1 Ring to Rule Them All, 1 Share to Lead the Charge

June 4, 2024

This is an incredible chart. Not only has the index risen over 300 times since 1974 but there have been only six significant down years in that period, spanning over half a century, and only twice has there been a sequence of over two down years with three of the six severe down years coming in sequence after the bursting of the 2000 dot com bubble, which was a tulip mania event.

As the quote below suggests the biggest risk for investors is not being invested in US stocks. This can be achieved with regular ETFs, leveraged ETFs, selected UK investment trusts or most excitingly by building a portfolio of what I am coming to call Super 3G stocks. Or perhaps, most exciting but most dangerous of all, by investing in a handful of superstars.

Table of Contents

Such a portfolio will often take the form of a market leaders’ portfolio perhaps leavened with some emerging market leaders. A not entirely insane strategy would be to just hold one stock in which you believe strongly; a similar strategy to that adopted by the typical company founder. I don’t suppose Jensen Huang, co-founder and CEO of Nvidia would mind having all his eggs (chips) in that basket. It works for him. It might well work for you.

US Growth Shares are the Wonder of the Investment World

The quote below references the power and desirability of top US growth shares which are the wonder of the investment world.

Stock market investors should be feeling pretty pleased. The Dow Jones Industrial Average recently made headlines for hitting 40,000 — a long awaited milestone. While the index has pulled back, job growth and corporate profits remain solid and Friday’s inflation numbers suggest prices are slowly coming under control.

But a rising stock market isn’t without its pain points. Investors might be feeling they missed out on Nvidia, whose price has doubled this year, or AI more generally. Or they may be feeling a sense of disbelief about China, whose market has rebounded. The iShares MSCI China ETF is up more than 9pc this year, despite many investors’ deep doubts regarding the nation’s economic recovery.

The term “pain trades” — highlighted in a recent note by Nicholas Colas, co-founder of DataTrek Research — addresses situations like those, where the market refuses to comport with conventional wisdom, irking investors across Wall Street and Main Street.

“It essentially says that when everyone agrees on a given idea, everyone is wrong,” writes Colas.

Unfortunately, pain trades are an inevitable part of investing. They stem from the fact that when too many investors want to place a good bet at the same time, it gradually ceases to be a winner. Eventually that attention and anxiety leads to unexplained volatility. Prices start to diverge from their fundamentals, rising on bad news or falling on good news, explains Colas.

The disconnect between a seemingly clear investing case and what’s actually happening in the market leaves investors with difficult calls to make. Those who were early to the idea must consider whether to take profits; investors on the sidelines wonder how long they can continue to buck the rest of the market.

Either way, the situation tends to be uncomfortable.

Even legendary investors can get burned by pain trades. Colas recalls the case of George Soros who bet against tech stocks during the dot-com bubble, only to throw up his hands and go longer just as it burst. Ultimately, his fund shrank to less than half its previous size.

How to handle the pain? Colas offers two points of advice.

First, don’t be irked by short-term losses. It is better to endure a 20pc to 30pc dip, typical for bear markets, than to miss out on all of an investment’s future gains.

Second, trust in the prospects of large-cap U.S. stocks, which consistently deliver for investors over the long term. “In the end, the worst Pain Trade is being underinvested,” Colas writes.

Dow Jones Newswires, 2 June 2024

The Importance of Resistance Levels

This is the chart I usually show of Nvidia using six-month candle sticks and showing the powerful uptrend since the epic breakout in 2015. Everyone might seem to agree that Nvidia is a wonderful investment and there are no sceptics to be converted. Still, many investors think AI generally and Nvidia particularly are wildly overhyped. There are loads of people whose minds have yet to change partly because all the GenAI excitement is so new.

Nvidia shares took off in May 2023 when the company stunned investors with its massive forecast for Q2 2024 sales. This was the starting gun for the GenAI boom so it has only been running for a year. Many people expect it to run for decades and for Nvidia to remain at the heart of the action.

It is hard to put a numerical value on that; in the same way as the world’s greatest works of art are priceless the same may be true of Nvidia. Like bitcoin it may swing around wildly with momentum and day traders involved but the direction of travel looks to be strongly higher. If ever there was a company poised to rewrite the record books it is Nvidia. I have never encountered a company so exciting or a CEO so inspirational.

This is a chart you won’t often see in Quentinvest. It is a daily chart with each candlestick representing one day’s trading. It shows two things which interest me. First is the decisive breach of round number resistance at $1,000, which will be $100 after the 10:1 share split takes effect on 10 June. Second is the explosive chart breakout when the shares breached the $1,000 mark. They didn’t creep through it; they blasted through it with gaps in trading.

This is the price action I love to see. It is indicative of a bull run which is still bursting with power. I look at that price action and see a share which is going much higher.

Another interesting exercise is trying to understand what is happening with Nvidia. I am increasingly looking for answers to these questions in the Yahoo Finance Chat Rooms. I used to think people who wrote in these chat rooms were social media crazies. I am learning to be much more respectful. Some of these guys are wise and knowledgeable.

Here is a typical quote.

Nvidia keeps beating and raising in the past 3 quarters, and the price is now just keeping up.

The biggest mid-term catalyst for Nvidia is that the demand is sustainable past 2025 (FY2026), which would blow the current 18.86pc growth estimate out of the water.

If we are still early in the Generative AI journey, it’s likely to happen. Based on the facts that even OpenAI wanted to make their own chips (and some other facts) we can speculate the demand will be stronger for longer.

The risk is pull-forward demand where the biggest customers may start reducing orders when their chips start working.

But IMO [in my opinion] making the best chips requires a lot of R&D and many refresh cycles, and Nvidia with its experience will keep outperforming custom chips to the point it makes no sense to keep doing it. An example is Tesla’s Dojo. This was created to match A100 but Nvidia is now at max production of H100 while H200 & B100 are on their way in 2024.

Another problem for custom chips is software, where most developers only want to work on CUDA. When the cost is similar, it makes very little sense for them to switch.

JeffG, 4 February 2024

Or this one which is so simple but so right.

Like I’ve said before owning/buying this stock [Nvidia] is like climbing over the ridge and descending down into the Klondike, 130 or so years ago and finding a nugget or vein of gold. Hold this for a long time and collect your millions and then enjoy a peaceful and calm life.

Jack, 4 February 2024

3 Reasons to Buy Nvidia Stock Like There’s No Tomorrow…

KEY POINTS

Nvidia just announced its latest AI processor and continues to stay well ahead of the competition.

The world’s largest cloud infrastructure providers are lining up to get their hands on Nvidia’s latest and greatest.

Nvidia is increasingly supplying “full stack” solutions, which consist not only of its lightning-fast processors but also the software optimised to work with them.

Anthony, 26 March 2024

With all its future prospects, I truly believe that NVDIA stock will be marching to new highs, especially with expected strong revenue growth and total dominance of the AI market. NVDIA stock’s P/E will be much lower with the company’s explosive earnings. The company is not faced with aggressive competition from other chip manufacturers. Once in every decade, a pioneer technology company stock will be the winning stock of the decade. NVDIA is the one this decade

Abdelrahim, 6 May 2024

When we look at a long-term chart it seems that the Nvidia bull market began in July 2015 when the shares were $5. There is a case for saying that a new bull market began in the Spring of 2023 and that this bull market is still young.

A far more powerful phenomenon is driving it. The first bull run was about Nvidia’s chips and the gaming market. This second bull run is about Nvidia, GenAI, AI factories, the new industrial revolution and ubiquitous robotics. There is no comparison. In the first run, Nvidia was a bit-part player in the technology revolution. In the second, Nvidia IS the technology revolution. It is so massive the mind boggles.

Statistically, NVDA performance is rather like the rise of AMZN a few years ago. Can’t blame people for visualising a bubble. But the signals of valid, strong, persistent momentum are unmistakeable. And the company can do without Chinese buyers of its top chips.

Michael, 4 November 2023

Maybe, simplest of all is to listen to the source.

“Today, we’re at the cusp of a major shift in computing,” Huang said Sunday. “With our innovations in AI and accelerated computing, we’re pushing the boundaries of what’s possible and driving the next wave of technological advance.”

Dave, 26 March 2024

Strategy – How About Buying Some Nvidia Shares!

In terms of one of my favourite books, Lord of the Rings, Nvidia is the Ring to Rule Them All and maybe Jensen Huang is Gandalf. In the book Gandalf had the strength of mind to resist putting on the ring because it would give him more power than even he could handle. It seems Jensen Huang has no such fears. Let’s hope it turns out OK and GenAI doesn’t end up ruling us and turning Jensen Huang into Sauron.

Share Recommendations

Nvidia. NVDA. Buy @$1150 (before 10 for 1 share split)

I have found an excellent article on Nvidia which I am going to post in full. It is quite long but worth reading.

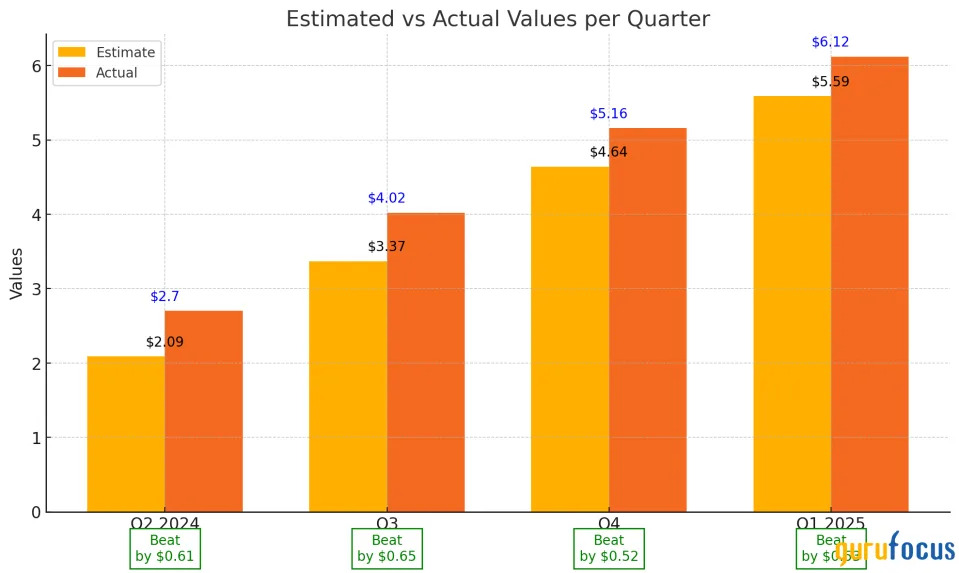

Nvidia Corp. (NASDAQ:NVDA) had one of its most remarkable quarters yet, with earnings exceeding already high expectations. The stock reached record highs in after-hours trading on May 22, achieving a market cap of around $2.50 trillion.

The company reported non-GAAP earnings of $6.12 per share, surpassing consensus estimates by approximately 10pc. Revenue reached $26.04bn, a 262pc year-over-year increase, exceeding forecasts by $1.45bn. A significant portion of this revenue, $22.60bn, came from the data centre segment, which saw 427pc growth year over year.

Key drivers of this explosive growth include Nvidia’s H100 products, with the next generation of artificial intelligence products expected from the H200, Blackwell and InfiniBand and Ethernet solutions. The H200 nearly doubles the inference performance of the H100, a crucial factor as AI growth shifts from training to inference stages, where superior inference performance could lower the total cost of AI deployments for enterprise customers. The company’s price gains are not solely based on the irrational positive sentiment on generative AI, but are matched by extraordinary earnings and revenue growth. It has recorded three consecutive quarters of over 200pc revenue growth, while profits increased by 628pc year over year, as recorded in the most recent earnings release.

Figure 1: Nvidia has consistently beaten consensus expectations over the last four quarters

Nvidia Earnings Beats

Sources: Schwab and Nvidia investor relations

Nvidia’s recent strategic initiatives, including a dividend increase and a proposed 10-to-1 stock split, indicate further positive developments on its outlook, potentially driving it to outperform in 2024 and 2025. The upcoming stock split is anticipated to boost momentum in the short term as it will be more accessible to retail investors, potentially leading to a significant increase in the stock price.

Financials

Figure 2: Nvidia income statement (FY21-FY24)

Nvidia, Q1 2025

Source: GuruFocus

In fiscal 2024, Nvidia reported unprecedented financial results, underscoring its leadership in the accelerated computing and generative AI sectors. The company achieved a record revenue of $60.90bn, reflecting an extraordinary 126pc year-over-year growth – a testament to its successful penetration and dominance in a market experiencing explosive demand across various sectors and geographies. Nvidia’s earnings per share figures highlight its exceptional profitability and growth trajectory, with the GAAP diluted earnings soaring to $11.93, a remarkable 586pc surge from the prior year. On a non-GAAP basis, which excludes certain non-recurring items, the earnings per share reached $12.96, marking an impressive 288pc increase.

Nvidia’s industry, characterised by rapid technological advances and expanding applications of AI, positions it for sustained high growth. The company has achieved a staggering rate of earnings per share growth, significantly outpacing its 10-year average of 34.30pc. Given the dynamic landscape and increasing adoption of AI technologies, I believe Nvidia is well-positioned to sustain an EPS growth rate of 20pc or higher over the next decade (reflected in my intrinsic valuation below).

In terms of Nvidia’s free cash flow [FCF] dynamics, the company experienced an extraordinary surge, increasing by 269.10pc over the past year. Over the past decade, Nvidia has maintained an average annual FCF growth rate of 28.50pc, underscoring its financial resilience and strong cash generation capabilities. These robust cash flow dynamics are crucial for sustaining future growth, funding research and development in addition to returning capital to shareholders through dividends and share buybacks, which is expected to add more value to holding the stock.

Market growth and potential

Looking forward, it is crucial to consider the current market and its expected growth. Nvidia is the leading beneficiary of this expansion given its leading position and competitive advantages. Its Blackwell architecture could deliver up to 4 times faster training than H100, potentially expanding the GPU market to 2.5 times its current size. The Blackwell platform represents a further push toward a future where AI becomes a commodity, though Nvidia is not producing commoditized hardware. This integrated approach likely helps sustain Nvidia’s valuation. With $47bn billion in revenue from its data centre segment in 2024, it is reasonable to assume that with market expansion, Nvidia could potentially generate revenue exceeding $100bn annually in data centre revenue in the near term.

Competitive landscape

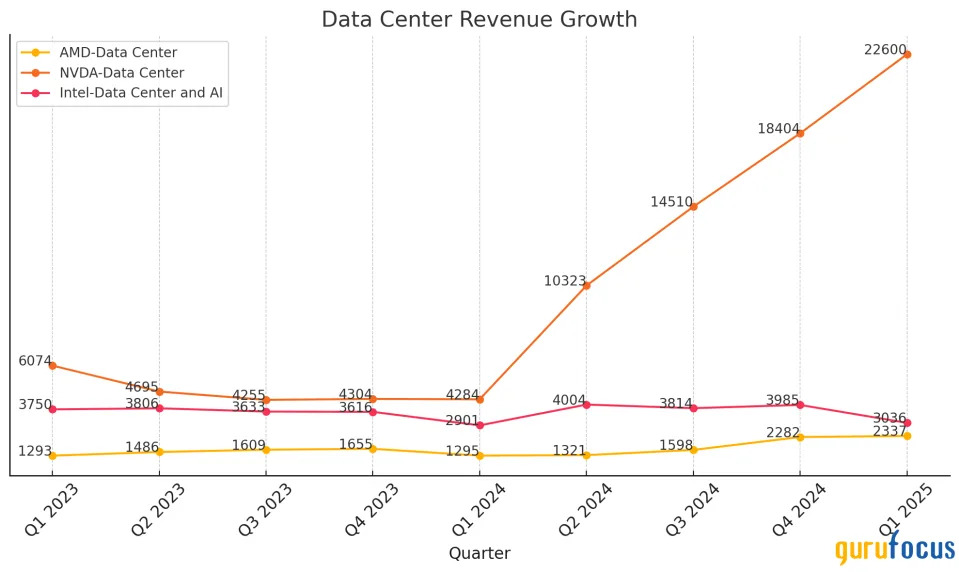

Figure 3: Nvidia dominating the AI race, recording significant data centre growth versus peers

Data centre growth v peers to Q1 2025

Source: Nvidia investor relations

In terms of its peers, Nvidia is currently leading the market by a landslide. Its data centre business has been growing much faster than those of Advanced Micro Devices Inc. (NASDAQ:AMD) and Intel Corp. (NASDAQ:INTC) over the past few quarters. Several factors contribute to its market leadership, primarily the CUDA toolkit, which enables engineers to fully leverage the GPU’s computing power to accelerate applications.

Once applications are built on CUDA, it becomes challenging for customers to switch platforms. While Intel has just started producing and developing its Gaudi 3 GPU accelerator, which uses the same process node as Nvidia’s H100, Nvidia has already begun production of its Blackwell products, the next generation of accelerators. This means competitors are at least one generation behind.

Diminished Chinese exposure

Regarding exposure to China, I believe this no longer poses significant risks to Nvidia as its Chinese revenue is now in the mid-single digits, down from around 25pc previously. This makes the current growth rates even more impressive. A return of China’s revenue is now an option if and when U.S.-China relations improve. However, a commonly discussed risk is whether cutting China off from semiconductor supplies, whether from Nvidia or ASML Holding N.V. (NASDAQ:ASML), increases the likelihood of Chinese competitors emerging. However, if AMD and Intel (being well established players) still lag Nvidia’s performance and innovation, I do not see how Chinese competitors could be a threat in the near to medium term.

Investment thesis and price target

Figure 4: Nvidia up 173pc in the past year

Shares blast through $1,000

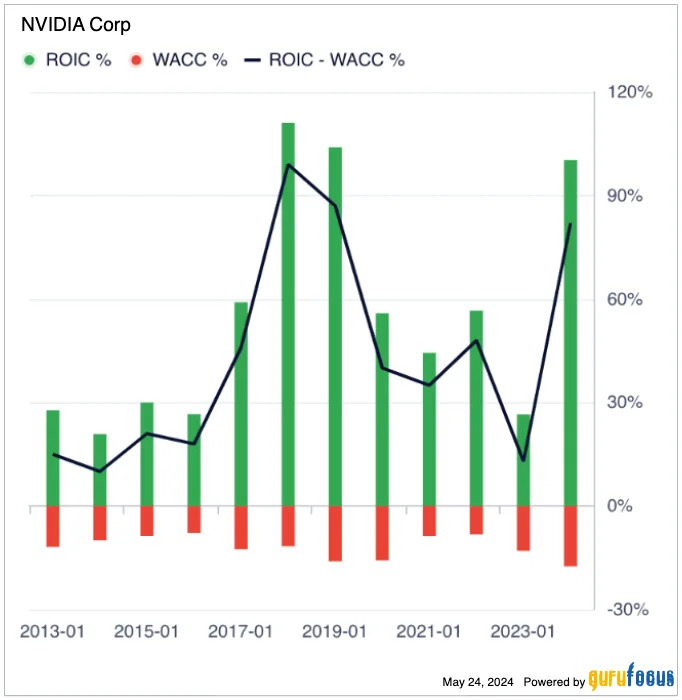

From a valuation perspective, Nvidia might not appeal to value investors as both the intrinsic and relative valuation measures suggest it is not attractive (on conservative/normalized growth estimates). Despite its stock being up over 170pc in the past year, the company’s consistent performance and significant revenue increases justify its current price levels. The company’s performance is not just hype from the AI industry; it is backed by substantial revenue increases and improving margins. In the case of Nvidia, intangible investments are increasingly important in delivering shareholder value, making traditional valuation tools less relevant. The most crucial metric is how management rewards shareholders, best shown by the return on invested capital versus the weighted average cost of capital. According to this metric (as shown below), Nvidia’s price gains are justified.

Figure 5: Nvidia’s ROIC-WACC

Nvidia Return on Capital. ROIC = return on invested capital. WACC = weighted average cost of capital

For those seeking a price target, I am confident Nvidia will maintain its leadership in the GPU market, driven by innovations such as H200 and Blackwell, along with its unique CUDA software platform. Therefore, I have established a one-year target price of $1,377 per share for Nvidia, reflecting its robust growth prospects and ongoing market-driving innovations. Some may argue this estimate is overly optimistic, but I firmly believe in its validity since we are still in the early stages of the AI revolution, and Nvidia is strategically positioned at the forefront to reap substantial benefits from this transformative wave.

Figure 6: DCF valuation upon my aggressive estimates given AI growth potential

Nvidia Valuation and Price Target

Source: GuruFocus and author estimates

Final thoughts

Nvidia’s recent financial performance has been nothing short of extraordinary, with the company’s innovative strides in AI and accelerated computing driving record-breaking revenue and earnings. While some investors might argue the stock is overvalued given its remarkable price surge over the past year, I believe this is the beginning of its growth trajectory. Nvidia’s stock price reflects not only its current operational performance, but also its future potential in a rapidly expanding market. As AI continues to evolve and integrate into various industries, Nvidia’s role as a pivotal enabler of these technologies positions it to deliver sustained growth and value to shareholders.

It is a lot to read but I have found another sensational article on Nvidia.

Erik Isakson

Along with the AI boom, Nvidia Corporation (NASDAQ:NVDA) has become the talk of the town. Nvidia’s datacentre has become crucial for the development of AI, as it has proven itself to have the best chips for machine-learning training and generation. In fact, the datacentre has provided $22.6bn out of the total $26bn in quarterly revenue. Nvidia has some other streams of income as well, like gaming ($2.6bn quarterly revenue) and visualization and robotics ($0.75bn quarterly revenue). Thus, it is indisputable that the acceleration of AI is key to Nvidia’s success.

However, there is always skepticism over how long this AI run would last, while others think Nvidia will only further its dominance as AI king as AI will only be applied more often. While I, an engineer (electrical to be exact), share similar visions of the future as Nvidia CEO Jensen Huang, I am certain that Nvidia will slow down one day – but likely not within the next 10 years. Thus, I still believe there is ample reason to invest in Nvidia, thus giving it a buy.

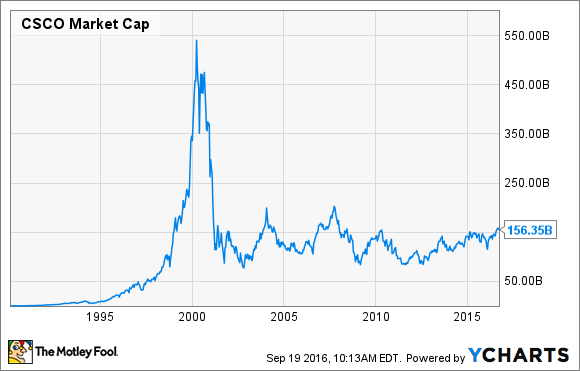

Nvidia is not Cisco

Bears for Nvidia repeatedly reference the dot-com era turbulence of Cisco Systems (CSCO) stock as a reason to avoid the skyrocketing NVIDIA stock, which has seen a price-jump of over 30pc over the past month and now is almost triple the price of last year. Cisco had its downfall during 2001, with market cap plunging by ~70pc because it over-invested in the tech bubble era, particularly in the expansion of Internet infrastructure and technology startups. This over-investment was fueled by overly optimistic projections of Internet growth, leading to an excess supply of networking equipment and significant financial losses when the tech bubble burst.

Motley Fools

However, I’m here to tell you AI is different. Analysts are predicting the market size of AI will increase from its current $200bn to $1.8 trillion by 2030.

AI has already proven to be useful over various industries, unlike the dot-com-era which had a lot of exploration for its use cases rather than practical application. ChatGPT, a user-friendly AI chatbot designed for basic response generation, reached 1m users in 5 days and 100m users in just 2 months after launch-with zero advertising. For reference, it took Instagram 2.5 years to reach 100m users with plenty of paid advertising. The spread of ChatGPT was almost purely through word-of-mouth, as users found it practically useful enough in numerous instances of everyday life. This only gives a glimpse of the power of AI in a professional setting, with more well-tuned weights for its specific applications.

For example, Google’s DeepMind AlphaFold server can predict with high-accuracy protein shapes. Shapes of tertiary and quaternary proteins have been famously difficult to calculate, as every atom responding to every layer of protein peptides has to be accounted for in determining its shape. With the help of AI, it has become possible to explore usage of proteins in processes like helping cure cancer at a rate never seen before. It can’t help but remind me of Steve Jobs’s prediction that “the biggest innovations of the 21st century will be at the intersection of biology and technology.”

Moore’s Law vs Need for Compute

In semiconductor engineering, Moore’s law has famously maintained true for the past 60 years-that the number of transistors in an integrated circuit doubles about every two years with a minimal rise in cost.

In the past, it meant making the transistors thinner, but more recently, it entails making chips bigger to fit in more transistors. This is because transistors have reached atomic levels where further decrease in size would mean jumping from classical mechanics to quantum mechanics, which simply means transistors would not behave the way we want them to. The key here is that the time when Nvidia falls is the time AI slows down to this pace of compute-improvement.

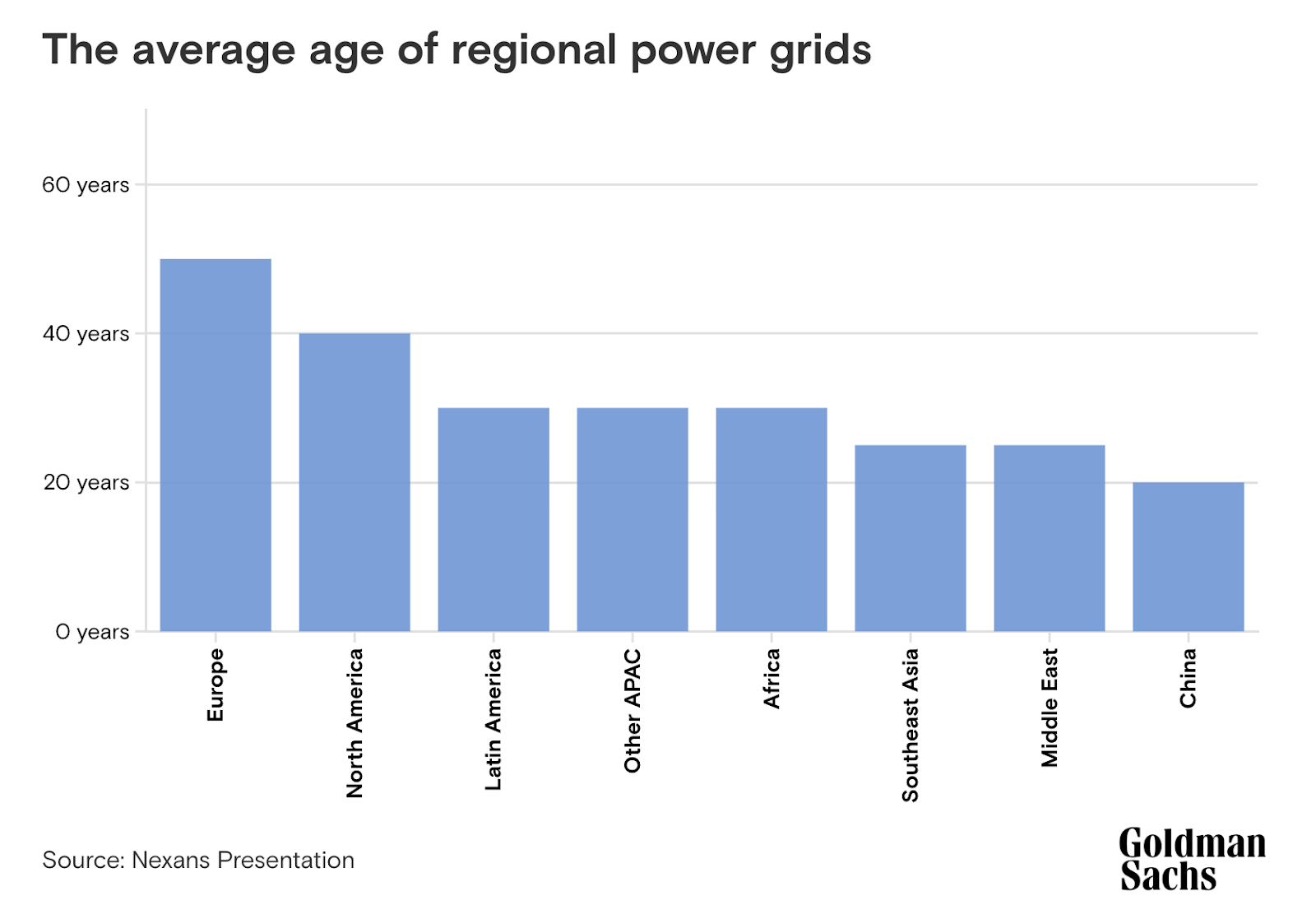

According to the Centre for the Governance of AI, “Currently, the compute used to train notable AI systems doubles every six months.” This is significantly faster than the improvement of semiconductors, which explains why Nvidia datacentre revenue is up 427pc from a year ago. The only way currently to match this pace of growth is to create more data centres. This data is further confirmed by Goldman Sachs, who estimate 8pc of U.S. power will go to datacentres by 2030, compared to the current 3pc.

In addition, to reach the growth rate of AI that Goldman Sachs analysts estimate, the US will need to invest “$50bn in new generation capacity just to support data centres alone”. Europe is estimated to invest over $1 trillion-plus to prepare its power grid for AI.

”Going forward, between 2023 and 2033, thanks to both the expansion of data centres and an acceleration of electrification, Europe’s power demand could grow by 40pc and perhaps even 50pc, according to Goldman Sachs Research. At the moment, around 15pc of the world’s data centres are located in Europe. By 2030, the power needs of these data centres will match the current total consumption of Portugal, Greece, and the Netherlands combined.”

Seeking Alpha, 31 May 2024 (Li Eason)

Goldman Sachs

Nvidia is expected to grow at a pace in which even the current power infrastructures do not support, much less compute efficiency. My point is, simple semiconductor efficiency will not justify reduced datacentre investment for many years to come, so worries that Nvidia could overinvest in its data centres like Cisco did back in the dot-com era should be put aside as every sign shows that it’s only going to continue to grow.

Nvidia’s Dominance Is Untouched, but near-term turmoil may be a problem

AI is the next big thing, its already-proven usefulness and popularity in casual and professional settings only gives up a glimpse of what AI will be capable of. Until we reach a stage where investments for AI data centres could afford to slow down-which won’t be anytime soon, Nvidia will be the centre of the show.

Nvidia’s dominance over data centres is unquestionable. In 2023, Nvidia had about 80pc of the AI chip market. In 2024, Nvidia will spend around $8.7bn in R&D, compared to $2.9bn in 2020. Nvidia’s technology is so much ahead that their CEO Jensen Huang claims “that even when the competitor’s chips are free, it’s not cheap enough.”

However, my only worry for the company is its reliance on TSMC (TSM), a Taiwan-based semiconductor manufacturing company. It is the world’s most advanced semiconductor foundry that manufactures chips for companies like Nvidia, Apple, AMD, and Qualcomm. It is known for its ability to reliably make ultra-thin 3 nm transistors that is far ahead of competitors like Samsung.

However, I believe this will be Nvidia’s weakest link in the near-term as geopolitical tension between China and Taiwan escalates. China recognizes Taiwan as its own and is known for protective policies meant to promote domestic technologies by restricting foreign ones. Thus, the future of TSMC is unclear. If it were to fall under Chinese control, strong tariffs or even outright ban may be imposed that will hurt Nvidia significantly. If that is the case, Nvidia will be only left with the technology, but no foundry to make their technology come to life-at least until other manufacturers like Samsung or ASML catch up.

Nonetheless, as TSMC provides manufacturing to all the top chip companies, it is unlikely sudden measures will be taken. Geopolitical tensions should still be carefully monitored as it could significantly impact many of the S&P companies, most notably NVIDIA.

Overall, there is still a strong upside for Nvidia as it is expected to grow at full speed for the foreseeable future. From an analytical point of view, not many understand the true pace at which AI will change the world, and in fact, Nvidia is still not at its highest demand simply because the infrastructure in many parts of the world does not allow for it. This is one of the cases where “buy low, sell high” does not apply yet, as I fully believe AI is just at its starting stages.

Seeking Alpha, 31 May 2024 (Li Eason)

Fill Your Boots

I have a feeling that Nvidia is still an early-stage fill-your-boots investment. I have been listening to Jensen Huang speaking at a conference in Taiwan where he was greeted like a rock star. I struggled to understand what he was talking about but he left me and others with the impression that Nvidia is in full creative mode with many exciting things happening. When he says this revolution is just beginning he means exactly what he says. All we have to do is believe him.

I have now listened to the whole Computex presentation which is up there with Steve Jobs’s famous Apple product launch presentations as among the most exciting presentations I have ever seen. It is easy to believe that Nvidia is at the heart of an industrial revolution which is just beginning with Huang as a latter-day George Stephenson (inventor of the steam locomotive).