of safety for your capital that is hard to achieve with individual share investments.

QV for ETFs is a separate service which costs £100 a year or £10 a month and it is totally worth the money.

Quentinvest for Shares, which has been running for over three years now in the format of emailed alerts to subscribers, costs £250 a year or £25 a month and again I think is super worth it.

But you can have both, the whole shebang, effectively everything I do, for £300 a year or £30 a month. If I found Quentinvest.com online published by somebody else I would subscribe like a shot and I don’t subscribe to things in a hurry. Of course, I reseach and write it and I am not renowned for my modesty but they are good, better than good. They are terrific!

And we live in terrific times for investors. I believe we are living through the greatest bull market in history, which is nowhere near finished. I believe there are a string of great technology businesses in the world which are among the greatest investments in history. And I believe there has never been a better time to be a long-term investor. Go for it!

Please note that there may be some glitches in the copy below as we move to a digital format.

Additions to live portfolio

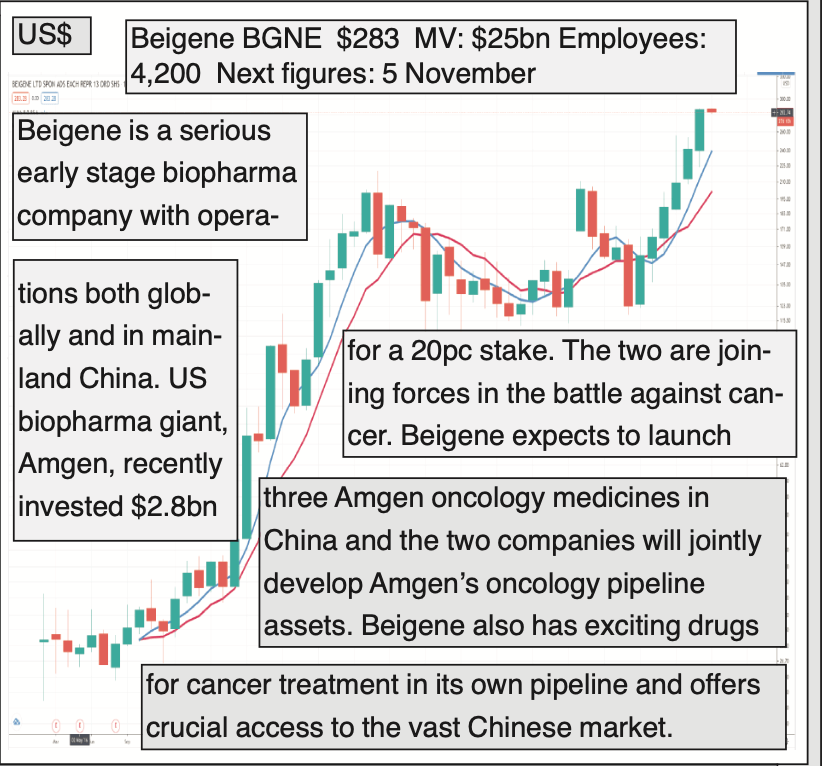

Beigene/ BGNE @ $283 (3) – “Our strategies for building a leading global innovative biotech company from China.” Beigene, 14 September 2020

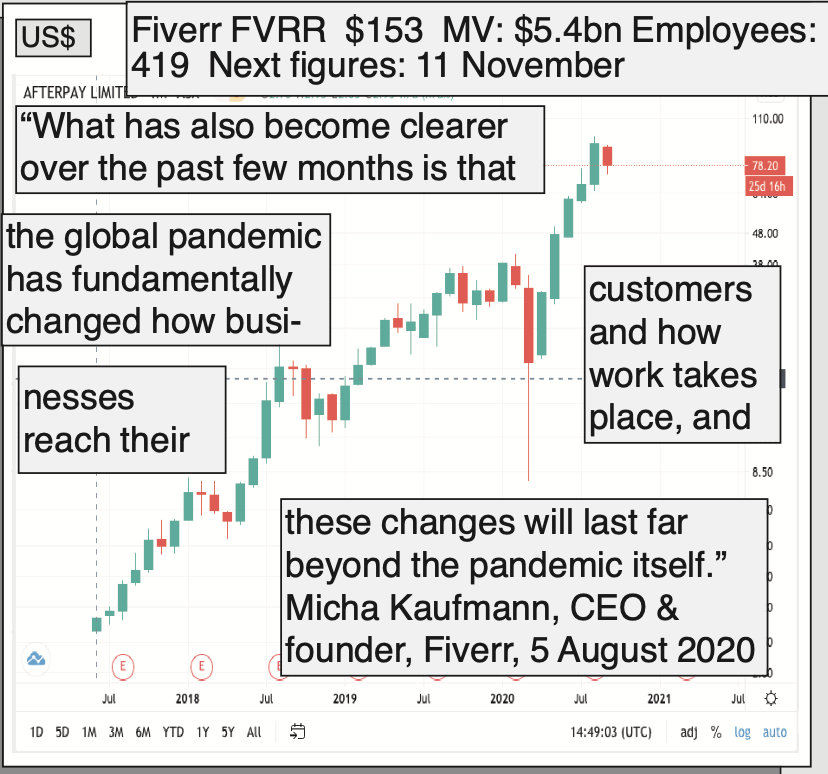

Fiverr/ FVRR @ $153 – “We have built our business from day one to promote remote work, to enable digital transformation, and to create a leveled playing field for every talent.” Fiverr, 5 August 2020

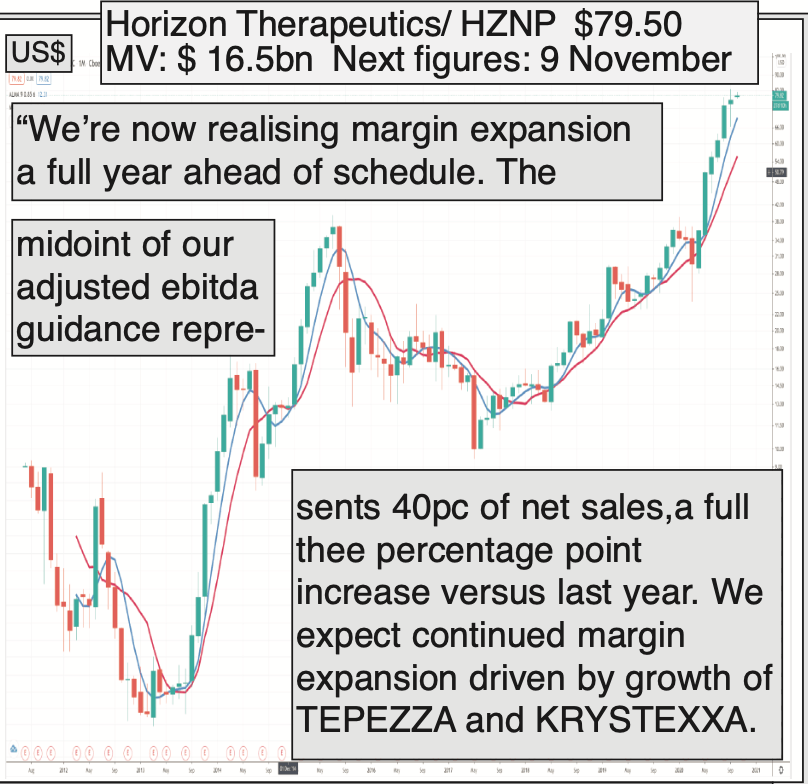

Horizon Ther/ HZNP @ $79.50 – “We delivered fantastic results this quarter, driven by the continued outperformance of TEPEZZA, our medicine we launched earlier this year for thyroid eye disease.” Tim Walbert, CEO, Horizon Ther., 5/8/20

Orsted @ DKK940/ £114 – “In January 2020, we were named the most sustainable company in the world.” Orsted

Peloton Interactive/ PTON @ $107 – “[We are] a media company that creates engaging-to-the-point-of-addictive original programming with the best instructors in the world. “ Peloton prospectus, September 2019

Solaredge/ SEDG @ $251 – “Or mission is to become the leading provider of intelligent inverter solutions across all solar PV market segments enabling the availability of cost-effective, clean renwable solar energy worldwide.” Solaredge Technologies, IPO, March 2015.

Square/ SQ @ $169 (5) – “Square is a bigger threat to banks than tech giants like Google and Amazon.” Forbes article, 8 June 2020

Twilio/ TWLO @ $290 (5) – “We are addressing a large and fast growing market.” Twilio, 1 October 2020

Beigene/ BGNE @ $283 (3)

(There is not a story to accompany the above chart but it is still a full-on recommendation.)

Fiverr Int./ FVRR Buy @ $153

Covid-19 lockdown puts a rocket under growth at platform for freelancers, Fiverr International

Fiverr was founded by Micha Kaufman and Shai Wininger, and launched in February 2010. The founders came up with the concept of a marketplace that would provide a two sided platform for people to buy and sell a variety of digital services typically offered by freelance contractors. such as writing, translation and graphic design. Fiverr’s services start at US$5, and can go up to thousands of dollars with gig extras. Each service offered is called a “gig”

Fiverr provides a platform for freelancers to find work and enterprises of all sizes to find the expert assistance they need. The business was tailormade for global lockdowns and has exploded as a result of Covid-19.

“As a company whose vision for the past 10 years was a future built around a remote and flexible workforce, today that vision has become closer than ever to reality. Since COVID-19 forced the entire world into social and economic lockdown, every aspect of businesses and work has been upended. Remote work and digital transformation are no longer options, but necessities to survive and thrive. Fiverr’s platform has become an important place for businesses to turn to in order to find experienced support and solutions, and where talent has turned to look for opportunities and income.”

What has made investors even more excited is that Fiverr clearly intends to use its platform to expand and play an even more ambitious role in the fast-changing world of work and do this on a global scale.

The company has also taken the opportunity of a soaring share price to strengthen its resource base. It recently raised $130m through an equity issue. This should help it take advantage of the favourable backdrop.

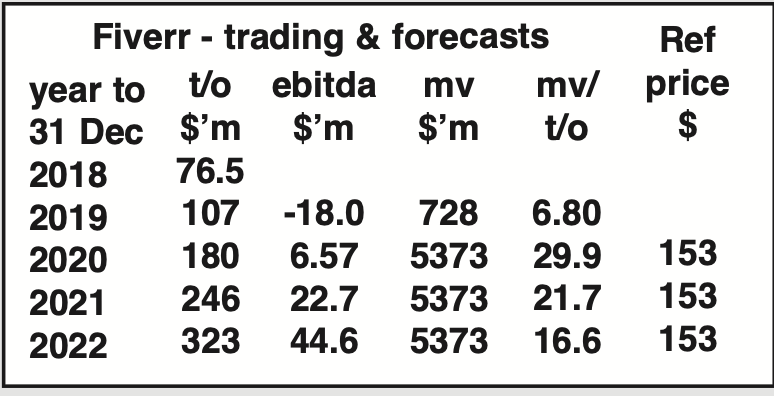

Fiverr grows by increasing both the number of buyers on the platfrom and hw much they spend. Between 2017 and 2018 buyers grew from 1.8m to 2m but their spend climbed from $119 to $145.

In the 12 months to 30 June 2020 active buyers grew 28pc to 2.8m with over 300,000 joining during the quarter. Spend per buyer jumped 18pc to $184 and high spend buyers, over $500, grew to 55pc of the total.

“On the seller side, not only is Fiverr an important channel for freelancers and individual talent, but we will also become partners and distribution channels for agencies, consultancies and other service providers. With this in mind, we launched Fiverr Business in Beta – a dedicated environment for businesses and teams to transact and collaborate on Fiverr. This is going to be a long-term investment for us and we are just at the very beginning. Second, we are building a global brand with a global footprint, global share of voice and a global business. Our investments in localization and into non-English websites have proved to be very timely. It is more apparent than ever that the need for remote work and digital transformation is global and that the potential market outside of English speaking countries is huge. Second, we are building a global brand with a global footprint, global share of voice and a global business. Our investments in localization and into non-English websites have proved to be very timely. It is more apparent than ever that the need for remote work and digital transformation is global and that the potential market outside of English speaking countries is huge.” Micha Kaufmann, CEO & founder, 5 August 2020

“The past few months have been one of the most productive and rewarding times in our company’s history. The strategies that we have put in place and our strong execution during the global pandemic is what has allowed us to achieve such an outstanding quarterly performance, with revenue growing 82pc year over year to reach $47.1m. This is the strongest quarterly growth we have had since 2012, and over $10m or nearly 30pc above the top end of our guidance. With this stronger than anticipated top-line growth, we also achieved EBITDA profitability two years ahead of our expectation at the IPO, and many quarters ahead of our expectations as communicated just a few months ago. While it is incredibly satisfying to see our business accelerate, it is equally rewarding to know that our success is a direct result of the success of our community. More and more businesses are transforming to digital-first using Fiverr, and more and more freelancers are provided with opportunities to generate income. It is an incredible privilege to be able to be there for our community in these challenging times.” Micha Kaufmann, founder and CEO, 5 August 2020

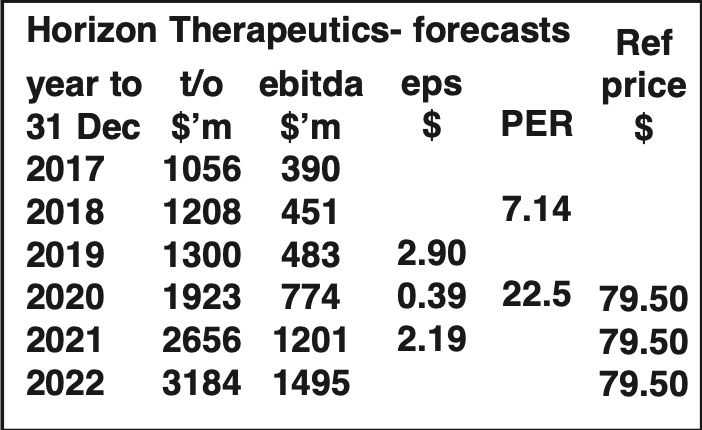

Horizon Therapeutics/ HZNP Buy @ $79.50

Horizon smashes expectations as demand for eye treatment drug, TEPEZZA, explodes

Horizon Therapeutics is a biopharma company focused on developing medicines for rare diseases. It is based in Dublin with offices in the US and Germany. Unlike many early stage biopharmas the group is both highly profitable and is focused on launch preparations for its breakthrough bilogic medicine, TEPEZZA, for thyroid eye disease. Strong growth means the group is moving into larger offices in both Dublin and the USA.

Horizon Therapeutics is a biopharma on fire.

“We delivered fantastic results this quarter, driven by the continued outperformance of TEPEZZA, our medicine we launched earlier this year for Thyroid Eye Disease or TED.

We continue to hear from our stakeholders that TEPEZZA is meeting a significant and critical need for so many patients who’ve gone years without any FDA-approved options to treat this painful and vision-threatening, rare autoimmune disease.

Based on the significant TEPEZZA demand, we are increasing our full year 2020 TEPEZZA net sales guidance to more than $650m, a substantial increase in the guidance of more than $200m we announced last quarter. Additionally, based on the faster uptick we are seeing for the medicine as well as its broad indication, we’re raising our TEPEZZA peak U.S. annual net sales estimate to more than $3bn.

Driven by TEPEZZA, we’re also increasing our 2020 total company net sales guidance by more than 30pc to $1.85bn to $1.9bn. We’re also raising our adjusted EBITDA guidance by approximately 60pc to $725m to $775m. For perspective, our updated 2020 guidance is now in line with what sell-side analysts expect for net sales and adjusted EBITDA next year in 2021.

We’re now realizing margin expansion of full year ahead of schedule. The midpoint of our adjusted EBITDA guidance represents 40pc of net sales, a full three percentage point increase versus last year. We expect continued margin expansion over the next several years, driven by the continued growth of TEPEZZA and KRYSTEXXA. Our success is a testament to the value of our unique biopharma model where the cash flow we have generated from our legacy business allowed us to significantly invest first in the relaunch of KRYSTEXXA, and the success of KRYSTEXXA has allowed us to optimally invest in the launch of TEPEZZA.

The continued strong performance of both KRYSTEXXA and TEPEZZA will provide us with the cash to build our clinical development pipeline to generate growth in the years ahead.”

The above says it all. Horizon is one of the most exciting early stage biopharma companies in the world.

“We strive to help as many people as possible impacted by rare and rheumatic diseases. Last year, we provided our medicines to more patients than ever before: roughly 4,000 patients received treatment

with KRYSTEXXA® and it passed the $340 million net sales mark, which is truly remarkable growth for a medicine nine years post-FDA approval. More than 1,000 patients received treatment with RAVICTI®, PROCYSBI® and ACTIMMUNE® combined, and more than 500,000 people living with osteoarthritis and rheumatoid arthritis were treated with our inflammation medicines. In January 2020, the FDA approved TEPEZZA for the treatment of TED, which is a serious, progressive and vision-threatening, rare autoimmune disease. TEPEZZA is the first and only FDA-approved medicine for the treatment of TED. At the time of approval, which was nearly two months before the target action date, the FDA said that “this treatment has the potential to alter the course of this disease.” As we look to the future, we have a tremendous opportunity to help thousands more people who are living with this devastating disease.”

“As a result of our continued growth, we announced that we are moving our global corporate headquarters to a much larger space at 70 St. Stephen’s Green, which is one of the most visible and central locations in Dublin, Ireland. The new office was designed with sustainability in mind, making it compliant with near-zero emission building standards. We also opened a 20,000-square-foot facility in South San Francisco, featuring office and laboratory space to enable formulation and process development for manufacturing, as well as bioanalytical method development and other R&D functions. And in early 2020, we announced we are moving our U.S. headquarters to a 74-acre campus with more than 650,000 square feet of office space in Deerfield, Ill.”

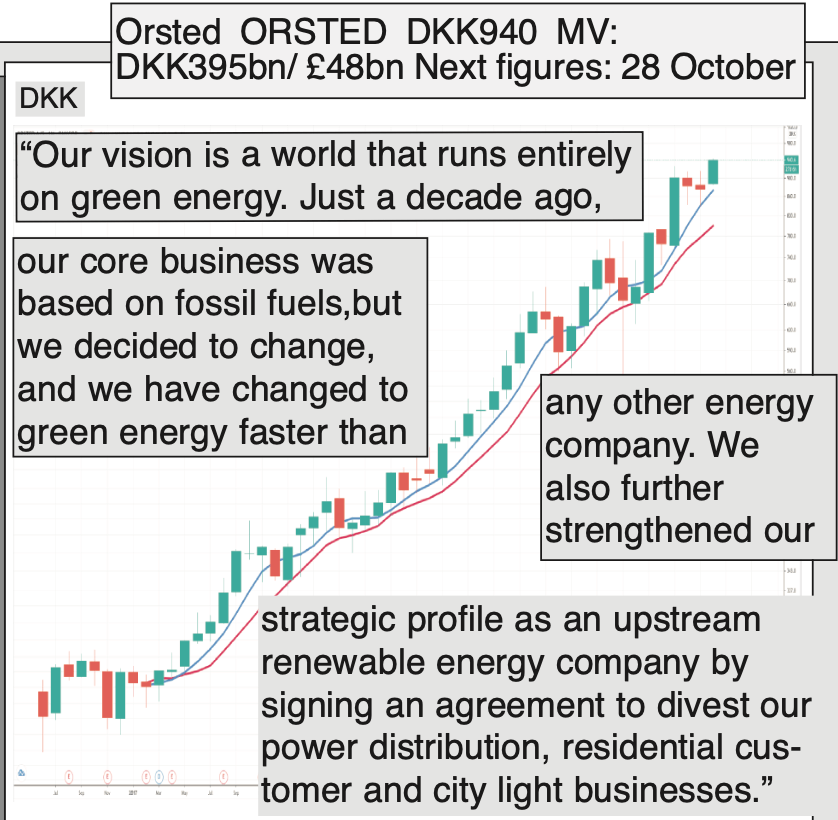

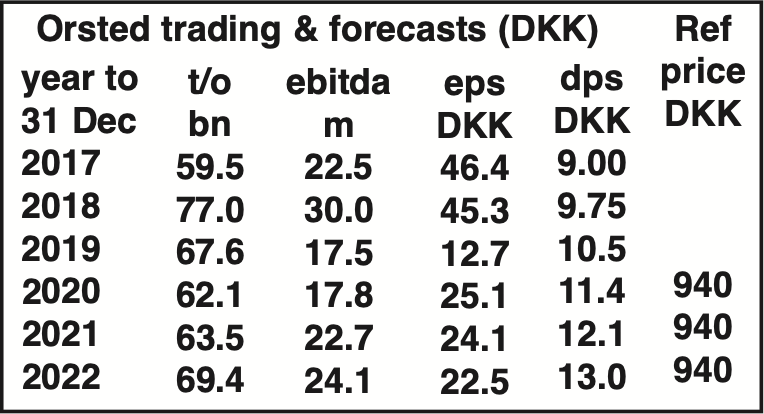

Orsted Buy @ DKK940/ £114

Danish sustainable energy superstar, Orsted, expands at pace to save us from fossil fuels

In 2017, DONG Energy decommisioned the world’s first offshore wind farm, decided to phase-out the use of coal for power generation and sold off its oil and gas business for US$1.bn. After selling its oil and gas business the company announced its intention to transition to renewable energy and change its name to Ørsted after the Danish scientist Hans Christian Ørsted. In 2018 Ørsted acquired Deepwater Wind to expand offshore wind in the US.

Orsted is a former state owned Danish fossil fuel and utility business, which has completely reinvented itself as a downstream renewables energy business. {Downstream means it actually produces energy as opposed to upstream which is distribution, making chemicals – in the oil business – and so on].

The company has won the accolade of being “the most sustainable company in the world”, which has no doubt attracted many investors keen to display their green credentials.

But it does look well deserved. Orsted is doing its utmost to move the wheel when it comes to saving the world from a climate disaster.

“In the beginning of July, we signed the world’s largest renewables energy corporate power purchase agreement with Taiwan-based TSMC for the 920 megawatt Greater Changhua 2b and 4 in Taiwan. I’ll come back to this groundbreaking corporate PPA shortly. In Taiwan, we are currently in the process of farming down the Greater Changhua 1 project. The transaction is progressing according to plan, and we still expect to sign this year and close the deal during first half of 2021. In addition, we are exploring the potential opportunities to farm down the Dutch Parcel-A [ph] 1 and 2 project. We continue to see very strong demand for our offshore wind projects among investors looking for de-risked stable returns, and if a farmed down crane can create additional value for Orsted, we will pursue it.”

And that is just in Taiwan. The company is pushing ahead with exciting renewables projects all over the place.

“In June, we commissioned our 230 megawatt onshore wind farm Plum Creek in Nebraska ahead of schedule and on budget, and we received the tax equity funding from our partners. The completion of the project brings our operational onshore capacity to 1.6 gigawatt, and one step closer to our ambition of five gigawatt installed onshore wind and solar PV capacity by2025.”

It is doing much more.

“In July, we acquired the 227 megawatt solar PV project Muscle Shoals located in Alabama. The project is currently under construction and is expected to be completed in third quarter 2021, where it will be the largest solar energy asset in the U.S. Southeast. The project is eligible for 30pc ITC, and has a fully contracted 20-year utility PPA. The acquisition of Muscle Shoals will establish an anchor position for Orsted onshore in the U.S. Southeast, a market which in the coming years is expected to realise the largest growth in solar installations in the U.S.”

The group is also active in the fledgling market for hydrogen generated power, where Europe hopes to become a global front runner.

It is hard to evaluate Orsted as an investment but there is something of the feeling of Tesla about the business. It could be exciting.

“We are very pleased with our strategic progress and results in 2019. Ørsted maintains a leading position in the global high growth market for green energy. We are well on track to deliver on our financial targets of 20pc average growth in profits from operating renewable assets for the period 2017-2023 and an average group ROCE [return on capital employed] of 10pc for the period 2019-2025.”

“In 2019, we achieved a global breakthrough outside Europe by initiating construction of our first large-scale offshore wind project in Taiwan, by winning two large scale projects and expanding our portfolio in the US, and by taking the decision to fully integrate Lincoln Clean Energy into Ørsted. Our deployment of renewable energy now spans markets on three continents. We bring more than 25 years of experience in renewable energy on-time and on-budget delivery of large infrastructure projects as well as new approaches and innovative solutions that can help decarbonise societies. Recently, we have set up a hydrogen team to explore how to transform renewable power from offshore wind into hydrogen and other green fuels to be used in the chemicals industry and as green fuels in hard-to-abate sectors, such as heavy transport and logistics.”

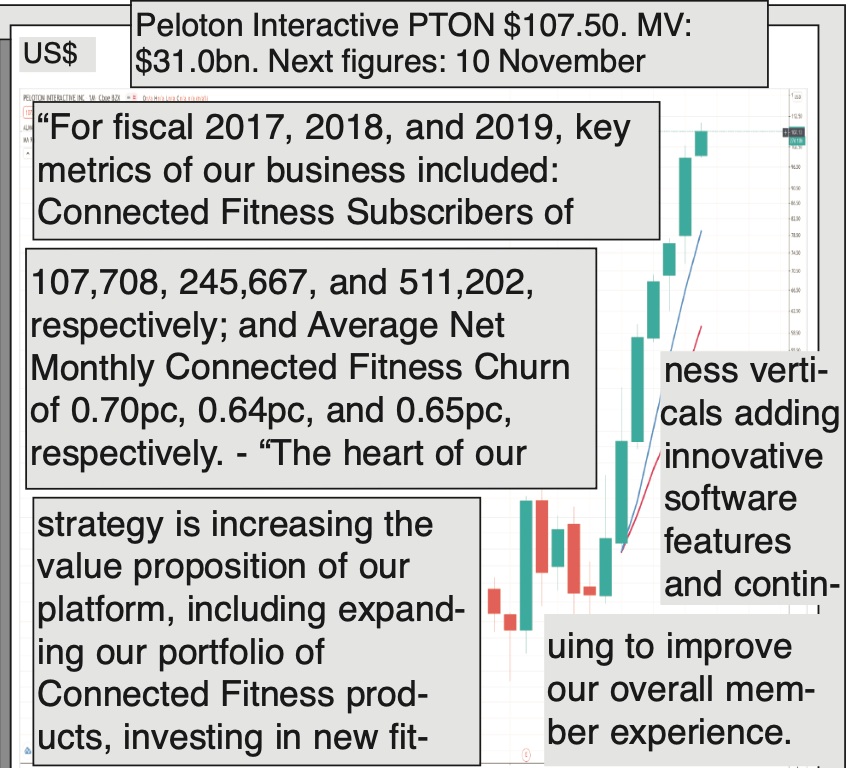

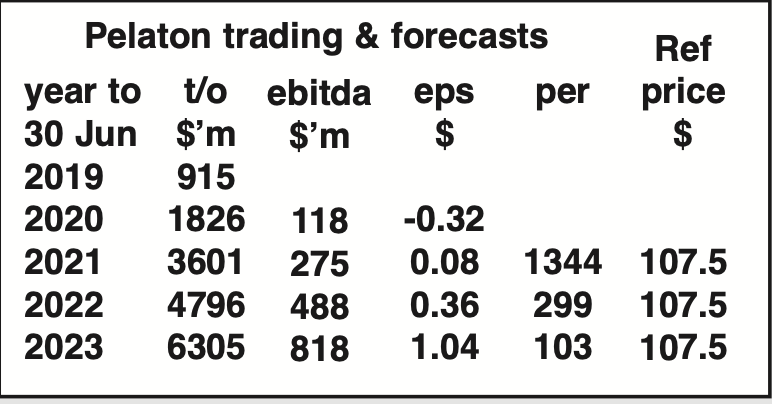

Pelaton/ PTON Buy @ $107.50

Low churn/ high subscription growth makes Peloton Interactive a super-fit stock

Peloton is an American exercise equipment and media company that was founded in 2012 and launched with help from a Kickstarter funding campaign in 2013. The company is based in New York. Its main products include a stationary bicycle and treadmill that allow users to remotely participate in classes that are streamed from the company’s fitness studio and are paid for through a monthly subscription service.

Peloton has a huge opportunity.

“We consider our market opportunity in terms of a Total Addressable Market, or TAM, which we believe is the market we can reach over the long-term in our current and announced markets, and a Serviceable Addressable Market, or SAM, which we address with our current product verticals and price points.

According to our research, our TAM is 67m households, of which 45m are in the USA. Within our TAM, we estimate that 52m households are interested in learning more about our Connected Fitness Products without seeing the price. We estimate that our SAM is 14m Connected Fitness Products, with 12m in the USA.

Historically, our SAM has grown as our brand awareness has increased. With low brand awareness in our current international markets, we believe we will see SAM expand as we make further investments in building brand and product awareness in these regions.

We will grow both TAM and SAM as we expand beyond our current geographies and grow SAM as we develop new Connected Fitness Products and content in new fitness verticals.

With approximately 577,000 Connected Fitness Products sold globally as of 30 June , 2019, we are approximately 4pc penetrated in our SAM of 14m.”

Thanks to Covid-19 fitness at home rather than in gyms is exploding as evidenced by this statistic from the recently reported Q4 2020 results

“My favorite KPI [key performance indicator] is workouts represented by our Connected Fitness subscriptions. In the fourth quarter workouts reached 76.8m, up 333pc year-over-year equating to nearly 25 average workouts per Connected Fitness Subscription per month, compared to 12.0 workouts per subscription per month in the fourth quarter of last year.”

This is an exciting business.

”Our compelling financial profile is characterized by high growth, strong retention, recurring revenue, margin expansion, and efficient customer acquisition. Our low Average Net Monthly Connected Fitness Churn, together with our high Subscription Contribution Margin, generates attractive Connected Fitness Subscriber Lifetime Value. When we acquire new Connected Fitness Subscribers, we are able to offset our customer acquisition costs with the gross profit earned on our Connected Fitness Products. This allows for rapid payback of our sales and marketing investments and results in a robust unit economic model.”

“Peloton is the largest interactive fitness platform in the world with a loyal community of over 1.4 million Members. We pioneered connected, technology-enabled fitness, and the streaming of immersive, instructor-led boutique classes to our Members anytime, anywhere. We make fitness entertaining, approachable, effective, and convenient, while fostering social connections that encourage our Members to be the best versions of themselves. We define a Member as any individual who has a Peloton account. We are an innovation company at the nexus of fitness, technology, and media. We have disrupted the fitness industry by developing a first-of-its-kind subscription platform that seamlessly combines the best equipment, proprietary networked software, and world-class streaming digital fitness and wellness content, creating a product that our Members love. Our highly compelling offering helped our Members complete over 58 million Peloton workouts in fiscal 2019. Driven by our Members-first mindset, we built a vertically integrated platform that ensures a best-in-class, end-to-end experience. We have a direct-to-consumer multi-channel sales platform, including 74 showrooms with knowledgeable sales specialists, a high-touch delivery service, and helpful Member support teams. Our Members are as devoted to us as we are to them—92% of our interactive fitness equipment ever sold, which we refer to as our Connected Fitness Products, still had an active Connected Fitness Subscription attached as of June 30, 2019.”

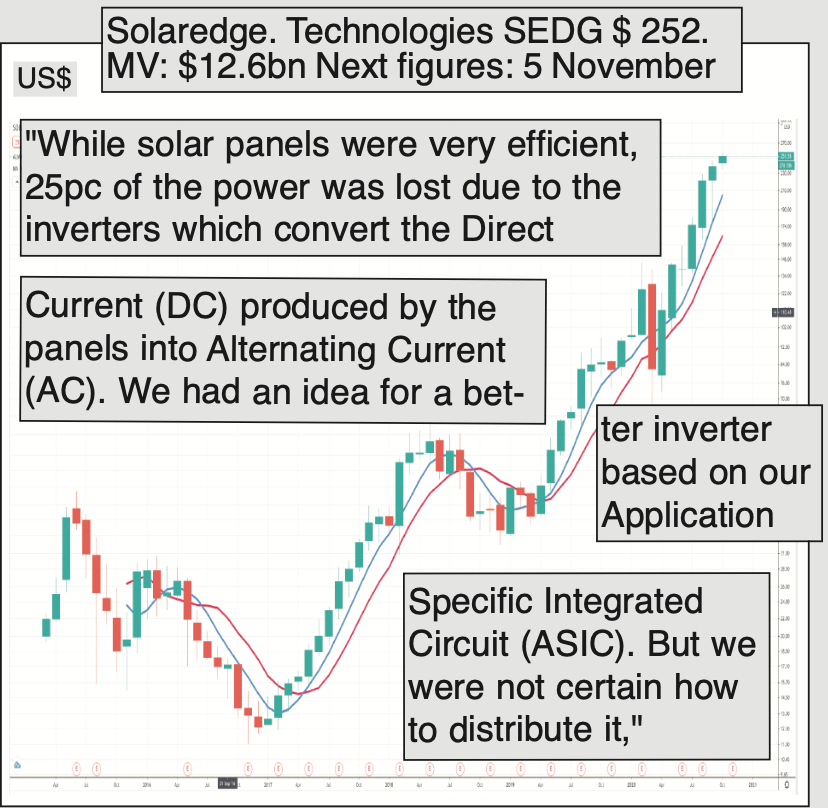

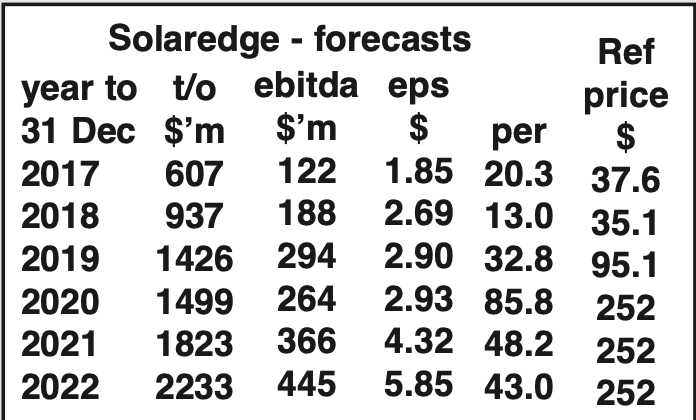

SolarEdge Technologies Buy @ $252

Israeli/ American SolarEdge on a mission to make solar energy & windpower more efficient

SolarEdge is an American-Israeli provider of power optimizer, solar inverter and monitoring systems for photovoltaic arrays.These products aim to increase energy output through module-level Maximum Power Point Tracking. Established in 2006, the company has offices in the US, Germany, Italy, Japan, and Israel. In 2009, the company started mass production of its products by electronic manufacturing services provider Flextronics International.

SolarEdge Technologies is a classic example of a company, which is doing well from making a better mousetrap.

It has two principal products, power optimisers and inverters. These are used to make renewable energy more efficient, whether that is from solar cells or wind power systems.

The company measures how it is doing by looking at the number of power optimisers and inverters sold.

The virus briefly stopped the company in its tracks as reflected in the table below, where sales growth is forecast to slow dramatically in calendar 2020 with ebitda (earnings before interest, tax, depreciation and amortisation) actually falling.

But growth s already recovering, especially outside the US and the overall picture is of a business growing very rapidly indeed.

In the IPO the company lists inverters shipped as growing from 30,140 in 2012 to 61,999 in 2014 and power optimisers shipped as growing from 709,804 to 1,357,251.

BY the time of the 2019 annual report these numbers had exploded. The three year sequence for inverters shipped to 2019 was 317,288, 455,793 and 665,520 and for power optimisers it was 7.37m, 11.4m and 15.8m. The growth is spectacular.

At the same time the technology is changing almost as rapidly. I don’t really understand what inverters and power optimisers do (let the SolarEdge brainiacs do that) but I have just watched a video saying that inverter technology is only now moving into the digital age similar to the shift in TVs from clunky boxes to flat screens.

Another thing that is exciting about Soaredge as an investment is that the company could hardly be more in tune with the zeitgeist. We need to save the planet. The whole business of this company is helping us to do that as cost-effectively and efficiently as possible.

In this respect they have a great deal in common with Tesla so no surprise that the two companies are collaborating to provide inverter solutions that work with Tesla’s home battery solutions.

A tragedy for the company is that founder and CEO, Guy Sella, died from cancer in 2019 at 54. He has obviously left a hole but also a company that has a clear mission and increasingly the resources and technology to realise it.

“Herziliya Petuach, Israel-based solar power electronics maker SolarEdge Technologies has a powerful growth trajectory — revenues have risen at a 46pc annual rate to $607m in 2017 and are forecast to pratically quadruple from those levels by 2022. SolarEdge’s technologies make solar systems produce more electricity. Specifically, its “direct-current optimised inverter systems — which consist of power optimizers, inverters, and cloud-based monitoring platforms — maximize power generation at the individual solar module level.” SolarEdge sells into the residential, commercial and small-utility solar installation markets by partnering with “large installers and engineering, procurement and construction firms, and indirectly to a multitude of smaller solar installers through distributors and electrical equipment wholesalers.”

“ We have invented an intelligent inverter solution that has changed the way power is harvested and managed in a solar photovoltaic (“PV”) system. Our direct current (“DC”) optimized inverter system maximizes power generation at the individual PV module level while lowering the cost of energy produced by the solar PV system and providing comprehensive and advanced safety features. Our system consists of our power optimizers, inverters and cloud-based monitoring platform and addresses a broad range of solar market segments, from residential solar installations to commercial and small utility-scale solar installations. Since we began commercial shipments in 2010, we have shipped approximately 1.2 gigawatts (“GW”) of our DC optimized inverter systems and our products have been installed in solar PV systems in 73 countries.” Extract from IPO document, March 2015.

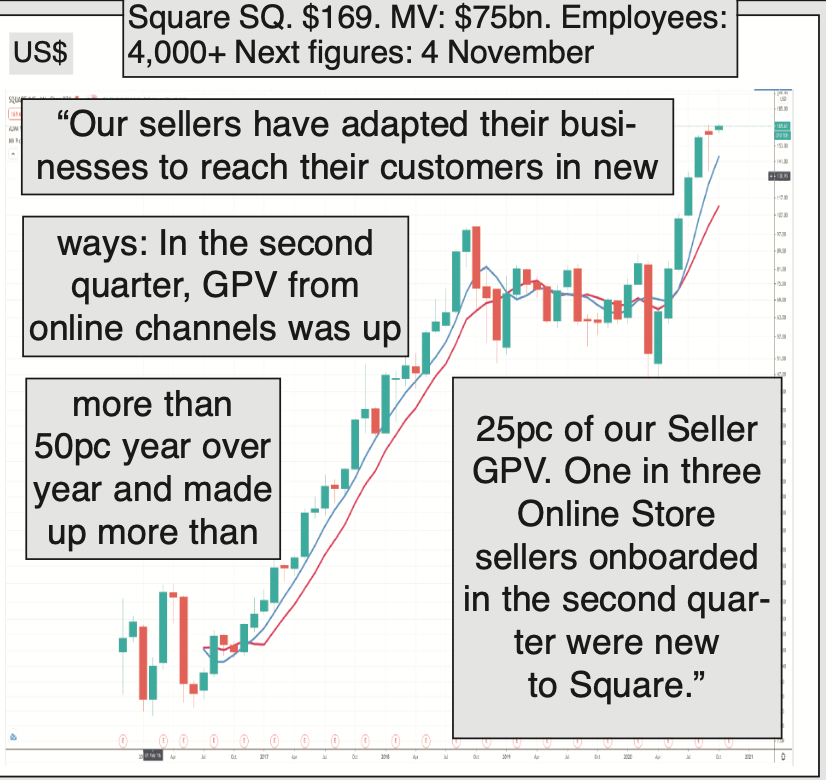

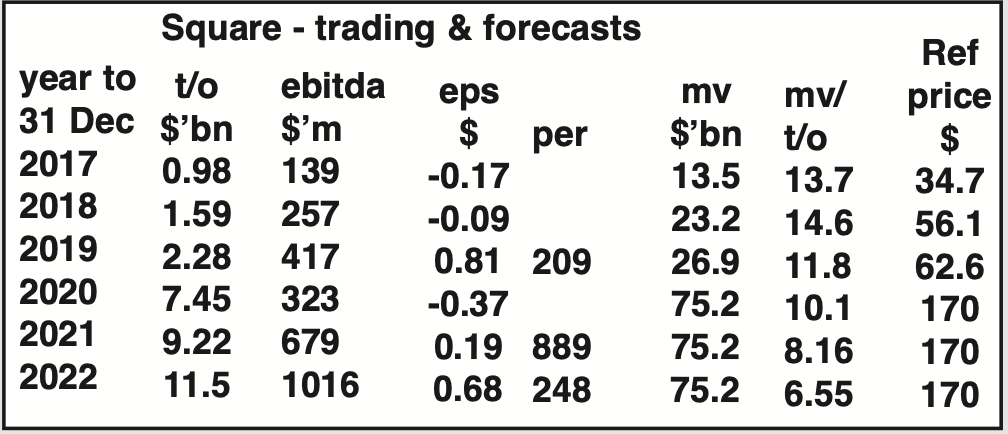

Square/ SQ Buy @ $169 (update-5)

Square rockets through lockdown as its Cash App business delivers 167pc growth

Square, Inc. is an American financial services, merchant services aggregator, and mobile payment company based in San Francisco, California. The company markets software and hardware payments products and has expanded into small business services. The company was founded in 2009 by Jack Dorsey and Jim McKelvey and launched its first app and service in 2010. It has been traded as a public company on the NYSE since November 2015.

Most people are probably more familiar with Jack Dorsey as the founder and CEO of Twitter but this amazingly creative guy founded another business, fintech company, Square, which is twice the size of Twitter by market value and growing at a staggering rate.

Square is two businesses, an ecosystem for sellers and Cash App, which does the same thing for individuals.

The sellers’ business declined slightly due to the initial impact of lockdown which affected its many offline sellers. This has already turned around as online business explodes and all sellers seek to ramp up the online side of their business.

The Cash App business by contrast has gone ballistic with growth of 167pc in the heavily virus affected second quarter to 30 June 2020.

The overall effect is that despite its sellers’ business declining overall growth in Q2 2020 was 64pc to $1.92bn so no surprise that the shares have been performing strongly.

Square’s shares took a hit in October 2018, when super-charismatic CFO, Sarah Friar, announced she was leaving to become CEO of an exciting unquoted Californian business.

Dorsey was in tears and I was pretty emotional myself, Friar is amazing and was a huge loss. But the company has rallied, found an impressive new CFO, Amrita Ahuuja, who came from Blizzard Entertainment and, as is clear from the latest quarterly figures, it is all systems go again at the group.

A long article in Forbes argues that Square poses a big threat to banks.

Its Cash App customer base is growing dramatically, reaching 30m in the latest quarter, while its sellers’ ecosystem involves handling transaction for its merchant customers and lending them money.

The group started, like Shopify, with smaller operators but there is an increasing trend to larger customers using Square.

I think it is game over for banks.

“Square is a cohesive commerce ecosystem that helps sellers start, run, and grow their business. We combine sophisticated software with affordable hardware to enable sellers to turn mobile and computing devices into powerful payment and point-of-sale solutions. Our tools help sellers make informed business decisions through the use of analytics and reporting. Sellers can manage orders, inventory, locations, and employees; engage customers and grow their sales; and gain access to business loans. Our approach is the same with Cash App: we see an opportunity to build a similar ecosystem of services for individuals, providing financial access to all and allowing anyone to send, spend, and save money all from one app.”

“In the second quarter of 2020, total net revenue grew 64pc year over year, to $1.92bn, and gross profit grew 28pc year over year, to $597m. Excluding Caviar [now sold] from the second quarter of 2019, total net revenue and gross profit were up 70pc and 32pc, respectively, year over year. Our Cash App ecosystem delivered strong gross profit growth of 167pc year over year as we scaled our network to more than 30m monthly transacting active customers in June. We remain focused on helping Cash App customers access our broader ecosystem of financial tools, including Cash Card. In our Seller ecosystem, gross profit was down 9pc year over year during the second quarter. Although Seller GPV (Gross Payment Volume) declined in the second quarter of 2020 on a year-over-year basis, GPV trends in our Seller business improved sequentially each month in the quarter, driven primarily by sellers resuming operations as COVID-19–related restrictions eased, consumers increasing spending, sellers adapting to contactless commerce, and new sellers joining Square.”

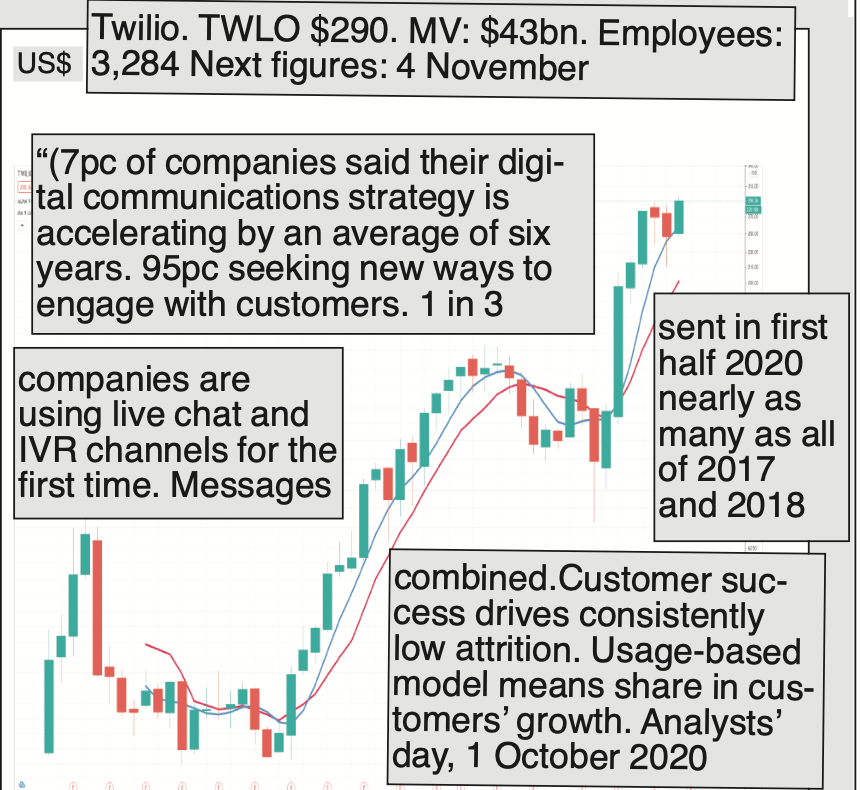

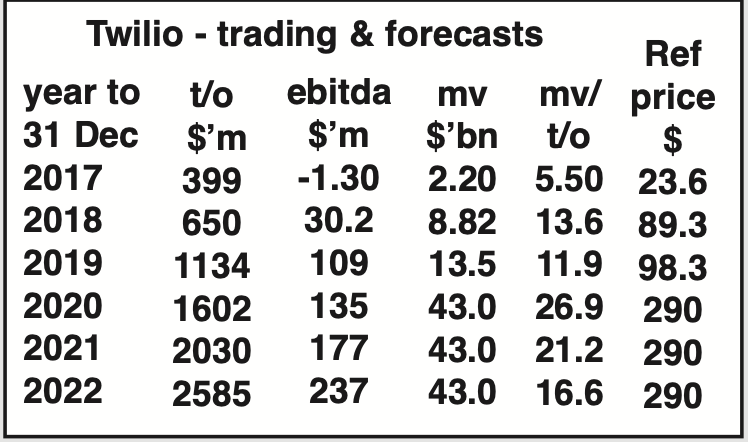

Twilio/ TWLO Buy @ $290 (update – 5)

2020 analyst day presentation and news sales to beat expectations helps Twilio shares soar.

Twilio is an American cloud communications platform as a service (CPaaS) company based in San Francisco, California. Twilio allows software developers to programmatically make and receive phone calls, send and receive text messages, and perform other communication functions using its web service APIs. Twilio was founded in 2008 by Jeff Lawson, Evan Cooke, and John Wolthuis

At one stage last Friday (2 October), shares in Twilio were up nearly 15pc don the day and they close at an all-time high. The reason was an analysts’ day presentation at which the group announced (a) that Q3 sales would come in above the high point of the group’s guidance, (b) that the total addressable market had grown to $87bn and (c) that the group was firing on all cylinders.

Twilio is an enterprise software business that supplies its customers with a software-based communications platform. The CEO and founder, Jeff Lawson, is and looks like an uber-geek although, at least in his latest photo, he has dropped the specs.

I am not so I struggle to get my head around exactly what the company does let alone how it does it. What is apparent is that whatever it is that they do they do it incredibly well.

In 2017, when the company floated it was valued at $1.2bn. The latest valuation is $43bn and I think these shares are going way higher.

In an article around that time the company was being lauded for the massive coup in landing all the Uber business across the globe.

Now Uber is just a drop in the ocean. In the latest breakdown by sectors ridesharing, aka Uber and mabe others too, was just three per cet of total turnover. The biggest sector was IT at 17pc of sales, rideshare was seventh on the list.

Also exciting is the way the number of big customers is growing. $100K plus is up from 526 to 1,445 but by the time you get to $10m plus the increase between Q4 2017 and Q2 2020 is from two to seven.

Twilio also boasts one of the highest net expansion rates (growth by existing customers) out there at 132pc v 123pc in Q4 2017.

The group’s sales and marketing spend as a percenage of revenue is low v most rivals yet the group added 79pc to its quota carrying rep headcount year on year in Q2 2020.

Despite the incredible success in the last two and half years Twlio is on a long term mission. Wow!

“We had over 28,000 Active Customer Accounts as of March 31, 2016, representing organizations big and small, old and young, across nearly every industry, with one thing in common: they are competing by using the power of software to build differentiation through communications. With our platform, our customers are disrupting existing industries and creating new ones. For example, our customers have reinvented hired transportation by connecting riders and drivers, with communications as a critical part of each transaction. Our customers’ software applications use our platform to notify a diner when a table is ready, a traveler when a flight is delayed or a shopper when a package has shipped. The range of applications that developers build with the Twilio platform has proven to be nearly limitless.”

“ Software developers are reinventing nearly every aspect of business today. Yet as developers, we repeatedly encountered an area where we could not innovate — communications. Because communication is a fundamental human activity and vital to building great businesses, we wanted to incorporate communications into our software applications, but the barriers to innovation were too high. Twilio was started to solve this problem. We believe the future of communications will be written in software, by the developers of the world — our customers. By empowering them, our mission is to fuel the future of communications. Cloud platforms are a new category of software that enable developers to build and manage applications without the complexity of creating and maintaining the underlying infrastructure. These platforms have arisen to enable a fast pace of innovation across a range of categories, such as computing and storage. We are the leader in the Cloud Communications Platform category. We enable developers to build, scale and operate real-time communications within software applications.” Twilio IPO document, 2015.

*Please note that some of the prices may have changed since this was first published in hard copy a week ago.